Usha 2024 – Class 12

Usha-2024-Part I – Solution

Usha-2024-Part II – Solution

Book Solutions

Class +1 – Accountancy

Usha Publication Book’s Solution – PSEB

Unimax Publications Book’s Solution – PSEB

D K Goel Book’s Solution – ISC

T.S. Grewal’s Book’s Solution – CBSE

Class +2 – Accountancy

Usha Publication – Part I – Solution

Usha Publication – Part II – Solution

Unimax Publications Part 1 – Solution

Unimax Publications Part 2 – Solution

T.S. Grewal’s Book Part – A Vol. I – Solution

T.S. Grewal’s Book Part – A Vol. II – Solution

T.S. Grewal’s Book Part B – Solution

V K Publications Part B– Solution

Video Lectures

Video Lectures Class 11

Accounts

Business Studies

Economics

Video Lectures Class 12

Accounts

Business Studies

Economics

Store

Chapter No. 4-Accounting Ratios

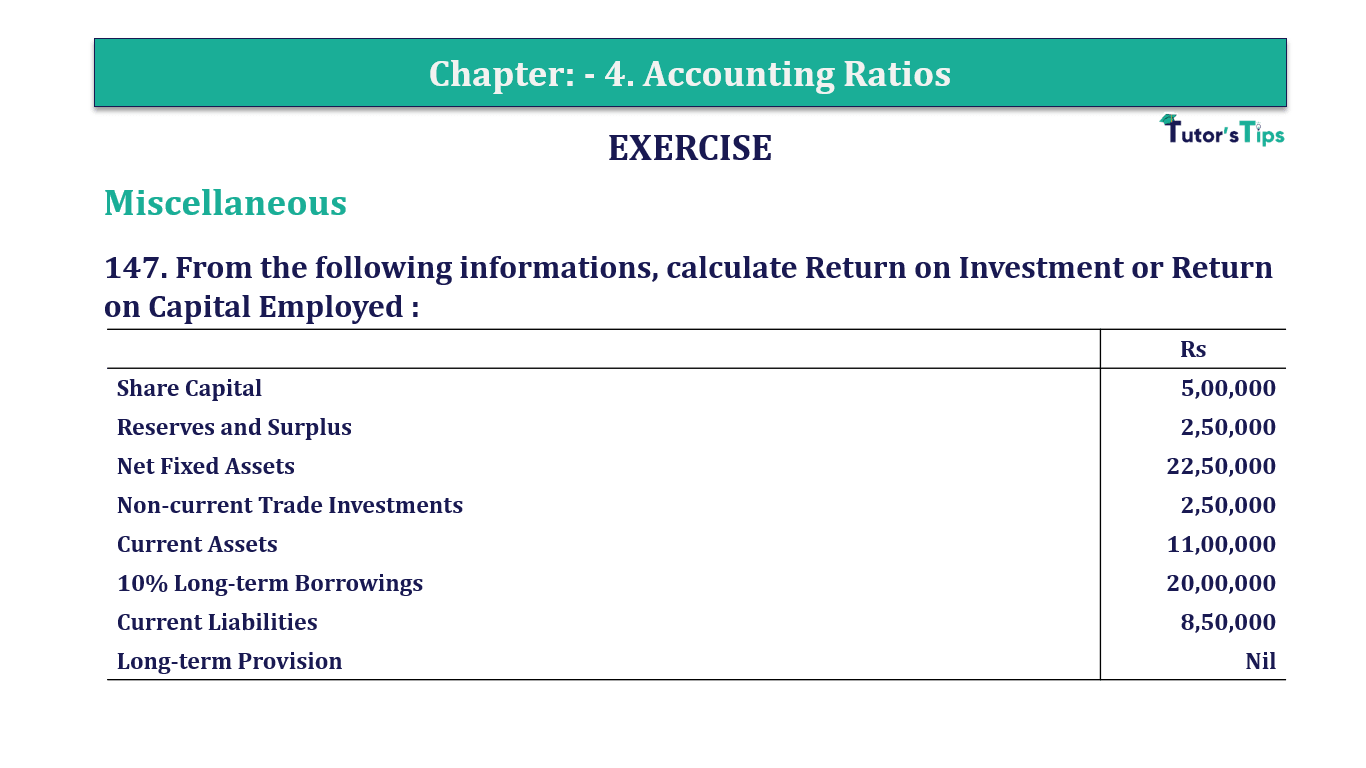

Question 147 Chapter 4 of +2-B – T.S. Grewal 12 Class

Question 146 Chapter 4 of +2-B – T.S. Grewal 12 Class

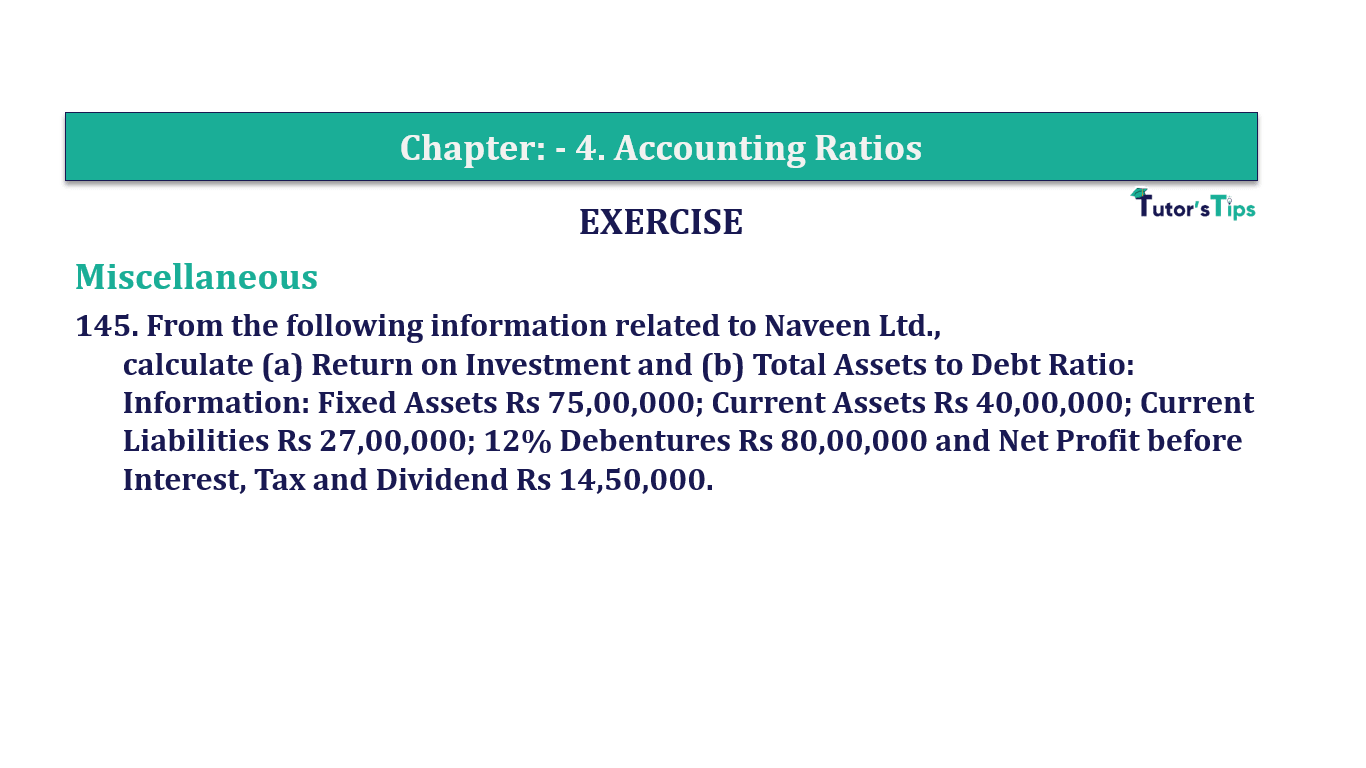

Question 145 Chapter 4 of +2-B – T.S. Grewal 12 Class

Question 144 Chapter 4 of +2-B – T.S. Grewal 12 Class

Question 143 Chapter 4 of +2-B – T.S. Grewal 12 Class

Question 142 Chapter 4 of +2-B – T.S. Grewal 12 Class

Question 141 Chapter 4 of +2-B – T.S. Grewal 12 Class

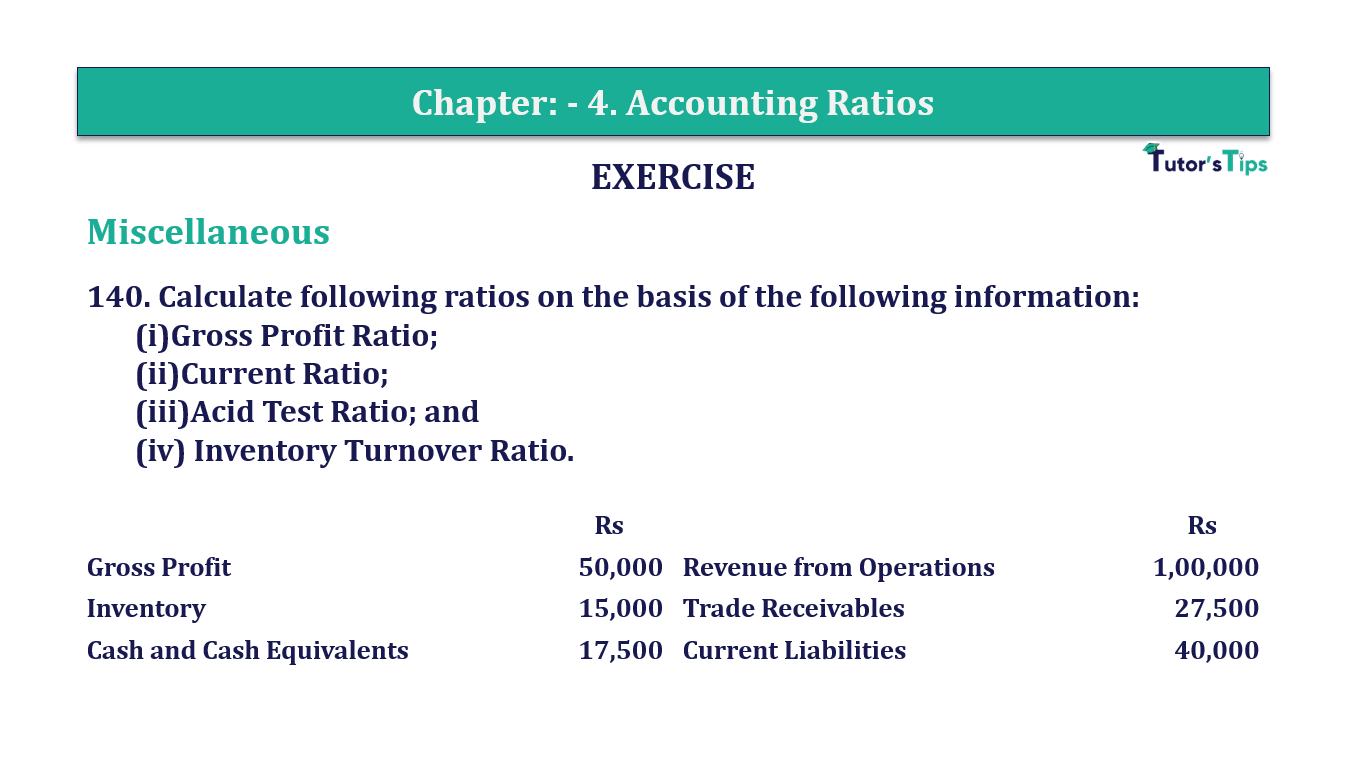

Question 140 Chapter 4 of +2-B – T.S. Grewal 12 Class

Question 139 Chapter 4 of +2-B – T.S. Grewal 12 Class

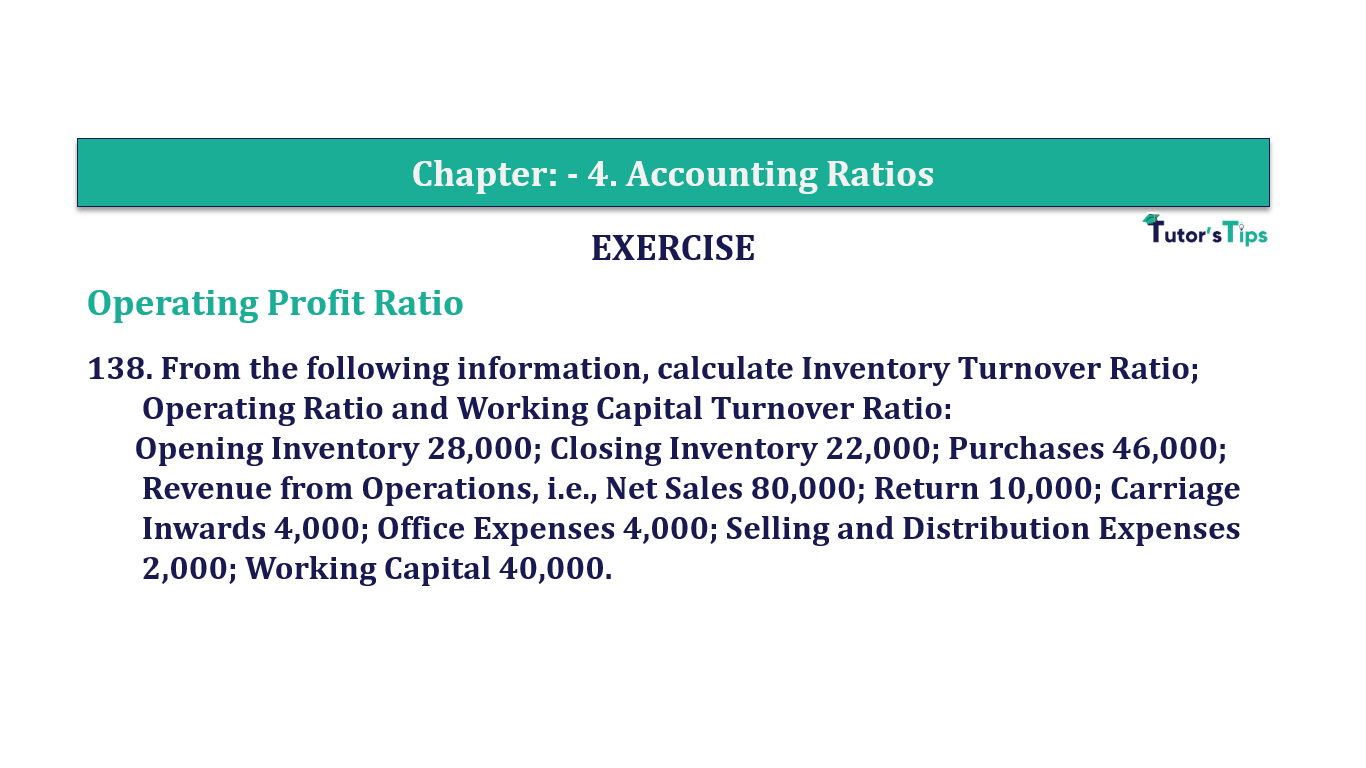

Question 138 Chapter 4 of +2-B – T.S. Grewal 12 Class

Advertisement

1

2

…

15

error:

Content is protected !!