In this article, We will explain to you the Basic Journal Entries and after this chapter, You will know about all journal entries which are regularly used in all business.

1. Capital:

Capital means investing anything by the owner in the business. It may be in cash or in kind.

Subscribe to our Youtube Channel

Example: –

01/02/2018 Started Business with cash Rs. 1,00,000/-, Building 15,00,000/-, Furniture 1,75,000/-.

we are solving this example in the following table:

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

| Cash -> | Assets -> | Real Account -> | cash comes In the business -> | What comes In -> | Debit |

| Building -> | Assets -> | Real Account -> | Building Comes In the business -> | What comes In -> | Debit |

| Furniture -> | Assets -> | Real Account -> | Furniture Comes In the business -> | What comes In -> | Debit |

| Capital->*1 | Personal -> | Personal Account -> | Owner giving cash and other assets to business-> | The Giver -> | Credit |

*1 Note:- In this transaction, we can not credit the name of the Owner in the books of business because anything invest by the owner in the business is known as capital. So, we have to create an account named the capital and credit it.

2. Drawing:

Drawing is anything withdrawal by the owner from the business. This is also a Basic Journal Entries.

Example:

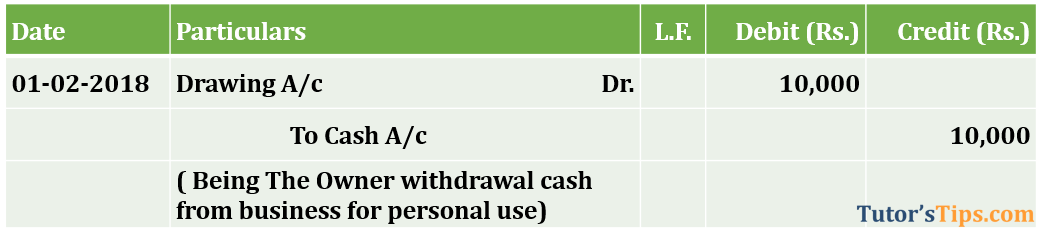

01/02/2018 Owner Withdrawal cash Rs 10,00/- from the business for personal use

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

| Drawing-> *2 | Personal -> | Personal Account -> | Receiving cash from Business -> | The Receiver -> | Debit |

| Cash -> | Assets -> | Real Account -> | Goes out from business -> | What goes out -> | Credit |

*2 Note:- In this transaction, we can not credit the name of the Owner in the books of business because anything withdrawal by the owner from the business is known as drawing. So, we have to create an account named drawing and debit it.

Another Example

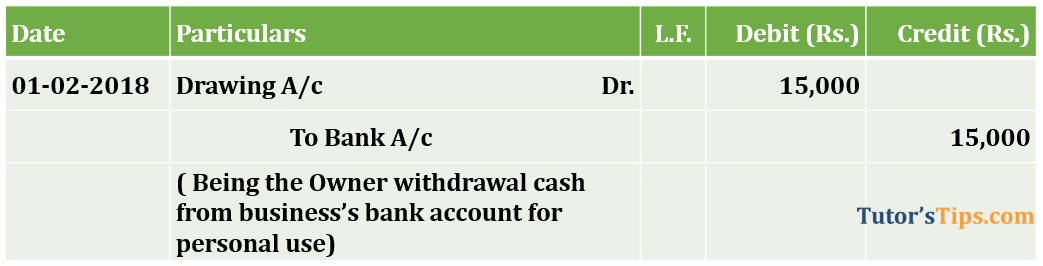

05/02/2018 Life Insurance Premium of the owner’s life Rs. 15,000 Paid by cheque.

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

| Drawing->*2 | Personal -> | Personal Account -> | Receiving cash from Business -> | The receiver -> | Debit |

| Bank->*3 | Personal -> | Personal Account -> | Paid Cash to Insurance Company -> | The giver -> | Credit |

*3 Note:- Bank is an Artificial person. So, that’s why we are applying Personal Rule on it.

All expenses met by the business for the owner’s personal use will be treated as same. the only name of the account will be charged.

like Following Examples:-

- Income Tax paid on income of the owner by the business.

- School or college fees of the children of the owner paid by the business.

- Household expenses paid by the business.

3. Purchase of Goods/Inventories:

When Business buy only goods is known as a purchase. When businesses buying any other assets than it is not treated as a purchase.

Subscribe to our Youtube Channel

Check the meaning of Goods Click Here and Purchase Click Here

Example:

05/02/2018 Purchase of Goods for Rs 50,000/-

Or

05/02/2018 Purchase of Goods for Rs 50,000/- for Cash

Both transactions are cash transaction will be treated as below:

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

| Purchase ->*4 | Expense-> | Nominal Account -> | Spending money on goods -> | All Expenses and losses -> | Debit |

| Cash->*5 | Asset -> | Real Account -> | Paid Cash to Supplier -> | What goes out -> | Credit |

*4 Note: when we purchase goods then purchase accounts will be created not a goods account.

*5 Note: if there is nothing given about payment mode then we have to assume that payment was made by cash only.

If the name of the person or company given in the transaction and if not cleared about payment then we will treat this transaction as credit business transaction.

like:

05/02/2018 Purchase goods from Ram & sons for Rs 50,000/-

Here Purchase will be treated as same as above

but instead of cash, we have to treat Ram & sons account like as below:

Ram & Sons -> Personal -> Personal Rule-> Ram & Sons is Supplied goods -> The giver -> Credit.

The Journal Entry will be as the following

If the name of the person or company given in the transaction and if cleared about payment then we will treat this transaction as cash business transaction.

like:

05/02/2018 Purchase goods from Ram & sons for Rs 50,000/- paid by cheque.

Here Purchase will be treated as same as above

but instead of Ram & sons, we have to treat Bank account because the payment was made by cheque (click here to know the meaning of cheque – wiki) like as below:

Bank a/c -> Personal -> Personal Rule-> Made Payment from bank -> the giver -> Credit.

The Journal Entry will be as the following

4. Sale of Goods:

When a business sells goods are treated as Sale in accounting books. When selling any other assets than it is not treated as Sale.

Check the meaning of Sale Click Here

Example:

05/02/2018 Sold Goods for Rs 20,000/-

Or

05/02/2018 Sold Goods for Rs 20,000/- for cash.

Both transactions are cash transaction will be treated as below:

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

| Cash-> | Asset -> | Real Account -> | Received Cash from Customer-> | What comes in -> | Debit |

| Sale-> *6 | Income -> | Nominal Account -> | Earned money from the selling of goods -> | All incomes and gains -> | Credit |

*6 Note: when we Sold goods then the Sales account will be created not a goods account.

If the name of the person or company given in the transaction and if not cleared about payment then we will treat this transaction as credit business transaction.

like:

05/02/2018 Sold Goods for Rs 20,000/- to Sham & Sons Ltd.

Here Sale will be treated as same as above

but instead of cash, we have to treat Sham & Sons Ltd. account like as below:

Sham & Sons Ltd. -> Personal -> Personal Rule-> Sham & sons ltd is buying goods ->The receiver -> Debit

The Journal Entry will be as the following

If the name of the person or company given in the transaction and if cleared about payment then we will treat this transaction as cash business transaction.

like:

05/02/2018 Sold Goods for Rs 20,000/- to Sham & Sons Ltd and paid by cheque.

Here Sale will be treated as same as above

but instead of cash, we have to treat Sham & Sons Ltd. account like as below:

Bank A/c. -> Personal -> Personal Rule-> Payment received in Bank account -> The receiver -> Debit

The Journal Entry will be as the following

5.Purchase of Assets

The assets are those valuable things or properties which the business or individual owns and get the benefits from it in the future or use it in generating income.

Subscribe our Youtube Channel

Example:

05/02/2018 Computer Purchased for Rs 55,000/-

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

| Computer -> | Asset -> | Real Account -> | Purchased Computer -> | What comes in -> | Debit |

| Cash-> | Asset -> | Real Account -> | Paid Cash to Supplier -> | What goes out -> | Credit |

If the name of the person or company given in the transaction and if not cleared about payment then we will treat this transaction as credit business transaction.

like:

05/02/2018 Computer Purchased for Rs 55,000/- from A&b Computers Pvt. Ltd.

In this Transaction, Purchase of an asset will be treated as same as given above

but instead of cash, we have to treat A&b Computers Pvt. Ltd. account like as below:

A&b Computers Pvt. Ltd. -> Personal -> Personal Rule->A&b Computers Pvt. Ltd. Supplied computer -> The giver -> Credit.

The Journal Entry will be as the following

If the name of the person or company given in the transaction and if cleared about payment then we will treat this transaction as cash business transaction.

like:

05/02/2018 Computer Purchased for Rs 55,000/- from A&b Computers Pvt. Ltd. paid by cheque.

Here Purchase will be treated as same as above

but instead of A&b Computers Pvt. Ltd, we have to treat Bank account because the payment was made by cheque(click here to know the meaning of check from wiki) like as below:

Bank a/c -> Personal -> Personal Rule-> Made Payment form Bank -> The giver -> Credit.

The Journal Entry will be as the following

Expenses met on the purchase of an asset or convert it into working condition, All these expenses will be added to the cost of the assets

For Example

Second-hand machine purchase for Rs. 50,000/- and paid transportation Rs 2,500/-, Installation charges 5,000/- and repair 2,500/-,

Now, the whole entry will remain the same but the only value of an asset will be changed.

Total Value of Assets = Purchase Value of Assets + All expenses

The amount will be debited to Machine account is Rs 60,000/- ( 50000+2500+5000+2500).

6. Sale of Assets

In the sale of an asset we have to calculate Profit/Loss on the sale of an asset shown below:

Profit or Loss on Sale of asset = Sale Price of an Asset – Book value of an Asset

Book Value of as Asset = Cost/Purchase Price of Assets – Depreciation charged until the date of sale of an asset

Example:

05/02/2018 Old Machine cost price 1,00,000/- sold for rs 50,000/-. depreciation charged till date Rs 60,000/-

BV = CP-Dep.

1,00,000-60,000 = 40,000/-

P/L = SP – BV

50,000 – 40,000 = 10,000/-

Here. in this entry we will treat 3 accounts:

- Asset A/c,

- Profit on Sale of Asset A/c

- Cash A/c

Credit and Cash transaction are treated as same as Journal Entries for the purchase of assets.

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

| Cash-> | Asset -> | Real Account -> | Cash Received form buyer-> | What comes in -> | Debit |

| Machine -> | Asset -> | Real Account -> | Sold old machine -> | What goes out -> | Credit |

| Profit on sale of Asset-> | Gain -> | Nominal Account -> | Business earn the gain on sale of Asset-> | All income and gains -> | Credit |

7. Expenses: –

Expenses mean the amount spent by the business for running the business operation. The expenses are also known as Revenue Expenditure.

Subscribe our Youtube Channel

Example:

10/02/2018 Salary Paid to employees for Rs. 10,000/-

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

| Salary-> | Expense -> | Nominal Account -> | Spending money to pay salary-> | All expenses and losses -> | Debit |

| Cash->*5 | Asset -> | Real Account -> | Paid cash to Employees -> | What goes out -> | Credit |

Name of Expenses like:

- Wages

- Rent

- Commission paid on Turnover

- Freight

- Transportation

- Trade Expenses

- Sundry charges

- Municipal Tax

- Legal Charges

- Audit Fee

- Commission to Agent

- Insurance Premium paid for Insurance of Building/Factory/Machinery/Vehicle

- Repair and maintenance of the building, electricity, plant, machine, computer etc.

- Staff Welfare

- Travelling Expenses

- Printing and Stationery

- Mobile and Telephone

- Postage and Stamps

- Loading and Unloading

- Labour Charges

- Electricity charges

- Consumable items

- Fuel and Power

- Marketing Expenses

- Advertisement

- Donation and Charity

- Medical Expenses for Employees

- Bonuses

- Etc.

8. Incomes

Check the meaning of Income Click Here

Example:

10/02/2018 Rent received from sublet property for Rs. 10,000/-

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

| Cash-> | Asset -> | Real Account -> | Received Cash from Tenent -> | What comes in -> | Debit |

| Rent Received -> | Income -> | Nominal Account -> | Earned money from Building -> | All income and gains -> | Credit |

Name of Income like:

- Sale of Goods

- Services Rendered

- Commission Received

- Subsidy by Govt.

- Tax Rebate

- Rebate on Electricity Bill

- Interest on Investment

Thanks for reading the topic of Basic Journal Entries, please comment your feedback whatever you want.

Or

If you have any question please ask us by commenting.

Please Share and spread it.