To know to differences between provision and reserve we have to know the meaning of both the terms are shown below: –

Meaning of Provision:-

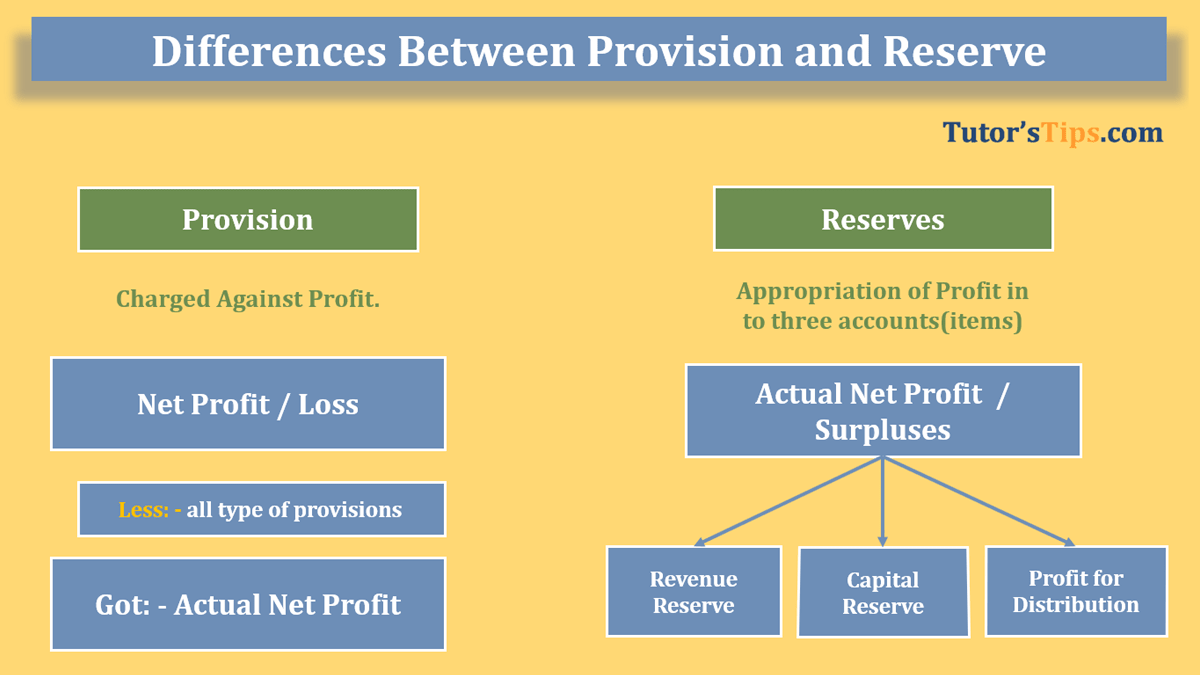

The provision in accounting means that amount which is charged against Profit or loss account(Income statement) for some uncertain amount of known liability which will be incurred in the near future.

To calculate the true profit or loss of the business for the current year, we have to charge the unknown amount of known expenses or liabilities which are related to current year operating activities to profit/loss account on the proportionate basis by making provision for this amount at the time of preparing financial statements.

Meaning of Reserve:-

A reserve refers to that proportionate amount of net profit or surpluses which is retained for the future payments. In other words, the retention of the profit which is not for any known liability.

According to William Pickles. “Reserve means the amount set aside out of profit and other surpluses, which are not earmarked in any way to meet any particular liability known to exist on the date of Balance Sheet.”

To get more explanation on the meaning of Provision and Reserves with the example please visit our last articles if you did not read.

The provision in accounting: Types and Treatment

Reserve: Meaning, type, Accounting treatment

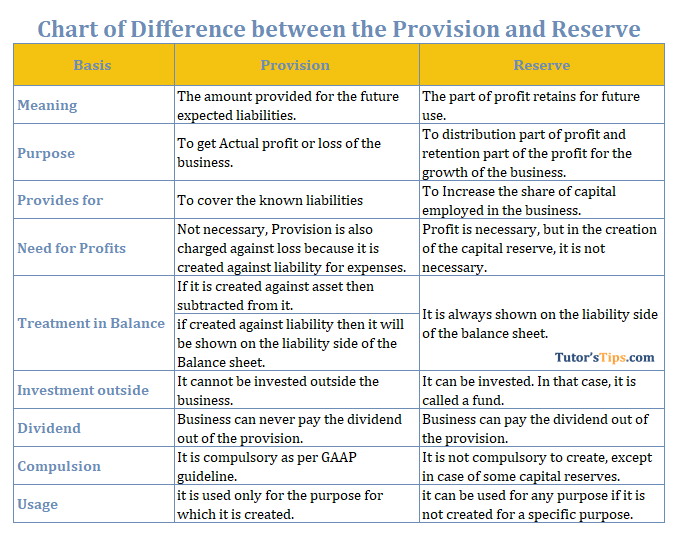

Chart of Difference between the Provision and Reserve.

Basis |

Provision |

Reserve |

| Meaning | The amount provided for the future expected liabilities. | The part of profit retains for future use. |

| Purpose | To get Actual profit or loss of the business. | To distribution part of profit and retention part of the profit for the growth of the business. |

| Provides for | To cover the known liabilities | To increase the share of capital employed in the business. |

| Need for Profits | Not necessary, Provision is also charged against loss because it is created against liability for expenses. | Profit is necessary, but in the creation of the capital reserve, it is not necessary. |

| Treatment in Balance | If it is created against asset then subtracted from it. if created against liability then it will be shown on the liability side of the Balance sheet. |

It is always shown on the liability side of the balance sheet. |

| Investment outside | It cannot be invested outside the business. | It can be invested. In that case, it is called a fund. |

| Dividend | Business can never pay the dividend out of the provision. | Business can pay the dividend out of the provision. |

| Compulsion | It is compulsory as per GAAP guideline. | It is not compulsory to create, except in case of some capital reserves. |

| Usage | it is used only for the purpose for which it is created. | it can be used for any purpose if it is not created for a specific purpose. |

The Example of Difference between the Provision and Reserve: –

Example |

Provision |

Reserve |

| 1 | Provision against an Asset: –

Create a 5% Provision for Doubtful or bad debts. Sundry Debtors = 5,00,000/- Provision for Doubtful or bad debts = 500000 X 5/100 = 25,000/- Accounting Treatment: – In the Profit or loss account: – Provision for doubtful or Bad debts post in the debit side of the P/L account or post as expenses in the Income statement. or added to the bad debts during the year. In the balance sheet:- It will be subtracted from the sundry debtors. |

Revenue Reserve: –

Create 25% Reserve for workman compensation. Net Profit = 50,000/- Workman Compensation Reserve = 50000 X 25/100 = 12,500/- Accounting Treatment: – It will be shown in the Appropriate Profit or Loss account. Workman Compensation Reserve post in the debit side of the P/L accounts. In the Balance Sheet : – It will be shown on the liability side. |

| 2 | Provision against a Liability: –

Create a Provision for taxation on Net profit @30% Net Profit Before Tax (NPBT) = 1,00,000/- Provision for Taxation: 100000 X 30% = 30,000/- Accounting Treatment: – In Profit or loss account: – Provision for Taxation post in the debit side of the P/L account or post as expenses in the Income statement. In the balance sheet:- It will be shown on the liability side. |

Capital Reserve: –

100 no. Equity share reissued. The face value of the share is Rs 10 and issued @ Rs 8/- as fully paid. The forfeiture balance of these shares is available for Rs 500/-. Utilize the short amount of from the forfeiture balance and reaming transfer to capital reserve. 100 X 10 = 1,000 (-) 100 X 8 = 800 = 200 Balance 200/- will be utilized from the Forfeiture balance 500 – 200 = 300/- Rs 300 will be transferred to Capital Reserve Accounting Treatment: – In the balance sheet (only):- It will be shown on the liability side. |

Download the chart: –

If you want to download the chart please download the following image and PDF file:-

The conclusion of the Difference: –

Provision and reserve both the terms are related to the profit and loss account but provision decreases the profit or increases the loss and reserve are part of the profit.

Thanks for reading the topic

In the comment box, please write your feedback. whatever you want. If you have any question please ask us by commenting.

Check out T.S. Grewal’s +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping