Question No 10 Chapter 3 – UNIMAX Class 12 Part 2 – 2021

Table of Contents

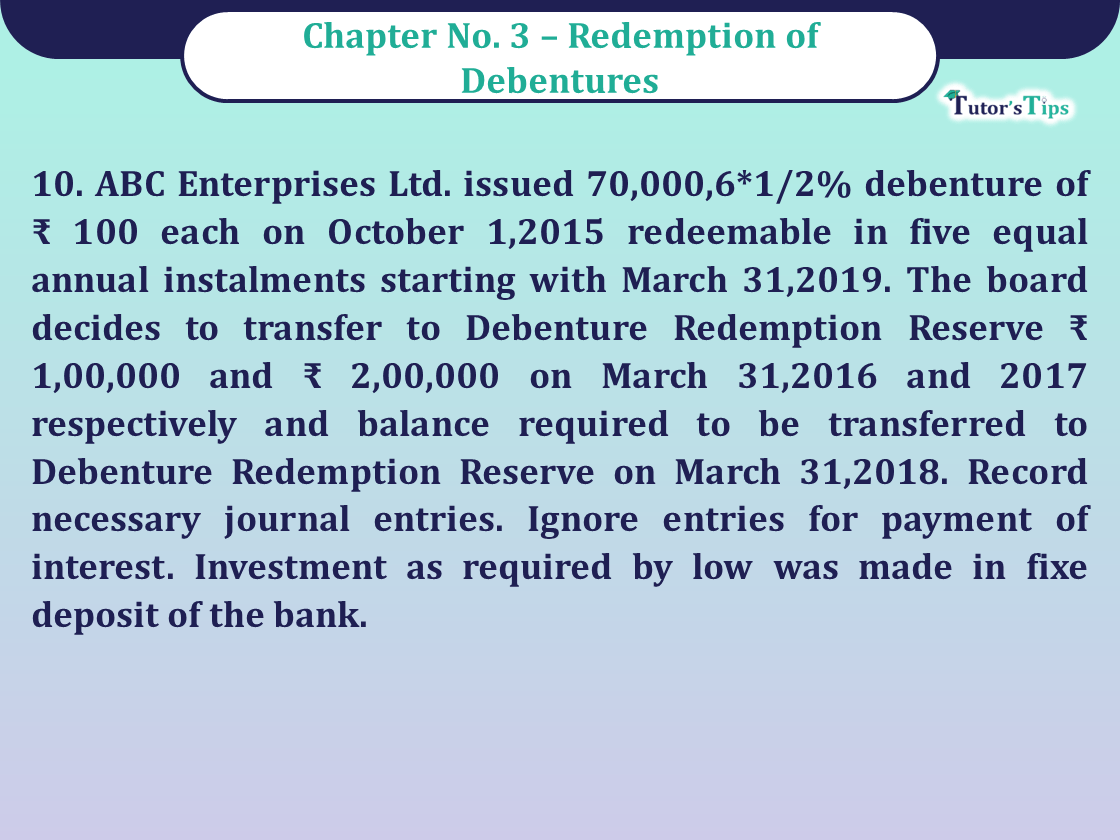

ABC Enterprises Ltd. issued 70,000,6*1/2% debenture of ₹ 100 each on October 1,2015 redeemable in five equal annual instalments starting with March 31,2019. The board decides to transfer to Debenture Redemption Reserve ₹ 1,00,000 and ₹ 2,00,000 on March 31,2016 and 2017 respectively and balance required to be transferred to Debenture Redemption Reserve on March 31,2018. Record necessary journal entries. Ignore entries for payment of interest. Investment as required by low was made in fixe deposit of the bank.

The solution of Question 10 Chapter 3 of +2 Part-2: –

Journal

Books of ABC Enterprises Ltd.

| Date | Particulars |

L.F. | Debit | Credit | |

| 2020 | |||||

| Oct. 1 | Bank A/c | Dr. | 70,00,000 | ||

| To Debenture application & Allotment A/c | 70,00,000 | ||||

| (Being receipt of application money) | |||||

| Oct. 1 | Debenture Application & Allotment A/c | Dr. | 70,00,000 | ||

| To Debenture A/c | 70,00,000 | ||||

| (Being transfer of application money) | |||||

| 2016 March 31 | Surplus is statement in Profit & Loss A/c | Dr. | 1,00,000 | ||

| To Debenture redemption reserve A/c | 1,00,000 | ||||

| (Being transfer of Profit & Loss to DRR) | |||||

| 2017 March 31 | Surplus statement of Profit & Loss A/c | Dr. | 2,00,000 | ||

| To Debenture redemption reserve A/c | 2,00,000 | ||||

| (Being transfer of Profit & Loss DRR) | |||||

| 2018 March 31 | Surplus in statement of Profit & Loss A/c | Dr. | 4,00,000 | ||

| To Debenture redemption investment A/c | 4,00,000 | ||||

| (Being transfer of Profit & Loss to DRR) | |||||

| April 30 | Debenture redemption investment A/c | Dr. | 2,10,000 | ||

| To Bank A/c | 2,10,000 | ||||

| (Being investment made equal to 15% of ₹ 14,00,000) | |||||

| 2019 March 31 | Debenture A/c | Dr. | 14,00,000 | ||

| To Debenture holder A/c | 14,00,000 | ||||

| (Being amount due on redemption) | |||||

| March 31 | Debenture holder A/c | Dr. | 14,00,000 | ||

| To Bank A/c | 14,00,000 | ||||

| (Being payment of amount due to debenture holders) | |||||

| March 31 | Debenture Redemption Reserve A/c | Dr. | 1,40,000 | ||

| To General reserve A/c | 1,40,000 | ||||

| (Being transfer of proportional amount of DRR to GR) | |||||

| 2020 March 31 | Debenture A/c | Dr. | 14,00,000 | ||

| To Debenture holder A/c | 14,00,000 | ||||

| (Being amount due on redemption) | |||||

| March 31 | Debenture holder A/c | Dr. | 14,00,000 | ||

| To Bank A/c | 14,00,000 | ||||

| (Being payment of amount due to debenture holder) | |||||

| March 31 | Debenture Redemption Reserve A/c | Dr. | 1,40,000 | ||

| To General reserve A/c | 1,40,000 | ||||

| (Being transfer of proportional amount of DRR to GR) | |||||

| 2021 March 31 | Debenture A/c | Dr. | 14,00,000 | ||

| To Debenture holder A/c | 14,00,000 | ||||

| (Being amount due on redemption) | |||||

| March 31 | Debenture holder A/c | Dr. | 14,00,000 | ||

| To Bank A/c | 14,00,000 | ||||

| (Being payment of amount due to debenture holder) | |||||

| March 31 | Debenture Redemption Reserve A/c | Dr. | 1,40,000 | ||

| To General reserve A/c | 1,40,000 | ||||

| (Being transfer of proportional amount of DRR to GR) | |||||

| 2022 March 31 | Debenture holder A/c | Dr. | 14,00,000 | ||

| To Bank A/c | 14,00,000 | ||||

| (Being payment of amount due to debenture holder) | |||||

| March 31 | Debenture Redemption Reserve A/c | Dr. | 1,40,000 | ||

| To General reserve A/c | 1,40,000 | ||||

| (Being transfer of proportional amount of DRR to GR) | |||||

| 2023 March 31 | Bank A/c | Dr. | 2,10,000 | ||

| To Debenture Redemption Investment A/c | 2,10,000 | ||||

| (Being investment encashed before redemption of last instalment) | |||||

| March 31 | Debenture A/c | Dr. | 14,00,000 | ||

| To Debenture holder A/c | 14,00,000 | ||||

| (Being amount due on redemption) | |||||

| March 31 | Debenture holder A/c | Dr. | 14,00,000 | ||

| To Bank A/c | 14,00,000 | ||||

| (Being payment of amount due to debenture holder) | |||||

| March 31 | Debenture Redemption Reserve A/c | Dr. | 1,40,000 | ||

| To General reserve A/c | 1,40,000 | ||||

| (Being transfer of proportional amount of DRR to GR) | |||||

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Share Capital: Meaning, Types, and Classes

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication