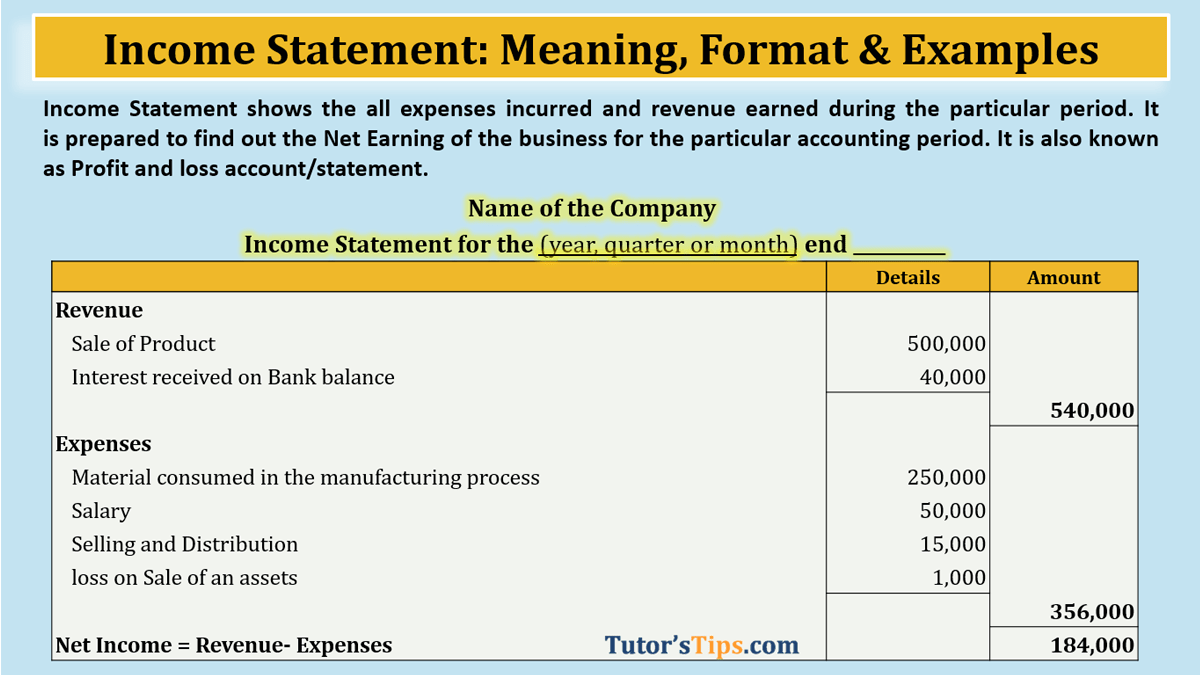

The income statement shows all expenses incurred and revenue earned during a particular period. It is prepared to find out the Net earnings of the business for the particular accounting period. It is also known as Profit and loss account/statement.

The income statement is one of all three financial statements. these are Income Statements, Balance sheet, and Cash flow statement. The income statement represents the actual earning of the company for a particular period of time. The period will be mentioned in it like Income statement is as on 30 September 2018. (also check Difference between the Profit and Loss Account (Income Statement) and Balance Sheet)

The focus of Income Statement: –

The income statement has focused on the nominal account only means revenue, expenses, loss, and gains. It is an accrual-based statement. It shows total expenses due or not only paid and income earned or not only received for a particular period. Further Explanation of these terms are shown below: –

- Revenue/Income

- Expenses

- Loss

- Gain

1. Revenue/Income : –

Revenue/income is the amount that a company earned during a particular period. It can be further divided into two parts: –

- Operating Revenue/Income

- Non-Operating Revenue/Income

Operating Revenue/Income: –

Operation Revenue/Income those revenues which are earned by business from its primary activities. Like revenue earned from the sale of their goods and services. For example, the operating revenue for the manufacture of shoes is that which he will be earned from the sale of shoes.

Non-Operating Revenue/Income: –

Non-Operation Revenue/Income those revenues which are earned by business from its secondary activities. Like revenue earned from the bank in the form of interest on the bank balance, rent received from the tenant. It means all that income which is separate from the sale of goods and services.

2. Expenses: –

Expenses are the amount that a company spent during a particular period to earn revenue. It can be further divided into two parts: –

- Operating Expenses

- Non-Operating Expenses

Operating Expenses: –

Operation Expenses are those expenses that are spent by business on its primary activities. Like expenses met on the purchase of their goods and services. For example, the operating expenses for the manufacture of shoes is that which he will be paid for the purchase of raw material for the manufacturing shoes. All other expenses met on the conversion of this raw material into the finished product i.e. shoes. Examples, Factory lighting, Repair and maintenance of Plant and machine, Salary of employees, Selling and distribution of product, etc.

Non-Operating Revenue/Income: –

Operation Expenses are those expenses that are spent by business on its secondary activities. Like Interest paid on loan, Charges for obsolescence of assets or currency exchange are also non-operating expenses.

3. Losses: –

All money spent on unusual events is known as losses. Like, Sale of old assets on the price less than book value and claims paid against lawsuits.

4. Gains: –

All money earned on unusual events is known as Gains. Like, Sale of old assets on price more than book value and claims received against lawsuits,

The format of Income Statement: –

In simple, in the income statement, we have deducted total expenses and losses from the total revenues and gains. i.e. Net income = Total Income(Revenue + gains) – Total Expenses(Expenses + loss).

The presentation of it may vary from country to country. The example of it shown below: –

| Name of the Company | ||

| Income Statement for the (year, quarter or month) end __________ | ||

| Details | Amount | |

| Revenue | ||

| Sale of Product | 500,000 | |

| Interest received on Bank balance | 40,000 | |

| 540,000 | ||

| Expenses | ||

| Material consumed in the manufacturing process | 250,000 | |

| Wages | 30,000 | |

| Salary | 50,000 | |

| Rent | 10,000 | |

| Selling and Distribution | 15,000 | |

| loss on the sale of an assets | 1,000 | |

| 356,000 | ||

| Net Income = Revenue- Expenses | 184,000 | |

In the above Example, The total amount received from the operating activities, non-operating activities, and gains are equal to 540,000/- and The total amount spends on operating activities, non-operating activities and losses are equal to 356,000/-. So, we get 184,000/- as our net income after deduction total expenses from the total income. it is a simple presentation of the income statement to understand the basic calculation.

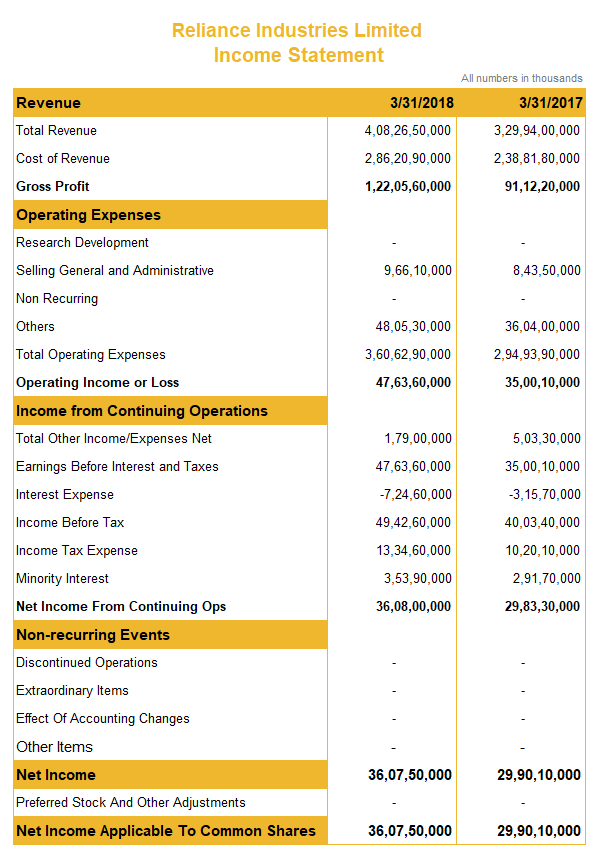

Example of Income Statement:

The Example of the listed Company – Reliance Industries Limited: –

Data Collected from Yahoo! Finance

| Reliance Industries Limited | ||

| Income Statement | ||

| All numbers in thousands | ||

| Revenue | 3/31/2018 | 3/31/2017 |

| Total Revenue | 4,08,26,50,000 | 3,29,94,00,000 |

| Cost of Revenue | 2,86,20,90,000 | 2,38,81,80,000 |

| Gross Profit | 1,22,05,60,000 | 91,12,20,000 |

| Operating Expenses | ||

| Research Development | – | – |

| Selling General and Administrative | 9,66,10,000 | 8,43,50,000 |

| Non Recurring | – | – |

| Others | 48,05,30,000 | 36,04,00,000 |

| Total Operating Expenses | 3,60,62,90,000 | 2,94,93,90,000 |

| Operating Income or Loss | 47,63,60,000 | 35,00,10,000 |

| Income from Continuing Operations | ||

| Total Other Income/Expenses Net | 1,79,00,000 | 5,03,30,000 |

| Earnings Before Interest and Taxes | 47,63,60,000 | 35,00,10,000 |

| Interest Expense | -7,24,60,000 | -3,15,70,000 |

| Income Before Tax | 49,42,60,000 | 40,03,40,000 |

| Income Tax Expense | 13,34,60,000 | 10,20,10,000 |

| Minority Interest | 3,53,90,000 | 2,91,70,000 |

| Net Income From Continuing Ops | 36,08,00,000 | 29,83,30,000 |

| Non-recurring Events | ||

| Discontinued Operations | – | – |

| Extraordinary Items | – | – |

| Effect Of Accounting Changes | – | – |

Other Items |

– | – |

| Net Income | 36,07,50,000 | 29,90,10,000 |

| Preferred Stock And Other Adjustments | – | – |

| Net Income Applicable To Common Shares | 36,07,50,000 | 29,90,10,000 |

If you want to Download the statement please download the following image: –

Thanks for reading the topic, please comment your feedback in the comment box whatever you want. If you have any question please ask us by commenting.