Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

To Opening Stock Account

To Purchase Account

To Wages Account

To Carriage inward Account

To Freight inward Account

(Being all expenses and Opening Stock related to Trading Account transferred)To Trading Account

(Being all Income and Closing Stock related to Trading Account transferred)To Purchase Account

(Being balance of purchase return account transferred to purchase account) (ii) In the case of Sale return or return inwards Sales Account Dr.To Sales Returns Account

(Being balance of Sale return account transferred to Sale account)To Purchase Account

(Being goods withdrawal by the owner not recorded yet transferred to purchase account)To Purchase Account

(Being goods distribute as Donation not recorded yet transferred to purchase account)To Profit/Loss A/c

(Being gross profit transferred to profit/loss account ) (i) In the case of Gross loss Profit/Loss A/c Dr.To Trading A/c

(Being gross loss transferred to profit/loss account )

Note : - if the total of Credit side excess over Debit side = Gross Profit if the total of Debit side excess over Credit side = Gross Loss

| Stock as on 01/04/2015 | 10,000 |

| Purchases | 2,00,000 |

| Freight | 15,000 |

| Wages | 50,000 |

| Carriage | 10,000 |

| Sales | 3,20,000 |

| Return Inward | 10,000 |

| Return outward | 20,000 |

| Stock as on 31/03/2018 | 20,000 |

Tutorstips Ltd.

Journal book

| Date | Particulars | L.F. | Debit | Credit |

|---|---|---|---|---|

| Trading A/c Dr. | 285,000 | |||

| To Opening Stock a/c | 10,000 | |||

| To Purchase a/c | 200,000 | |||

| To Freight | 15,000 | |||

| To Wages | 50,000 | |||

| To Carriage | 10,000 | |||

| (Being all expenses and Opening Stock related to Trading Account transferred) | ||||

| Sales a/c Dr. | 320,000 | |||

| Closing Stock Dr. | 20,000 | |||

| To Trading a/c | 340,000 | |||

| (Being all Income and Closing Stock related to Trading Account transferred) | ||||

| Sale a/c Dr. | 10,000 | |||

| To Return Inward a/c | 10,000 | |||

| (Being balance of Sale return account transferred to Sale account) | ||||

| Return outward Dr. | 20,000 | |||

| To Purchase a/c | 20,000 | |||

| (Being balance of purchase return account transferred to purchase account) | ||||

| Trading Account Dr. | 75,000 | |||

| To Profit/Loss Account | 75,000 | |||

| (Being gross profit transferred to profit/loss account ) | ||||

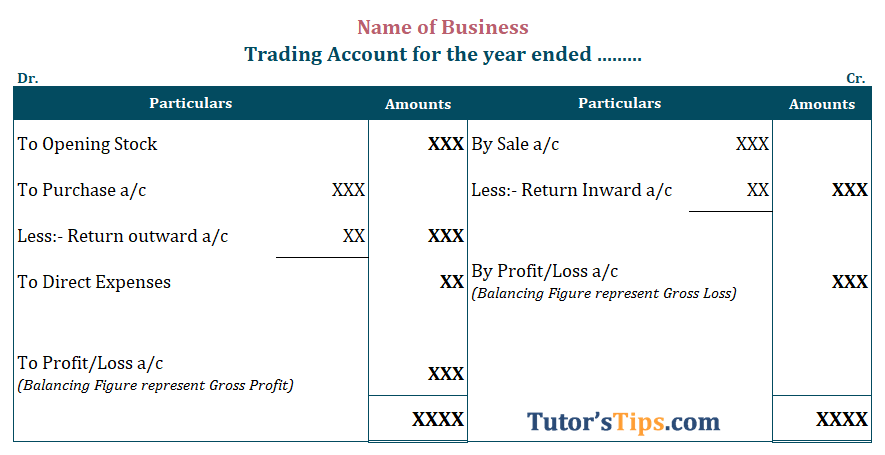

Tutorstips Ltd.

Trading Account as on March 31, 2018

| Dr. | Cr. | ||||

| Particulars | Amount | Particulars | Amount | ||

|---|---|---|---|---|---|

| To Opening Stock | 10,000 | By Sale a/c | 320,000 | ||

| To Purchase a/c | 200,000 | Less: - Return Inward a/c | 10,000 | 310,000 | |

| Less: - Return outward | 20,000 | 180,000 | By Closing Stock | 20,000 | |

| To Freight | 15,000 | ||||

| To Wages | 50,000 | ||||

| To Carriage | 10,000 | ||||

| To Profit/Loss a/c (Balancing Figure represent Gross Profit) | 75,000 | ||||

| 330,000 | 330,000 | ||||

Or

If you want to download the above illustration please download this following image:| Stock as on 01/04/2015 | 30,000 |

| Purchases | 1,00,000 |

| Freight | 10,000 |

| Wages | 70,000 |

| Carriage | 20,000 |

| Sales | 1,70,000 |

| Return Inward | 30,000 |

| Return outward | 25,000 |

| Stock as on 31/03/2018 | 40,000 |

Aman Enterprise Ltd.

Journal book

| Date | Particulars | L.F. | Debit | Credit |

|---|---|---|---|---|

| Trading A/c Dr. | 285,000 | |||

| To Opening Stock a/c | 30,000 | |||

| To Purchase a/c | 100,000 | |||

| To Freight | 10,000 | |||

| To Wages | 70,000 | |||

| To Carriage | 20,000 | |||

| (Being all expenses and Opening Stock related to Trading Account transferred) | ||||

| Sales a/c Dr. | 170,000 | |||

| Closing Stock Dr. | 40,000 | |||

| To Trading a/c | 210,000 | |||

| (Being all Income and Closing Stock related to Trading Account transferred) | ||||

| Sale a/c Dr. | 30,000 | |||

| To Return Inward a/c | 30,000 | |||

| (Being balance of Sale return account transferred to Sale account) | ||||

| Return outward Dr. | 25,000 | |||

| To Purchase a/c | 25,000 | |||

| (Being balance of purchase return account transferred to purchase account) | ||||

| Profit/Loss Account Dr. | 75,000 | |||

| To Trading Account | 75,000 | |||

| (Being gross loss transferred to profit/loss account ) | ||||

Aman Enterprise Ltd.

Trading Account as on March 31, 2018

| Dr. | Cr. | ||||

| Particulars | Amount | Particulars | Amount | ||

|---|---|---|---|---|---|

| To Opening Stock | 30,000 | By Sale a/c | 170,000 | ||

| To Purchase a/c | 100,000 | Less: - Return Inward a/c | 30,000 | 140,000 | |

| Less: - Return outward | 25,000 | 75,000 | By Closing Stock | 40,000 | |

| To Freight | 10,000 | ||||

| To Wages | 70,000 | By Profit/Loss a/c (Balancing Figure represent Gross Loss) | 25,000 | ||

| To Carriage | 20,000 | ||||

| 205,000 | 205,000 | ||||

Or

If you want to download the above illustration please download this following image:Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

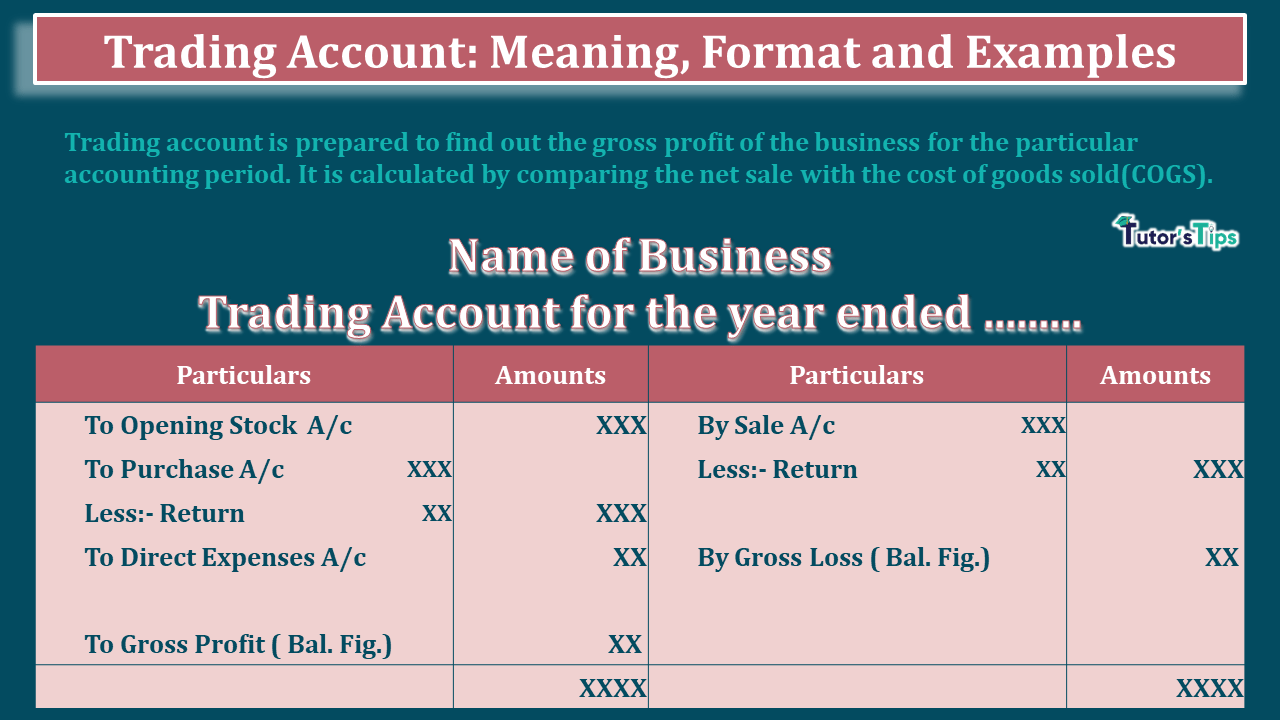

Meaning of Trading Account: - Trading account is prepared to find out the gross profit of the business for the particular accounting period. It is calculated…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.

30 August 2020

27 February 2022

27 February 2022

27 February 2022

27 February 2022

4 December 2022

22 December 2022

8 January 2023