Question 25 Chapter 1 of +2-A

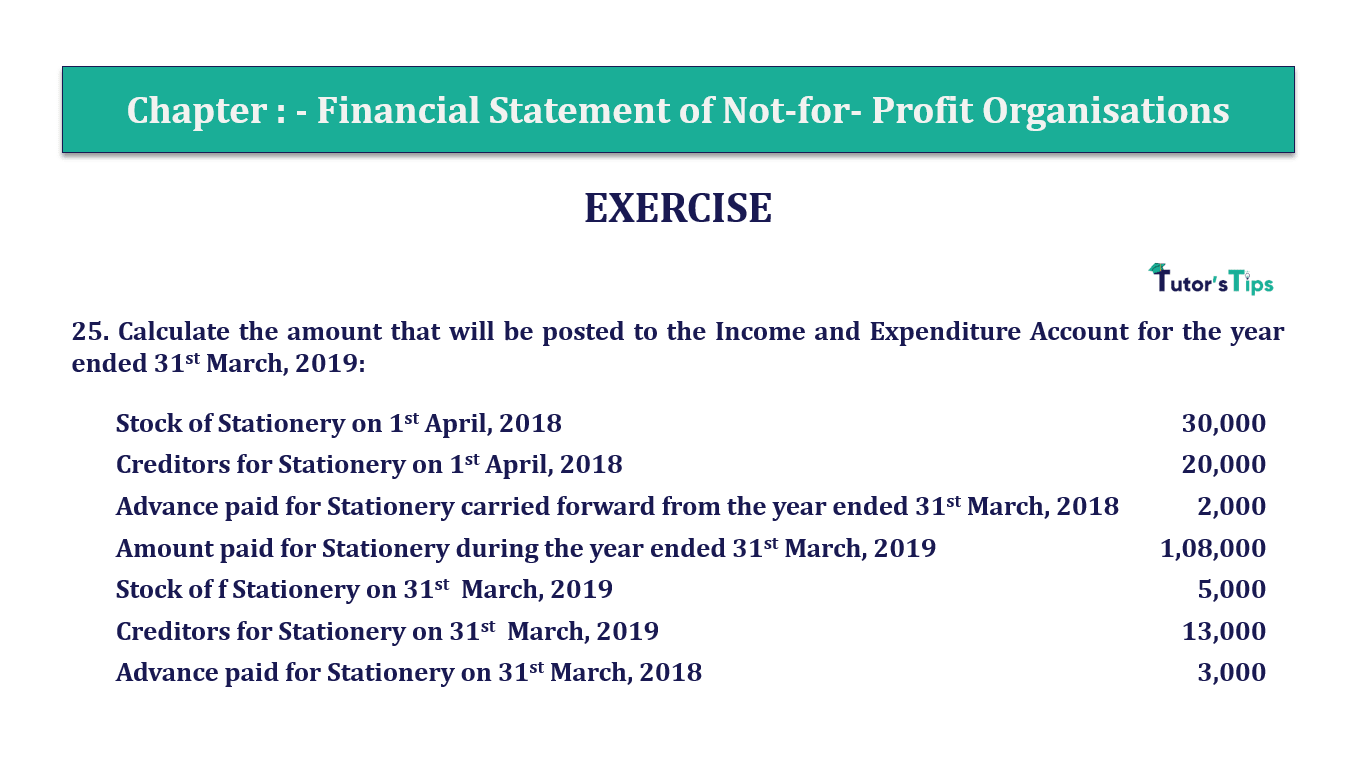

25. Calculate the amount that will be posted to the Income and Expenditure Account for the year ended 31st March 2019:

| The stock of Stationery on 1st April 2018 | 30,000 |

| Creditors for Stationery on 1st April 2018 | 20,000 |

| Advance paid for Stationery carried forward from the year ended 31st March 2018 | 2,000 |

| Amount paid for Stationery during the year ended 31st March 2019 | 1,08,000 |

| Stock off Stationery on 31st March 2019 | 5,000 |

| Creditors for Stationery on 31st March 2019 | 13,000 |

| Advance paid for Stationery on 31st March 2018 | 3,000 |

The solution of Question 25 Chapter 1 of +2-A: –

| Statement Showing stationery used during the year |

||

| Particular | Details | Amount |

| Amount paid for stationery during the year ended 31st March 2019 | 1,08,000 | |

| Add: – Opening Stock of Stationery | 30,000 | |

| Closing Creditors for Medicines | 13,000 | |

| Opening Advance paid for Stationery | 2,000 | 45,000 |

| 1,53,000 | ||

| Less: – Closing Stock of Medicines | 5,000 | |

| Opening Creditors for Stationery | 20,000 | |

| Closing Advance paid for Stationery | 3,000 | |

| 28,000 | ||

| The amount for Medicine debited to the Income and Expenditure A/c | 1,25,000 | |

Note: Opening balance of advance paid for the purchase of stationery is added in the total amount paid because this amount had shown as an advance in last year balance sheet it means that the items of stationery are delivered against this amount in the current year. So we can use these items in the current year so that’s why this is the expenditure of the current year rather than the previous year. And the closing balance of advance paid is treated opposite of opening balance.

| Income and Expenditure Account |

|||

| Particular | Amount | Particular | Amount |

| To Medicines Consumed | 1,25,000 | ||

Not-for-Profit Organisations – Meaning and Overview

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: –

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication