Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

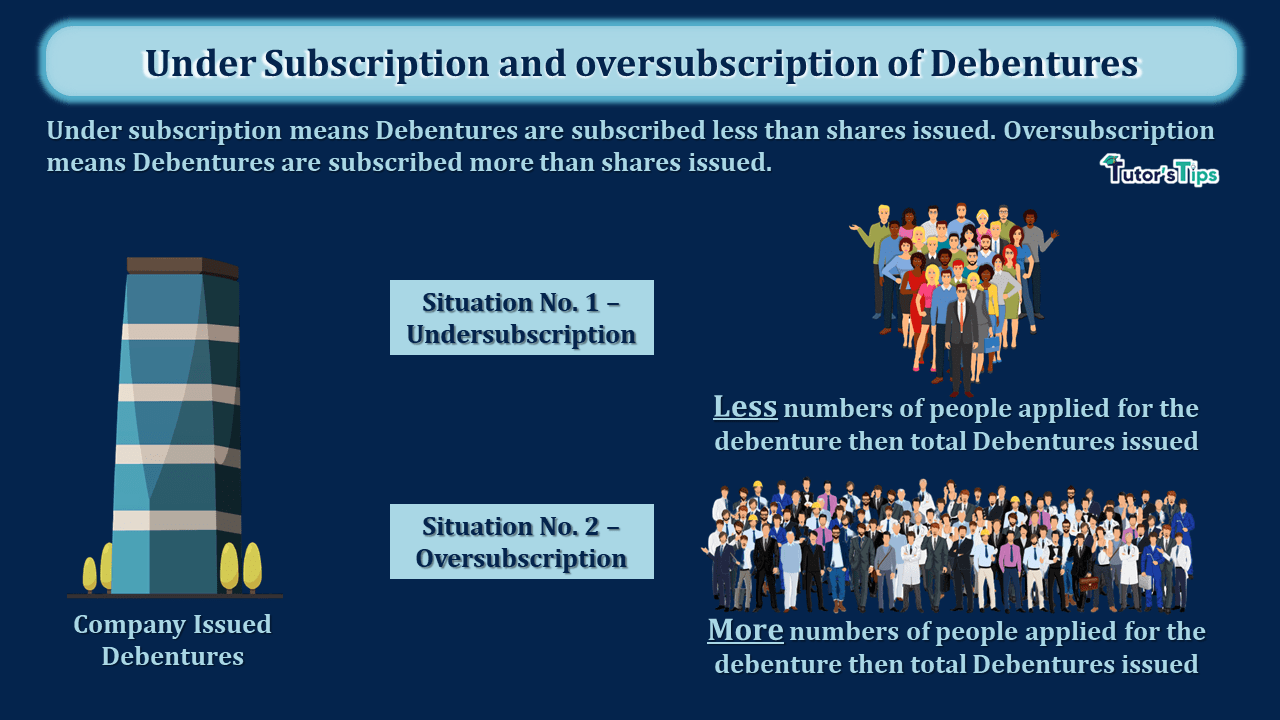

Under Subscription and oversubscription of Debentures are opposite terms to each other. Under subscription is used when Debentures are subscribed less than the number of Debentures issued but oversubscription is used when Debentures are subscribed more than the number of Debentures issued.

Under Subscription means less number of Debentures subscribed by the public than the number of Debentures issued. In this case, the same accounting treatment will be followed and just treated all journal entries with an actual subscribed number of Debentures.

ABC limited issued 1,00,000 9% Debentures @ 15 each but public subscribed 95,000 Debentures only.

So, In this case, is known as under subscription of Debentures, and the company will pass all journal entries and make the next calls for subscribed Debentures i.e. 95,000 shares.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| Discount on Issue of Deb. A/c | Dr. | *** | |||

| To Debenture Application A/c | ***** | ||||

| (Being share application money received) | |||||

| Debenture Application A/c | Dr. | ***** | |||

| To ___% Debenture A/c | ***** | ||||

| To Securities Premium A/c[If any] | *** | ||||

| (Being Debenture allotted and securities premium created (if issued at a premium)against the payment received on Debenture application) | |||||

| Debenture Allotment A/c | Dr. | ***** | |||

| To ___% Debenture A/c | ***** | ||||

| To Securities Premium A/c[If any] | *** | ||||

| (Being Debenture allotted and securities premium created (if issued at a premium) against the payment received on Debenture application) | |||||

| Bank A/c | Dr. | ***** | |||

| Discount on Issue of Deb. A/c | Dr. | *** | |||

| To Debenture Allotement A/c | ***** | ||||

| (Being Debenture Allotment money received) | |||||

| Debenture 1st Call A/c | Dr. | ***** | |||

| To Debenture Capital A/c | ***** | ||||

| To Securities Premium A/c[If any] | *** | ||||

| (Being Debenture 1st call and securities premium created (if issued at a premium)against the payment received on Debenture 1st call) | |||||

| Bank A/c | Dr. | ***** | |||

| Discount on Issue of Den A/c | Dr. | *** | |||

| To Debenture 1st Call A/c | ***** | ||||

| (Being share 1st call money received) | |||||

| Debenture 2nd Call A/c | Dr. | ***** | |||

| To ___% Debenture A/c | ***** | ||||

| To Securities Premium A/c[If any] | *** | ||||

| (Being Debenture 2nd call and securities premium created (if issued at a premium) against the payment received on Debenture 2nd call) | |||||

| Bank A/c | Dr. | ***** | |||

| Discount on Issue of Shares A/c | Dr. | *** | |||

| To Debenture 2nd Call A/c | ***** | ||||

| (Being Debenture 2nd Call money received) | |||||

| So on................... | |||||

Note: - All types of accounting journal entries are shown in the previous article which is shown as follows:

https://tutorstips.com/issue-of-debenture-methods-and-accounting-treatment/

Oversubscription of shares means more number of Debentures subscribed by the public than the number of Debentures issued. In this case, the different accounting treatments will be followed but remember one thing always that you can not allot full Debentures because the company can only allot the Debentures up to the number of Debentures actually issued. So, In this situation, the company has to adopt one of the following three methods:

This is a simple way to tackle the situation when the company received more applications for the subscription of Debentures. The company can decide to allot Debentures only to those individuals or corporations that applied more than a specific number of Debentures and who applied for less number of Debentures from this specific limit their application will be rejected and application money will be refunded to them.

In this method, The company will be allotted the Debentures on a pro-rata basis. It means the company will be allotted the specific number of Debentures against the specific number of applied Debentures i.e. 3 number of Debentures will be allotted against 5 number of Debentures applied by the subscriber. The excess amount will be adjusted with the next calls or treated as calls in advance.

In this method, The company will be allotted the Debentures on a pro-rata basis as well as reject some of the application which is below from specific limit decided by the company. The excess numbers of Debentures whose allotment is allowed on the pro-rata basis will be adjusted with the next calls or treated as calls in advance and the excess amount of rejected applications will be refunded.

Example of oversubscription of shares:

ABC limited issued 1,00,000 Debentures @ 10 each but public subscribed 1,15,000 shares only.

So, In this case, is known as oversubscription of Debentures, and the company will pass all journal entries and make the next calls for up to issued Debentures i.e. 1,00,000 Debentures and adjust or refund the balance amount.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| Discount on Issue of Deb. A/c | Dr. | *** | |||

| To Debentures App. A/c | ***** | ||||

| (Being Debentures application money received) | |||||

| Debentures Application A/c | Dr. | ***** | |||

| To ___% Debentures A/c | ***** | ||||

| To Securities Premium A/c[If any] | *** | ||||

| To Bank A/c | *** | ||||

| To Debentures Allt. A/c [If any] | *** | ||||

| To Calls in Advance A/c [if any] | *** | ||||

| (Being Debenture allotted and securities premium created (if issued at a premium)against the payment received on Debentures application) | |||||

This is all about Under Subscription and oversubscription of Debenture and The adjustment amount will be treated as calls in advance please check the following article of calls in advance for other journal entries:

https://tutorstips.com/calls-in-arrears-and-calls-in-advances/

Thanks for reading the topic.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Under Subscription and oversubscription of Debentures are opposite terms to each other. Under subscription is used when Debentures are subscribed less than the…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.