Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

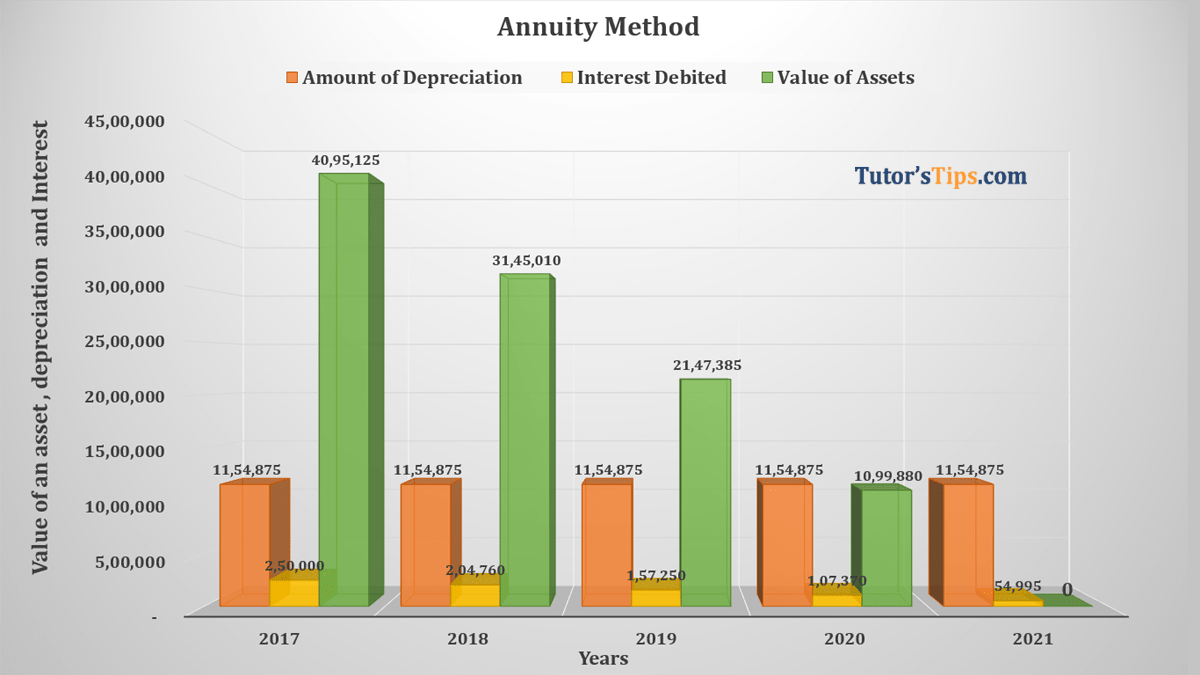

| Year ended | Opening balance of an asset | Interest Debited | Amount of depreciation | The closing balance of an asset |

| 31-03-2017 | 50,00,000 | 2,50,000 | 11,54,875 | 40,95,125 |

| 31-03-2018 | 40,95,125 | 2,04,760 | 11,54,875 | 31,45,010 |

| 31-03-2019 | 31,45,010 | 1,57,250 | 11,54,875 | 21,47,385 |

| 31-03-2020 | 21,47,385 | 1,07,370 | 11,54,875 | 10,99,880 |

| 31-03-2021 | 10,99,880 | 54,995 | 11,54,875 | 0 |

| Date | Particulars | L.F. | Debit | Credit | ||

|---|---|---|---|---|---|---|

| 1st Year | ||||||

| 2016-17 | ||||||

| 01-Apr | Lease A/c | Dr. | 50,00,000 | |||

| To Bank A/c | 50,00,000 | |||||

| (Being land purchased on lease ) | ||||||

| 31-Mar | Lease A/c | Dr. | 2,50,000 | |||

| To Interest A/c | 2,50,000 | |||||

| (Being Interest @ 5% charged on the closing balance of an asset) | ||||||

| 31-Mar | Depreciation A/c | Dr. | 11,54,875 | |||

| To Lease A/c | 11,54,875 | |||||

| (Being Depreciation on asset charged) | ||||||

| 31-Mar | Profit or loss A/c | Dr. | 11,54,875 | |||

| To Depreciation A/c | 11,54,875 | |||||

| (Being Depreciation transfer to P&L A/c) | ||||||

| 2nd Year | ||||||

| 2017-18 | ||||||

| 31-Mar | Lease A/c | Dr. | 2,04,760 | |||

| To Interest A/c | 2,04,760 | |||||

| (Being Interest @ 5% charged on the closing balance of an asset) | ||||||

| 31-Mar | Depreciation A/c | Dr. | 11,54,875 | |||

| To Lease A/c | 11,54,875 | |||||

| (Being Depreciation on asset charged) | ||||||

| 31-Mar | Profit or loss A/c | Dr. | 11,54,875 | |||

| To Depreciation A/c | 11,54,875 | |||||

| (Being Depreciation transfer to P&L A/c) | ||||||

| 3rd Year | ||||||

| 2017-18 | ||||||

| 31-Mar | Lease A/c | Dr. | 1,57,250 | |||

| To Interest A/c | 1,57,250 | |||||

| (Being Interest @ 5% charged on the closing balance of an asset) | ||||||

| 31-Mar | Depreciation A/c | Dr. | 11,54,875 | |||

| To Lease A/c | 11,54,875 | |||||

| (Being Depreciation on asset charged) | ||||||

| 31-Mar | Profit or loss A/c | Dr. | 11,54,875 | |||

| To Depreciation A/c | 11,54,875 | |||||

| (Being Depreciation transfer to P&L A/c) | ||||||

| 4th Year | ||||||

| 2017-18 | ||||||

| 31-Mar | Lease A/c | Dr. | 1,07,370 | |||

| To Interest A/c | 1,07,370 | |||||

| (Being Interest @ 5% charged on the closing balance of an asset) | ||||||

| 31-Mar | Depreciation A/c | Dr. | 11,54,875 | |||

| To Lease A/c | 11,54,875 | |||||

| (Being Depreciation on asset charged) | ||||||

| 31-Mar | Profit or loss A/c | Dr. | 11,54,875 | |||

| To Depreciation A/c | 11,54,875 | |||||

| (Being Depreciation transfer to P&L A/c) | ||||||

| 5th Year | ||||||

| 2017-18 | ||||||

| 31-Mar | Lease A/c | Dr. | 54,995 | |||

| To Interest A/c | 54,995 | |||||

| (Being Interest @ 5% charged on the closing balance of an asset) | ||||||

| 31-Mar | Depreciation A/c | Dr. | 11,54,875 | |||

| To Lease A/c | 11,54,875 | |||||

| (Being Depreciation on asset charged) | ||||||

| 31-Mar | Profit or loss A/c | Dr. | 11,54,875 | |||

| To Depreciation A/c | 11,54,875 | |||||

| (Being Depreciation transfer to P&L A/c) | ||||||

Lease Account

| Date | Particulars | Amount | Date | Particulars | Amount |

|---|---|---|---|---|---|

| 01-04-2017 | To Bank A/c | 50,00,000 | 31-03-2018 | By Depreciation A/c | 11,54,875 |

| 31-03-2018 | To Interest A/c | 2,50,000 | 31-03-2018 | By Balance C/d | 40,95,125 |

| 52,50,000 | 52,50,000 | ||||

| 01-04-2018 | To Balance B/d | 40,95,125 | 31-03-2019 | By Depreciation A/c | 11,54,875 |

| 31-03-2019 | To Interest A/c | 2,04,760 | 31-03-2019 | By Balance C/d | 31,45,010 |

| 42,99,885 | 42,99,885 | ||||

| 01-04-2019 | To Balance B/d | 31,45,010 | 31-03-2020 | By Depreciation A/c | 11,54,875 |

| 31-03-2020 | To Interest A/c | 1,57,250 | 31-03-2020 | By Balance C/d | 21,47,385 |

| 33,02,260 | 33,02,260 | ||||

| 01-04-2020 | To Balance B/d | 21,47,385 | 31-03-2021 | By Depreciation A/c | 11,54,875 |

| 31-03-2021 | To Interest A/c | 1,07,370 | 31-03-2021 | By Balance C/d | 10,99,880 |

| 22,54,755 | 22,54,755 | ||||

| 01-04-2021 | To Balance B/d | 10,99,880 | 31-03-2022 | By Depreciation A/c | 11,54,875 |

| 31-03-2022 | To Interest A/c | 54,995 | 31-03-2022 | By Balance C/d | 0 |

| 11,54,875 | 11,54,875 | ||||

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Annuity Method: In Annuity method, we will calculate a fixed amount of depreciation on the original cost of an asset but also calculate interest on the…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.

14 October 2020