Question No 07 Chapter 3 – UNIMAX Class 12 Part 2 – 2021

Table of Contents

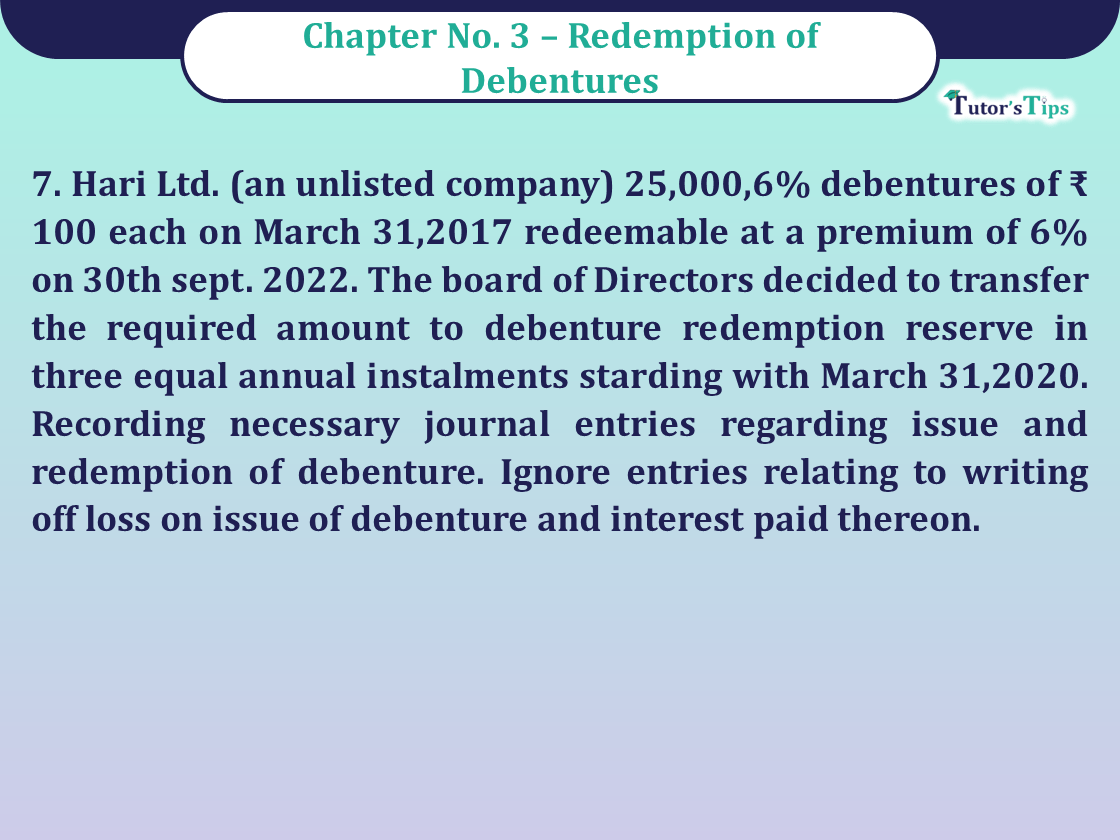

Hari Ltd. (an unlisted company) 25,000,6% debentures of ₹ 100 each on March 31,2017 redeemable at a premium of 6% on 30th sept. 2022. The board of Directors decided to transfer the required amount to debenture redemption reserve in three equal annual instalments starding with March 31,2020. Recording necessary journal entries regarding issue and redemption of debenture. Ignore entries relating to writing off loss on issue of debenture and interest paid thereon.

The solution of Question 07 Chapter 3 of +2 Part-2: –

Journal

Books of Hari Ltd.

| Date | Particulars |

L.F. | Debit | Credit | |

| 2017 | |||||

| March 31 | Bank A/c | Dr. | 25,00,000 | ||

| To Debenture application & allotment A/c | 25,00,000 | ||||

| (Being application money received on issue of debenture) | |||||

| March 31 | Debenture Application & Allotment A/c | Dr. | 25,00,000 | ||

| Loss on issue of debenture A/c | Dr. | 1,50,000 | |||

| To Debenture A/c | 25,00,000 | ||||

| To Premium on redemption of debenture A/c | 1,50,000 | ||||

| (Being transfer of application money) | |||||

| 2019 March 31 | Statement of Profit & Loss A/c | Dr. | 1,50,000 | ||

| To Loss on issue of debenture A/c | 1,50,000 | ||||

| (Being loss on issue of debenture written off) | |||||

| 2020 March 31 | Surplus is statement in Profit & Loss A/c | Dr. | 83,333 | ||

| To Debenture redemption reserve A/c | 83,333 | ||||

| (Being transfer of profit Debenture Redemption Reserve) | |||||

| 2021 March 31 | Surplus is statement in Profit & Loss A/c | Dr. | 83,333 | ||

| To Debenture redemption reserve A/c | 83,333 | ||||

| (Being transfer of profit to Debenture Redemption Reserve) | |||||

| 2022 March 31 | Surplus is statement in Profit & Loss A/c | Dr. | 83,333 | ||

| To Debenture redemption reserve A/c | 83,333 | ||||

| (Being transfer of profit to Debenture Redemption Reserve) | |||||

| April 30 | Debenture redemption investment A/c | Dr. | 3,75,000 | ||

| To Bank A/c | 3,75,000 | ||||

| (Being investment made @ 15% of the face value of debenture to be redeemed) | |||||

| Sept.30 | Bank A/c | Dr. | 3,75,000 | ||

| To Debenture Redemption Investment A/c | 3,75,000 | ||||

| (Being investment encashed) | |||||

| Sept.30 | Debenture A/c | Dr. | 25,00,000 | ||

| Premium on Redemption Reserve A/c | Dr. | 1,50,000 | |||

| To Debenture holder A/c | 26,50,000 | ||||

| (Being amount due to debenture holder on redemption of debenture) | |||||

| Sept. 30 | Debenture holder A/c | Dr. | 26,50,000 | ||

| To Bank A/c | 26,50,000 | ||||

| (Being payment of amount due to debenture holders) | |||||

| Sept. 30 | Debenture redemption reserve A/c | Dr. | 2,50,000 | ||

| To General reserve A/c | 2,50,000 | ||||

| (Being Debenture Redemption Reserve transferred to General Reserve) | |||||

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Share Capital: Meaning, Types, and Classes

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication