The basic Difference Between Revaluation and Realisation account is the time of preparation. The revaluation account is prepared when there are changes in the partnership deep but the realisation account is prepared when the firm is dissolved.

To know the difference between these two, we must clear the meaning of these terms and explained as follows: –

Meaning of Revaluation Account:-

The revaluation account is prepared to get the profit or loss on the revaluation of assets and reassessment of liabilities at the time of the reconstitution of the partnership firm. We have to revaluate the assets when there is a reconstruction of the firm like a change in the profit-sharing. The difference amount if increased then it will be posted on the debit side of the revaluation account and if decreased then it will be posted on the credit side of the revaluation account.

Meaning of realisation account: –

The realisation account is prepared at the time of the dissolution of the firm to know the profit or loss on realizing assets and repay the liabilities of the firms. This amount of profit or loss will be transferred to the partners’ capital or current account. In the case of capital fixed in nature, we will transfer the amount of profit/loss to the partners’ current account or in the case of the capital account is fluctuating in nature then transfer to the partners’ capital account.

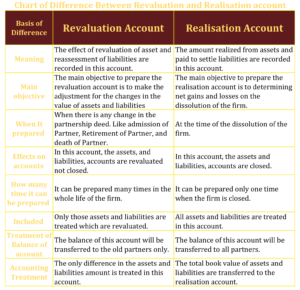

Chart of Difference Between Revaluation and Realisation account: –

Basis of Difference |

Revaluation Account |

Realisation Account |

| Meaning | The effect of revaluation of asset and reassessment of liabilities are recorded in this account. | The amount realized from assets and paid to settle liabilities are recorded in this account. |

| Main objective | The main objective to prepare the revaluation account is to make the adjustment for the changes in the value of assets and liabilities | The main objective to prepare the realisation account is to determining net gains and losses on the dissolution of the firm. |

| When It prepared | When there is any change in the partnership deed. Like admission of Partner, Retirement of Partner, and death of Partner. | At the time of the dissolution of the firm. |

| Effects on accounts | In this account, the assets, and liabilities, accounts are revaluated not closed. | In this account, the assets and liabilities, accounts are closed. |

| How many time it can be prepared | It can be prepared many times in the whole life of the firm. | It can be prepared only one time when the firm is closed. |

| Included | Only those assets and liabilities are treated which are revaluated. | All assets and liabilities are treated in this account. |

| Treatment of Balance of account | The balance of this account will be transferred to the old partners only. | The balance of this account will be transferred to all partners. |

| Accounting Treatment | The only difference in the assets and liabilities amount is treated in this account. | The total book value of assets and liabilities are transferred to the realisation account. |

Download the chart in PNG and PDF:-

If you want to download the chart please download the following image and PDF file:-

Conclusion:

Thus, both terms are different from each other on the basis of the time of preparation. revaluation account is prepared at the time of reconstruction of partnership and realisation account is prepares at the time of closing of the firm.

Thanks for reading the topic.

please comment your feedback whatever you want. If you have any questions please ask us by commenting.

Check out T.S. Grewal’s +2 Book 2020 @ Official Website of Sultan Chand Publication