Question No 2 Chapter No 11

Table of Contents

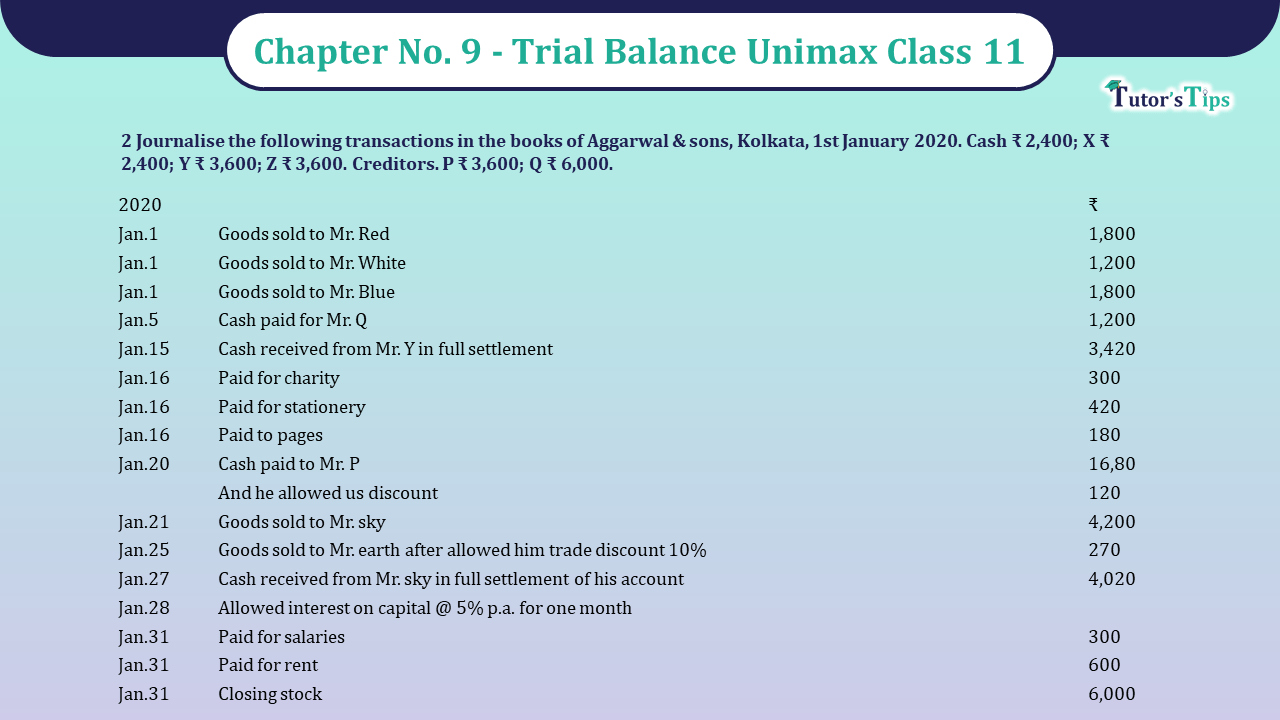

Journalise the following transactions in the books of Aggarwal & sons, Kolkata, 1st January 2020. Cash ₹ 2,400; X ₹ 2,400; Y ₹ 3,600; Z ₹ 3,600. Creditors. P ₹ 3,600; Q ₹ 6,000.

| 2020 | ₹ | |

| Jan.1 | Goods sold to Mr. Red | 1,800 |

| Jan.1 | Goods sold to Mr. White | 1,200 |

| Jan.1 | Goods sold to Mr. Blue | 1,800 |

| Jan.5 | Cash paid for Mr. Q | 1,200 |

| Jan.15 | Cash received from Mr. Y in full settlement | 3,420 |

| Jan.16 | Paid for charity | 300 |

| Jan.16 | Paid for stationery | 420 |

| Jan.16 | Paid to pages | 180 |

| Jan.20 | Cash paid to Mr. P | 16,80 |

| And he allowed us discount | 120 | |

| Jan.21 | Goods sold to Mr. sky | 4,200 |

| Jan.25 | Goods sold to Mr. earth after allowed him trade discount 10% | 270 |

| Jan.27 | Cash received from Mr. sky in full settlement of his account | 4,020 |

| Jan.28 | Allowed interest on capital @ 5% p.a. for one month | |

| Jan.31 | Paid for salaries | 300 |

| Jan.31 | Paid for rent | 600 |

| Jan.31 | Closing stock | 6,000 |

The solution of Question No 2 Chapter No 9 – Unimax Class 11

Journal

| Date | Particulars | L.F. | Debit | Credit | |

| 2020 | |||||

| Jan.1 | Cash A/c | Dr. | 12,000 | ||

| Furniture A/c | Dr. | 2,400 | |||

| W’s A/c | Dr. | 2,400 | |||

| Building A/c | Dr. | 36,000 | |||

| X’s A/c | Dr. | 2,400 | |||

| Y’s A/c | Dr. | 3,600 | |||

| Z’s A/c | Dr. | 3,600 | |||

| To P’s A/c | 3,600 | ||||

| To Q’s A/c | 6,000 | ||||

| To Capital A/c | 52,800 | ||||

| (Being opening entry made) | |||||

| Jan.1 | Mr. Red’s A/c | Dr. | 1,800 | ||

| To Sales A/c | 1,800 | ||||

| (Being goods sold to Mr. Red) | |||||

| Jan.1 | Mr. White’s A/c | Dr. | 1,200 | ||

| To Sales A/c | 1,200 | ||||

| (Being goods sold to Mr. White) | |||||

| Jan.1 | Mr. Blue’s A/c | Dr. | 1,800 | ||

| To Sales A/c | 1,800 | ||||

| (Being goods sold to Mr. Blue) | |||||

| Jan.5 | Mr. Q’s A/c | Dr. | 1,200 | ||

| To Cash A/c | 1,200 | ||||

| (Being cash paid to Mr. Q) | |||||

| Jan.15 | Cash A/c | Dr. | 3,420 | ||

| Discount A/c | Dr. | 180 | |||

| To Mr. T’s A/c | 3,600 | ||||

| (Being cash received from Mr. Y and discount allowed) | |||||

| Jan.16 | Charity A/c | Dr. | 300 | ||

| To Cash A/c | 300 | ||||

| (Being paid for charity) | |||||

| Jan.16 | Stationery A/c | Dr. | 420 | ||

| Postage | Dr. | 180 | |||

| To Cash A/c | 600 | ||||

| (Being paid for stationery postages) | |||||

| Jan.20 | Mr. P’s A/c | Dr. | 1,800 | ||

| To Cash A/c | 1,680 | ||||

| To Discount A/c | 120 | ||||

| (Being cash paid to Mr. P and received) | |||||

| Jan.21 | Mr. sky’ A/c | Dr. | 4,200 | ||

| To Sales A/c | 4,200 | ||||

| (Being goods sold to Mr. sky) | |||||

| Jan.25 | Mr. Earth A/c | Dr. | 243 | ||

| To Sales A/c | 243 | ||||

| (Being goods sold to Mr. Earth) | |||||

| Jan.27 | Cash A/c | Dr. | 4,020 | ||

| Discount A/c | Dr. | 180 | |||

| To Mr. Sky’s A/c | 4,200 | ||||

| (Being cash received from Mr. Sky and discount allowed) | |||||

| Jan.28 | Interest on capital A/c | Dr. | 2,240 | ||

| To Capita A/c | 2,240 | ||||

| (Being allowed interest on capital) | |||||

| Jan.31 | Salaries A/c | Dr. | 300 | ||

| Rent A/c | Dr. | 600 | |||

| To cash A/c | 900 | ||||

| (Being salaries and rent paid) |

| Cash A/c | |||||||

| Date | Particular | J.F. | Amount | Date | Particular | J.F. | Amount |

| Jan.1 | To balance b/d | 12,000 | Jan.5 | By Mr. Q’s A/c | 1,200 | ||

| Jan. 15 | To Mr. Y’s A/c | 3,420 | Jan.16 | By Charity A/c | 300 | ||

| Jan.27 | To Mr. Sky’s A/c | 4,020 | Jan.16 | By Stationery A/c | 420 | ||

| Jan.16 | By Postage A/c | 180 | |||||

| Jan.20 | By Mr. P’s A/c | 1,680 | |||||

| Jan.31 | By salaries A/c | 300 | |||||

| Jan.31 | By Rent A/c | 600 | |||||

| Jan.31 | By Balance c/d | 14,760 | |||||

| 19,440 | 19,440 | ||||||

| Feb.1 | To Balance b/d | 14,760 |

| Dr. | Furniture A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.1 | To Balance b/d | 2,400 | |||||

| 2,400 | |||||||

| Dr. | W’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.1 | To Balance b/d | 2,400 | |||||

| 2,400 | |||||||

| Dr. | Building A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.1 | To Balance b/d | 3,600 | |||||

| 3,600 | |||||||

| Dr. | X’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.1 | To Balance b/d | 2,400 | |||||

| 2,400 | |||||||

| Dr. | Y’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.1 | To Balance b/d | 3,600 | Jan.15 | By Cash A/c | 3,420 | ||

| Jan.15 | By Discount Allowed A/c | 180 | |||||

| 3,600 | 3,600 | ||||||

| Dr. | Z’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.1 | To Balance b/d | 3,600 | |||||

| 3,600 | |||||||

| Dr. | P’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.20 | To Cash A/c | 1,680 | Jan.1 | By Balance b/d | 3,600 | ||

| Jan.20 | To Discount received A/c | 120 | |||||

| Jan.31 | To Balance c/d | 1,800 | |||||

| 3,600 | 3,600 | ||||||

| Feb.1 | By Balance b/d | 3,600 | |||||

| Dr. | Q’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.5 | To Cash A/c | 1,200 | Jan.1 | By Balance b/d | 6,000 | ||

| Jan.31 | To Balance c/d | 4,800 | |||||

| 6,000 | 6,000 | ||||||

| Dr. | Capital A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.31 | To Balance c/d | 55,040 | Jan.1 | By Balance b/d | 52,800 | ||

| Jan.28 | By interest on capital A/c | 2,240 | |||||

| 55,040 | 55,040 | ||||||

| Feb.1 | By Balance b/d | 55,040 | |||||

| Dr. | Mr. Red’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.1 | To Sales A/c | 1,800 | Jan.31 | By Balance c/d | 1,800 | ||

| 1,800 | 1,800 | ||||||

| Feb.1 | To Balance b/d | 1,800 | |||||

| Dr. | Sales A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.31 | To Balance c/d | 9,243 | Jan.1 | By Mr. Red’s A/c | 1,800 | ||

| Jan.1 | By Mr. White’s A/c | 1,200 | |||||

| Jan.1 | By Mr. Blue’s A/c | 1,800 | |||||

| Jan.21 | By Mr. Sky’s A/c | 4,200 | |||||

| Jan.25 | By Mr. earth’s A/c | 243 | |||||

| 9,243 | 9,243 | ||||||

| Feb.1 | By Balance b/d | 9,243 | |||||

| Dr. | Mr. white’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.1 | To Sales A/c | 1,200 | Jan.31 | By Balance c/d | 1,200 | ||

| 1,200 | 1,200 | ||||||

| Feb.1 | To Balance b/d | 1,200 | |||||

| Dr. | Mr. Blue’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.1 | To Sales A/c | 1,800 | Jan.31 | By Balance c/d | 1,800 | ||

| 1,800 | 1,800 | ||||||

| Feb.1 | To Balance b/d | 1,800 | |||||

| Dr. | Discount allowed A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.15 | To Mr. Y’s A/c | 180 | Jan.31 | By Balance c/d | 360 | ||

| Jan.27 | To Mr. Sky’s A/c | 180 | |||||

| 360 | 360 | ||||||

| Feb.1 | To Balance b/d | 360 | |||||

| Dr. | Charity A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.16 | To Cash A/c | 300 | Jan.31 | By Balance c/d | 300 | ||

| 300 | 300 | ||||||

| Feb.1 | To Balance b/d | 300 | |||||

| Dr. | Stationery A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.16 | To Cash A/c | 420 | Jan.31 | By Balance c/d | 420 | ||

| 420 | 420 | ||||||

| Feb.1 | To Balance b/d | 420 | |||||

| Dr. | Postage A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.16 | To Cash A/c | 180 | Jan.31 | By Balance c/d | 180 | ||

| 180 | 180 | ||||||

| Feb.1 | To Balance b/d | 180 | |||||

| Dr. | Discount received A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.31 | To Balance c/d | 120 | Jan.20 | By Mr. P’s A/c | 120 | ||

| 120 | 120 | ||||||

| Feb.1 | By Balance b/d | 120 | |||||

| Dr. | Mr. Sky’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.21 | To Sales A/c | 4,200 | Jan.27 | By Cash A/c | 4,020 | ||

| Jan.27 | By Discount allowed A/c | 180 | |||||

| 4,200 | 4,200 | ||||||

| Dr. | Mr. Earth’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.25 | To Sales A/c | 243 | Jan.31 | By Balance c/d | 243 | ||

| 243 | 243 | ||||||

| Feb.1 | To Balance b/d | 243 | |||||

| Dr. | Interest on capital A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.25 | To Capital A/c | 2,240 | Jan.31 | By Balance c/d | 2,240 | ||

| 2,240 | 2,240 | ||||||

| Feb.1 | To Balance b/d | 2,240 | |||||

| Dr. | Sales A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.31 | To Cash A/c | 300 | Jan.31 | By Balance c/d | 300 | ||

| 300 | 300 | ||||||

| Feb.1 | To Balance b/d | 300 | |||||

| Dr. | Rent A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| Jan.31 | To Cash A/c | 600 | Jan.31 | By Balance c/d | 600 | ||

| 600 | 600 | ||||||

| Feb.1 | To Balance b/d | 600 | |||||

| Trail Balance A/c | ||||

| S. No. | Name of A/c | L.F. | Debit | Credit |

| 1 | Cash A/c | 14,760 | ||

| 2 | Furniture A/c | 2,400 | ||

| 3 | W’s A/c | 2,400 | ||

| 4 | Building A/c | 36,000 | ||

| 5 | X’s A/c | 2,400 | ||

| 6 | Z’s A/c | 3,600 | ||

| 7 | P’s A/c | 1,800 | ||

| 8 | Q’s A/c | 4,800 | ||

| 9 | Capital A/c | 55,040 | ||

| 10 | Mr. Red’s A/c | 1,800 | ||

| 11 | Salaries A/c | 9,243 | ||

| 12 | Mr. White A/c | 1,200 | ||

| 13 | Mr. Blue A/c | 1,800 | ||

| 14 | Discount allowed A/c | 360 | ||

| 15 | Charity A/c | 300 | ||

| 16 | Stationery A/c | 420 | ||

| 17 | Postage A/c | 180 | ||

| 18 | Discount received A/c | 120 | ||

| 19 | Mr. Earth A/c | 243 | ||

| 20 | Interest on capital A/c | 2,240 | ||

| 21 | Salaries A/c | 300 | ||

| 22 | Rent A/c | 600 | ||

| Total | 71,003 | 71,003 |

Read out the full article to know the meaning of Cash Book

Trial Balance | Explanation | Methods | Examples

Also, Check out the same article in Hindi from the following link

Trial Balance | Explanation | Methods | Examples

Also, Check out the solved question of all Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST): An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Computers and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software: Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship