Question 1 Chapter 1 of +2-A

EXERCISE

Receipts and Payment Account

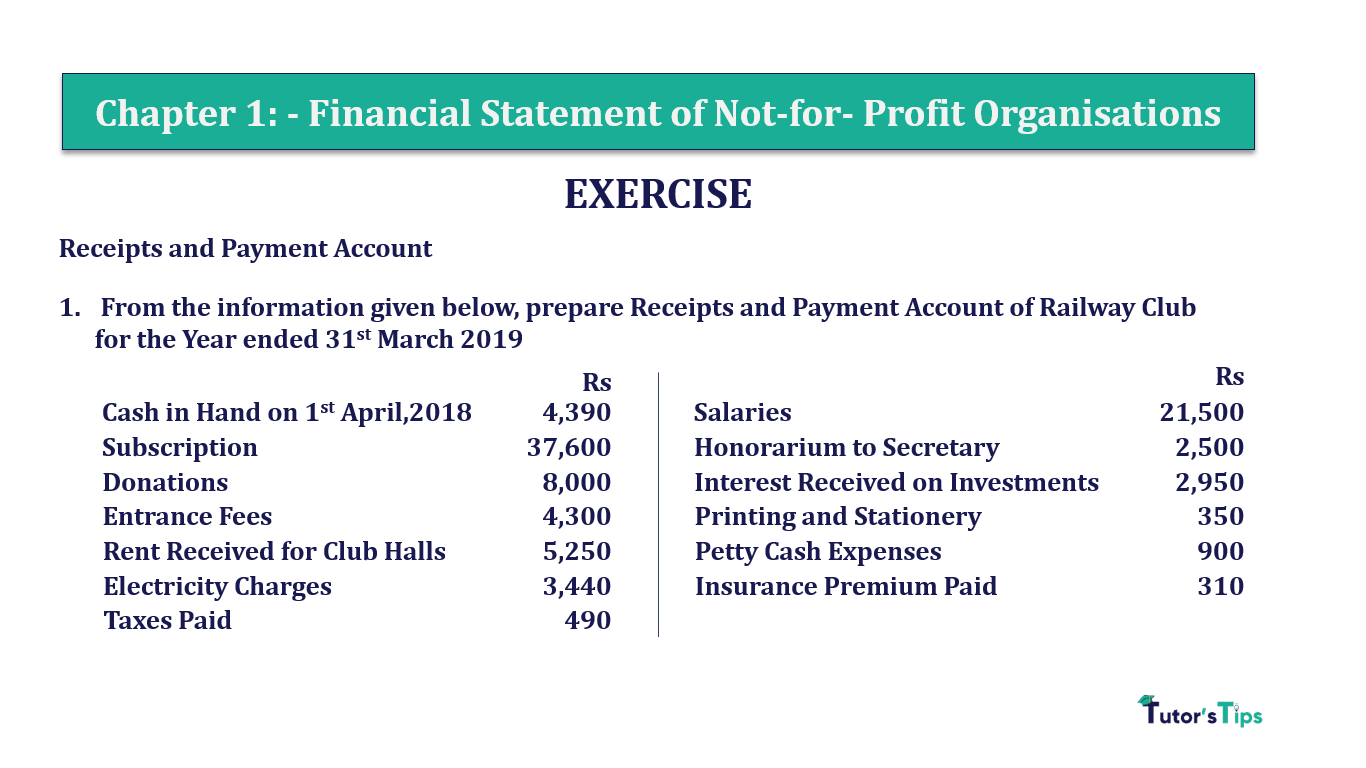

1. From the information given below, prepare Receipts and Payment Account of Railway Club for the Year ended 31st March 2019

| Rs | Rs | ||

| Cash in Hand on 1st April 2018 | 4,390 | Salaries | 21,500 |

| Subscription | 37,600 | Honorarium to Secretary | 2,500 |

| Donations | 8,000 | Interest Received on Investments | 2,950 |

| Entrance Fees | 4,300 | Printing and Stationery | 350 |

| Rent Received for Club Halls | 5,250 | Petty Cash Expenses | 900 |

| Electricity Charges | 3,440 | Insurance Premium Paid | 310 |

| Taxes Paid | 490 |

The solution of Question 1 Chapter 1 of +2-A

: –

| In the Books of Railway Club | |||

| Receipts and Payment A/c |

|||

| as on 31st March 2019 | |||

| Particulars |

Amount | Particulars |

Amount |

| To Balance b/d | 4,390 | By Electricity Charges A/c | 3,440 |

| To Subscription A/c | 37,600 | By Taxes Paid A/c | 490 |

| To Donations A/c | 8,000 | By Salaries A/c | 21,500 |

| To Entrance Fees A/c | 4,300 | By Honorarium to Secretary A/c | 2,500 |

| To Rent Received for Club Halls A/c | 5,250 | By Printing and Stationery A/c | 350 |

| To Interest Received A/c | 2,950 | By Petty Cash Expenses A/c | 900 |

| By Insurance Premium A/c | 310 | ||

| By Balance c/d | 33,000 | ||

| 62,490 | 62,490 | ||

Receipts:

It means that when a business has received cash from any source. All receipts are written on the Debit side of the Receipts and Payment account.

Payments:

It means that when a business has paid cash to anyone to run a business operation. All Payments are written on the Credit side of the Receipts and Payment account.

Receipts and Payment Account:

It means that in which we record the all-cash/bank-related transaction of Not-for-profit businesses, which occur during the year. This is similar to the cash account. It includes all previous as well as future year transactions (related to payment and receipts) which occur in the current year.

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: –

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication