Question 19 Chapter 8 – Unimax Publication Class 12 Part 2 – 2021

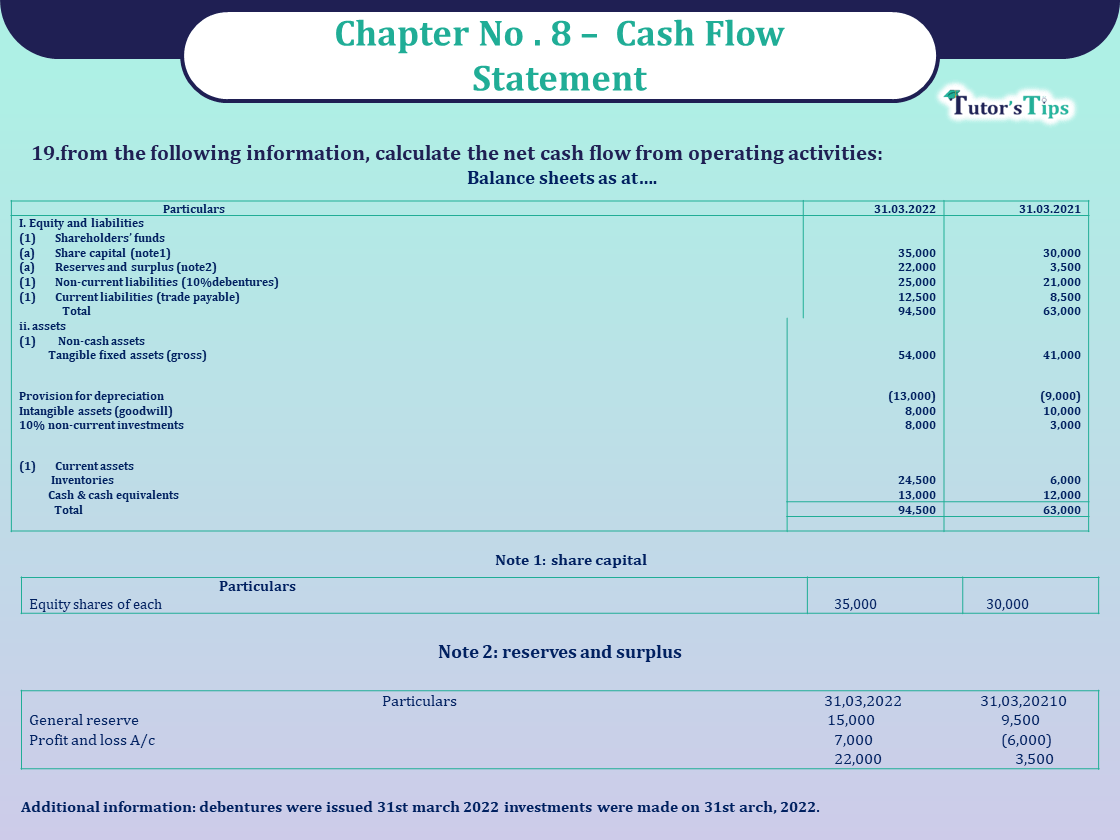

19.from the following information, calculate the net cash flow from operating activities:

Balance sheets as at….

| Particulars | 31.3.2022 ₹ | 31.3.2021 ₹ |

| I. Equity and liabilities | ||

| (1) Shareholders’ funds | ||

| (a) Share capital (note1) | 35,000 | 30,000 |

| (B) Reserves and surplus (note2) | 22,000 | 3,500 |

| (2) Non-current liabilities (10%debentures) | 25,000 | 21,000 |

| (3) Current liabilities (trade payable) | 12,500 | 8,500 |

| Total | 94,500 | 63,000 |

| ii. Assets | ||

| (1) Non-cash assets | ||

| Tangible fixed assets (gross) | 54,000 | 41,000 |

| Provision for depreciation | (13,000) | (9,000) |

| Intangible assets (goodwill) | 8,000 | 10,000 |

| 10% non-current investments | 8,000 | 3,000 |

| (2) Current assets | ||

| Inventories | 24,500 | 6,000 |

| Cash & cash equivalents | 13,000 | 12,000 |

| Total | 94,500 | 63,000 |

Note 1: share capital

| Particulars | 31.03.2022 (₹) | 31.03.2021 (₹) |

| Equity shares of each | 35,000 | 30,000 |

Note 2: Reserves and surplus

| Particulars | 31.3.2022 (₹) | 31.3.2021 (₹) |

| General reserve | 15,000 | 9,500 |

| Profit and loss A/c | 7,000 | (6,000) |

| 22,000 | 3,500 |

Additional information: debentures were issued 31st march 2022 investments were made on 31st arch, 2022.

The solution of Question 19 Chapter 8 – Unimax Publication Class 12 Part 2-2021 : –

Calculation of cash from operating activities

for the year ended 31st march ,2022

| ₹ | ₹ | |

| Net profit before tax (note1) | 18,500 | |

| Adjustment for non-cash and non- operating items: | ||

| add: payment of interest on long-team borrowing | ||

| (debentures) (10%on 21,000) | 2,100 | |

| Depreciation (13,000-9,000) | 4,000 | |

| Goodwill written off | 2,000 | 8,100 |

| 26,600 | ||

| Less: interest on non-current investments | 300 | |

| Operating profit before working capital changes | 26,300 | |

| Add: increase in current liabilities | ||

| Trade payable | 4,000 | |

| 30,300 | ||

| Less: increase in current assets: | ||

| Inventory | (18,500) | |

| Net current flow from operating activities | 11,800 |

Notes: (i) calculation of net profit before tax:

| Net profit during current year (7,000+6,000) | = | 13,000 |

| Add: transfer to general reserve | = | 5,500 |

| 18,500 |

Negative balance of profit & loss amounting to 6,000 appearing in the balance sheet on 31.3.2021 represents an amount of loss. In the current year, after covering this loss 6,000 the profit & loss shows a profit of 7,000. It means that net profit during the current year must have been 7,000+6,000=13,000

Cash flow from investing activities

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

What is the cash flow statement? why do we need to prepare?

Unimax Publication – Accountancy PSEB Class 12 – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Change in Profit sharing ratio among Existing Partners )

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Unimax Publication – Accountancy PSEB (Class 12) – Part – II – Solution

- Chapter No. 1 – Company Accounts (Share Capital)

- Chapter No. 2 – Company Accounts (Issue of Debentures)

- Chapter No. 3 – Company Accounts (Redemption of Debentures)

- Chapter No. 4 – Financial Statements of a Company

- Chapter No. 5 – Financial Statement Analysis

- Chapter No. 6 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 7 – Ratio Analysis

- Chapter No. 8 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2023@ Official Website of Sultan Chand Publication