Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

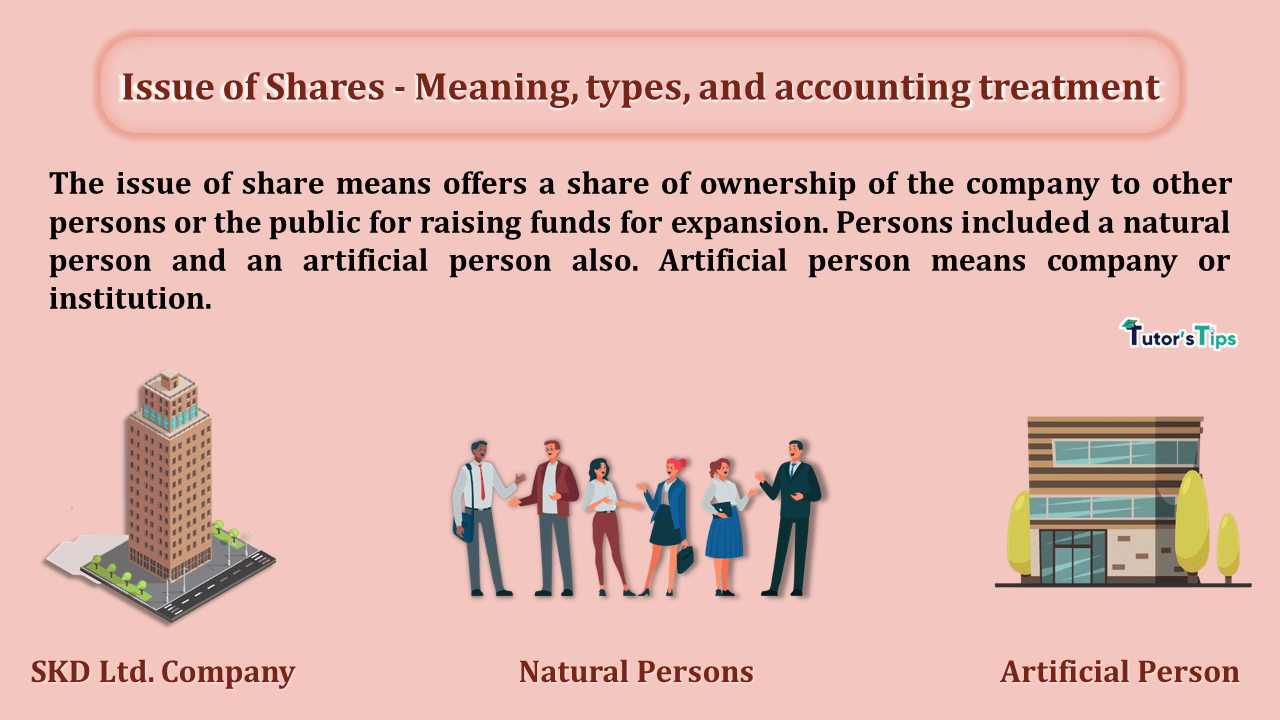

The Issue of Shares refers to raising funds from other persons or groups of persons for the expansion of a business/company.

It means offers a share of ownership of the company(Share Capital) to other persons or the public for raising funds for expansion. Persons included a natural person and an artificial person also. Artificial person means company or institution. Any business can issue its share capital by following the steps:

Every company can issue shares in the market in the following two ways:

When the company issue shares in the share market to subscribe. These activities can be performed by the company which is registered as a public limited company under the Companies Act, 2013.

When the company issue shares to subscribe to a small number of investors. Investors can be individuals or other companies. These activities can be performed by the company which is registered as a Private limited company under the Companies Act, 2013.

The accounting treatment of issued shares is on the basis of the following:

The shares can be issued for cash in the two following ways and there two have different accounting treatment as shown following:

When the company called up full share price including premium or discount at the time of application, the shares are said to be issued against lump-sum payment. The accounting treatment of this is shown as follows:

It can be issued in three ways :

When shares are issued at the face value.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| To Share App. and Allot. A/c | ***** | ||||

| (Being share application and allotment money received) | |||||

| Share App. and Allot. A/c | Dr. | ***** | |||

| To Share Capital A/c | ***** | ||||

| (Being Shares allotted against the payment received on share application and allotment) | |||||

At par means when shares are issued at less than their face value.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| Discount on Issue of Shares A/c | Dr. | *** | |||

| To Share App. and Allot. A/c | ***** | ||||

| (Being share application and allotment money received and discount allowed) | |||||

| Share App. and Allot. A/c | Dr. | ***** | |||

| To Share Capital A/c | ***** | ||||

| (Being Shares allotted against the payment received on share application and allotment) | |||||

When shares are issued at a higher price than their face value.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| To Share App. and Allot. A/c | ***** | ||||

| (Being share application and allotment money received) | |||||

| Share App. and Allot. A/c | Dr. | ***** | |||

| To Share Capital A/c | ***** | ||||

| To Securities Premium A/c | *** | ||||

| (Being Shares allotted and securities premium created against the payment received on share application and allotment) | |||||

When the company called up full share price including premium or discount in the instalments i.e., partly on Application, partly on Allotment and balance in the one or more calls, the shares are said to be issued in the instalments. The name of these instalments are must be as following :

1st Instalment: Shares Application

2nd Instalment: Shares Allotment

3rd Instalment: Shares 1st Calls

4th Instalment: Shares 2nd Calls (If any)

and So on.

The accounting treatment of this is shown as follows:

We have shown the share issued at par, at a discount and at a premium in the following single journal format and treatment of discount and premium are shown with grey colour so if in the question there is discount then u can add discount treatment and do not write a premium treatment and vice versa.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| Discount on Issue of Shares A/c | Dr. | *** | |||

| To Shares Application A/c | ***** | ||||

| (Being share application money received) | |||||

| Shares Application A/c | Dr. | ***** | |||

| To Share Capital A/c | ***** | ||||

| To Securities Premium A/c[If any] | *** | ||||

| (Being Shares allotted and securities premium created (if issued at a premium)against the payment received on share application) | |||||

| Shares Allotment A/c | Dr. | ***** | |||

| To Share Capital A/c | ***** | ||||

| To Securities Premium A/c[If any] | *** | ||||

| (Being Shares allotted and securities premium created (if issued at a premium) against the payment received on share application) | |||||

| Bank A/c | Dr. | ***** | |||

| Discount on Issue of Shares A/c | Dr. | *** | |||

| To Shares Allotement A/c | ***** | ||||

| (Being share Allotment money received) | |||||

| Shares 1st Call A/c | Dr. | ***** | |||

| To Share Capital A/c | ***** | ||||

| To Securities Premium A/c[If any] | *** | ||||

| (Being Shares 1st call and securities premium created (if issued at a premium)against the payment received on share 1st call) | |||||

| Bank A/c | Dr. | ***** | |||

| Discount on Issue of Shares A/c | Dr. | *** | |||

| To Shares 1st Call A/c | ***** | ||||

| (Being share 1st call money received) | |||||

| Shares 2nd Call A/c | Dr. | ***** | |||

| To Share Capital A/c | ***** | ||||

| To Securities Premium A/c[If any] | *** | ||||

| (Being Shares 2nd call and securities premium created (if issued at a premium)against the payment received on share 2nd call) | |||||

| Bank A/c | Dr. | ***** | |||

| Discount on Issue of Shares A/c | Dr. | *** | |||

| To Shares 2nd Call A/c | ***** | ||||

| (Being share 2nd Call money received) | |||||

| So on................... | |||||

Note:

The company can call the amount of premium with any call. So with which it is called, you have to record with that call. But we had shown treatment with all calls.

When the company issued share against the consideration other than cash i.e., for any assets or the whole business, the shares are said to be issued for consideration other than cash. The accounting treatment of this is shown as follows:

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Name of Assets/Company A/c | Dr. | ***** | |||

| Discount on Issue of Shares A/c | Dr. | *** | |||

| To Share Capital A/c | ***** | ||||

| To Securities Premium a/c | *** | ||||

| (Being Shares Allotted against the purchase of assets or other running company. | |||||

Thanks for reading the topic.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

The Issue of Shares refers to raising funds from other persons or groups of persons for the expansion of a business/company. What is the Issue of Shares? It…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.