Question No 4 Chapter No 9

Journalise the following transactions book of Afzal, Kolkata and post them in the ledger:

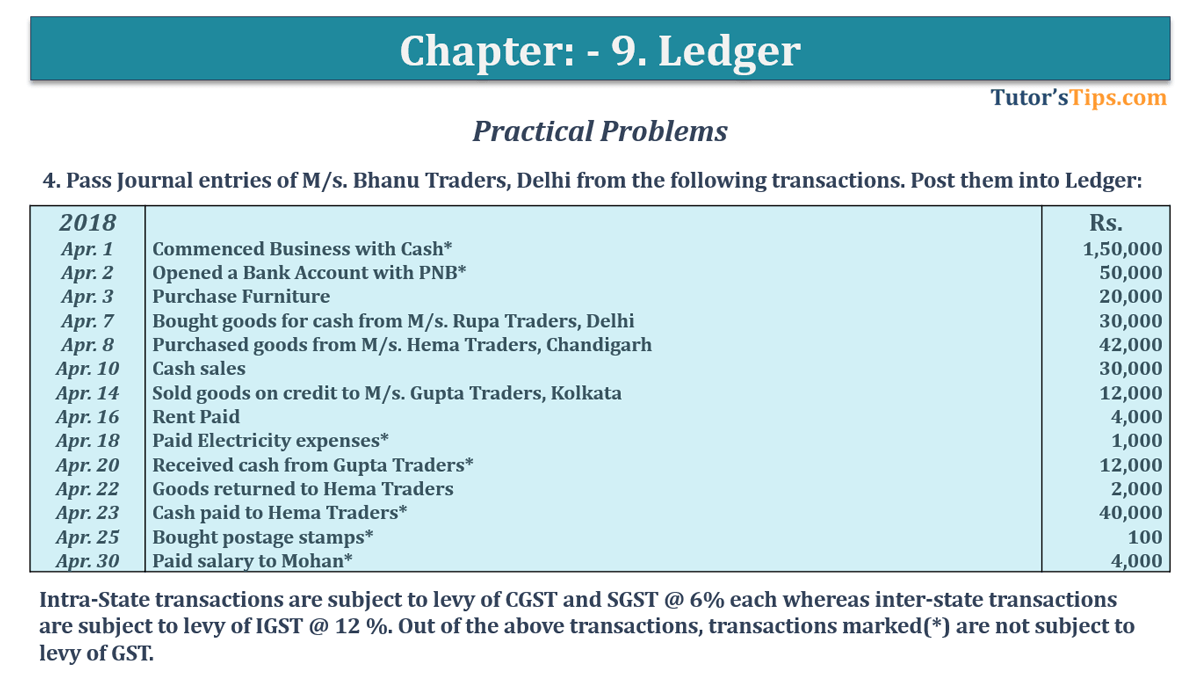

| 2018 | Rs. | |

| Apr. 1 | Commenced Business with Cash* | 1,50,000 |

| Apr. 2 | Opened a Bank Account with PNB* | 50,000 |

| Apr. 3 | Purchase Furniture | 20,000 |

| Apr. 7 | Bought goods for cash from M/s. Rupa Traders, Delhi | 30,000 |

| Apr. 8 | Purchased goods from M/s. Hema Traders, Chandigarh | 42,000 |

| Apr. 10 | Cash sales | 30,000 |

| Apr. 14 | Sold goods on credit to M/s. Gupta Traders, Kolkata | 12,000 |

| Apr. 16 | Rent Paid | 4,000 |

| Apr. 18 | Paid Electricity expenses* | 1,000 |

| Apr. 20 | Received cash from Gupta Traders* | 12,000 |

| Apr. 22 | Goods returned to Hema Traders | 2,000 |

| Apr. 23 | Cash paid to Hema Traders* | 40,000 |

| Apr. 25 | Bought postage stamps* | 100 |

| Apr. 30 | Paid salary to Mohan* | 4,000 |

Intra-State transactions are subject to levy of CGST and SGST @ 6% each whereas inter-state transactions are subject to levy of IGST @ 12 %. Out of the above transactions, transactions marked(*) are not subject to levy of GST.

Solution of Question No 4 Chapter No 9: –

In the Books of Afzal, Kolkata

| Date | Particulars |

L.F. | Debit | Credit | |

| 2018 | |||||

| Apr. 1 | Cash A/c | Dr. | 1,50,000 | ||

| To Capital A/c | 1,50,000 | ||||

| (Being Commenced business with cash.) | |||||

| Apr. 2 | Bank – PNB A/c | Dr. | 50,000 | ||

| To Cash A/c | 50,000 | ||||

| (Being Bank account opened in PNB) | |||||

| Apr. 3 | Furniture A/c | Dr. | 20,000 | ||

| Input CGST A/c | Dr. | 1,200 | |||

| Input SGST A/c | Dr. | 1,200 | |||

| To Cash A/c | 22,400 | ||||

| (Being Furniture purchased for cash ) | |||||

| Apr. 7 | Purchase A/c | Dr. | 30,000 | ||

| Input CGST A/c | Dr. | 1,800 | |||

| Input SGST A/c | Dr. | 1,800 | |||

| To Cash A/c | 33,600 | ||||

| (Being goods purchased for cash ) | |||||

| Apr. 8 | Purchase A/c | Dr. | 42,000 | ||

| Input IGST A/c | Dr. | 5,040 | |||

| To M/s Hema Traders, CHD A/c | 47,040 | ||||

| (Being goods purchased for cash ) | |||||

| Apr. 10 | Cash A/c | Dr. | 33,600 | ||

| To Sales A/c | 30,000 | ||||

| To Output CGST A/c | 1,800 | ||||

| To Output SGST A/c | 1,800 | ||||

| (Being goods sold for cash) | |||||

| Apr. 14 | M/s. Gupta Traders, Kolkata A/c | Dr. | 13,440 | ||

| To Sales A/c | 12,000 | ||||

| To Output IGST A/c | 1,440 | ||||

| (Being goods sold for cash) | |||||

| Apr. 16 | Rent A/c | Dr. | 4,000 | ||

| Input CGST A/c | Dr. | 240 | |||

| Input SGST A/c | Dr. | 240 | |||

| To Cash A/c | 4,480 | ||||

| (Being Rent paid to Landlord) | |||||

| Apr. 18 | Electricity Charges A/c | Dr. | 1,000 | ||

| To Cash A/c | 1,000 | ||||

| (Being Electricity Charges paid) | |||||

| Apr. 20 | Cash A/c | Dr. | 12,000 | ||

| To M/s Gupta Traders A/c | 12,000 | ||||

| (Being payment received in cash) | |||||

| Apr. 22 | M/s. Hema Traders, CHD A/c | Dr. | 2,240 | ||

| To Pruchase Return A/c | 2,000 | ||||

| To Input IGST A/c | 240 | ||||

| (Being goods returned) | |||||

| Apr. 23 | M/s. Hema Traders, CHD A/c | Dr. | 40,000 | ||

| To Cash A/c | 40,000 | ||||

| (Being payment made to vendor) | |||||

| Apr. 25 | Postage & stamps A/c | Dr. | 100 | ||

| To Cash A/c | 100 | ||||

| (Being cash paid for postage & stamps) | |||||

| Apr. 30 | Salary A/c | Dr. | 4,000 | ||

| To Cash A/c | 4,000 | ||||

| (Being Salary paid) | |||||

To clear the meaning of Ledger and Ledger balancing Click below:

What is Ledger in accounting – explain its Types

Ledger balancing or Closing of ledger account | Ledger

| Dr. | Cash A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 1 | To Capital A/c | 1,50,000 | Apr. 2 | By Bank- PNB A/c | 50,000 | ||

| Apr. 5 | To Sales A/c | 33,600 | Apr. 11 | By Furniture A/c | 22,400 | ||

| Apr. 15 | To M/s Gupta Traders A/c | 12,000 | Apr. 13 | By Purchase A/c | 33,600 | ||

| Apr. 16 | By Rent A/c | 4,480 | |||||

| Apr. 18 | By Electricity A/c | 1,000 | |||||

| Apr. 23 | By Hema Traders A/c | 40,000 | |||||

| Apr. 25 | By Postage & Stamps A/c | 100 | |||||

| Apr. 30 | By SalaryA/c | 4,000 | |||||

| Apr. 30 | By Balance C/d | 40,020 | |||||

| 1,95,600 | 1,95,600 | ||||||

| Dr. | Capital A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 1 | By Cash A/c | 1,50,000 | |||||

| Apr. 30 | By Balance C/d | 1,50,000 | |||||

| 1,50,000 | 1,50,000 | ||||||

| Dr. | Bank – PNB A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 2 | To Cash A/c | 50,000 | |||||

| Apr. 30 | By Balance C/d | 50,000 | |||||

| 50,000 | 50,000 | ||||||

| Dr. | Furniture A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 3 | To Cash A/c | 22,400 | |||||

| Apr. 30 | By Balance C/d | 22,400 | |||||

| 22,400 | 22,400 | ||||||

| Dr. | Purchase A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 7 | To Cash A/c | 33,600 | |||||

| Apr. 8 | To M/s Hema Trader, Kolkata A/c | 47,040 | |||||

| Apr. 30 | By Balance C/d | 80,640 | |||||

| 80,640 | 80,640 | ||||||

| Dr. | Sales A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 10 | By Cash A/c | 33,600 | |||||

| Apr. 14 | By M/s Gupta Traders, CHD A/c | 13,440 | |||||

| Jan. 31 | By Balance C/d | 47,040 | |||||

| 47,040 | 47,040 | ||||||

| Dr. | M/s Hema Traders, Chandigarh A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Jan. 15 | To Sales A/c | 6,000 | |||||

| Jan. 31 | By Balance C/d | 6,000 | |||||

| 6,000 | 6,000 | ||||||

| Dr. | Anurag, Kanpur A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Jan. 19 | To Purchase Return A/c | 5,000 | Jan. 18 | By Purchase A/c | 50,000 | ||

| Jan. 31 | By Balance C/d | 45,000 | |||||

| 50,000 | 50,000 | ||||||

| Dr. | Purchase Return A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Jan. 19 | By Anurag, Kanpur A/c | 5,000 | |||||

| Jan. 31 | By Balance C/d | 5,000 | |||||

| 5,000 | 5,000 | ||||||

| Dr. | Electricity Charges A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Jan. 22 | To CashA/c | 1,000 | |||||

| Jan. 31 | By Balance C/d | 1,000 | |||||

| 1,000 | 1,000 | ||||||

| Dr. | Telephone Charges A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Jan. 28 | To CashA/c | 500 | |||||

| Jan. 31 | By Balance C/d | 500 | |||||

| 500 | 500 | ||||||

| Dr. | Rent A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Jan. 29 | To CashA/c | 800 | |||||

| Jan. 31 | By Balance C/d | 800 | |||||

| 800 | 800 | ||||||

| Dr. | Wages A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Jan. 31 | To CashA/c | 3,000 | |||||

| Jan. 31 | By Balance C/d | 3,000 | |||||

| 1,000 | 1,000 | ||||||

Thanks Please share with your friends

Comment if you have any question.

Check out perivous questions: –

- Question No 34 Chapter No 8 – T.S. Grewal 11 Class

- Question No 33 Chapter No 8 – T.S. Grewal 11 Class

- Question No 32 Chapter No 8 – T.S. Grewal 11 Class

- Question No 31 Chapter No 8 – T.S. Grewal 11 Class

- Question No 30 Chapter No 8 – T.S. Grewal 11 Class

T.S. Grewal’s Double Entry Book Keeping