Question 73 Chapter 5 of +2-A

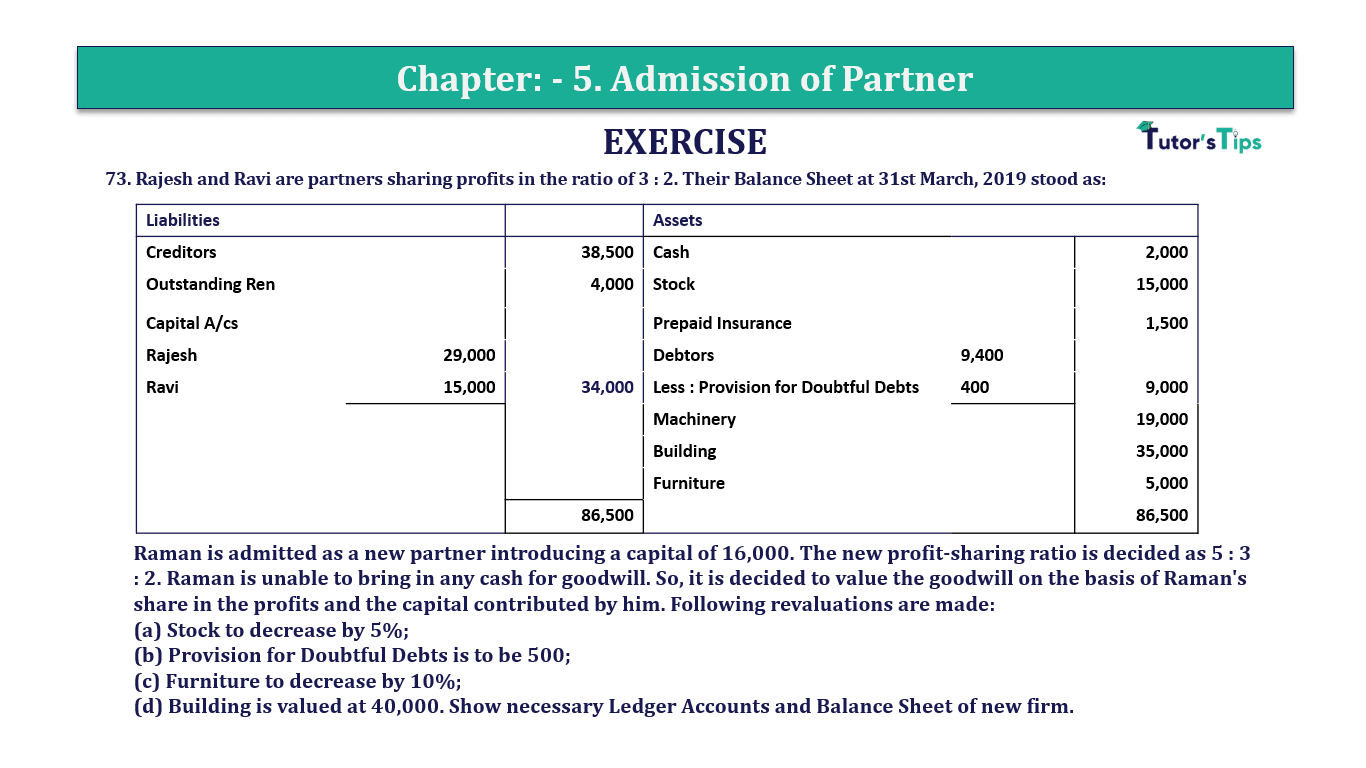

73. Rajesh and Ravi are partners sharing profits in the ratio of 3 : 2. Their Balance Sheet at 31st March, 2019 stood as:

| Liabilities | Assets | ||||

| Creditors | 38,500 | Cash | 2,000 | ||

| Outstanding Ren | 4,000 | Stock | 15,000 | ||

| Capital A/cs | Prepaid Insurance | 1,500 | |||

| Rajesh | 29,000 | Debtors | 9,400 | ||

| Ravi | 15,000 | 34,000 | Less : Provision for Doubtful Debts | 400 | 9,000 |

| Machinery | 19,000 | ||||

| Building | 35,000 | ||||

| Furniture | 5,000 | ||||

| 86,500 | 86,500 |

Raman is admitted as a new partner introducing a capital of 16,000. The new profit-sharing ratio is decided as 5 : 3 : 2. Raman is unable to bring in any cash for goodwill. So, it is decided to value the goodwill on the basis of Raman’s share in the profits and the capital contributed by him. Following revaluations are made:

(a) Stock to decrease by 5%;

(b) Provision for Doubtful Debts is to be 500;

(c) Furniture to decrease by 10%;

(d) Building is valued at 40,000. Show necessary Ledger Accounts and Balance Sheet of new firm.

The solution of Question 73 Chapter 5 of +2-A: –

| Revaluation Account |

|||||

| Liabilities |

Amount | Assets | Amount | ||

| To Stock A/c | 3,000 | By Building A/c | 5,000 | ||

| To Provision for D. Debts A/c | 500 | ||||

| Less: Old Provision | 400 | 100 | |||

| To Furniture A/c | 500 | ||||

| Profit on Revaluation transferred to | 18,400 | ||||

| Rajesh Capital | 2,190 | ||||

| Ravi Capital | 1,460 | 3,650 | |||

| 5,000 | 5,000 | ||||

| Partners’ Capital Account the year ended 31st March, 2019 |

|||||||

| Parti culars |

Rajesh | Ravi | Rama |

Partic |

Rajesh |

Ravi | Rama |

| – | By Balance B/d | 29,000 | 15,000 | – | |||

| By Bank A/c A/c | – | – | 16,000 | ||||

| To Balance c/d | 31,190 | 16,460 | 16,000 | By Reevaluation A/c | 2,190 | 1,460 | – |

| 31,190 | 16,460 | 16,000 | 31,190 | 16,460 | 16,000 | ||

| To Rajesh’s Capital A/c | – | – | 1,635 | By Balance c/d A/c | 31,190 | 16,460 | 16,000 |

| To Raman’s Capital A/c | – | – | 1,635 | By Raman’s Capital A/c | 1,635 | 1,635 | – |

| To Balance c/d | 32,825 |

18,095 | 12,730 | ||||

| 32,825 | 18,095 | 16,000 | 32,825 | 18,095 | 16,000 | ||

| Balance Sheet |

|||||

| Liabilities |

Amount | Assets | Amount | ||

| Creditors | 11,200 | Cash | (2,000 + 16,000) | 18,000 | |

| Outstanding Rent | 3,000 | Stock | (15,000 – 750) | 14,250 | |

| Prepaid Insurance | 1,500 | ||||

| Capital: | Debtors | 9,400 | |||

| Rajesh | 32,825 | Less : Provision for D.D | 500 | 8,900 | |

| Ravi | 18,095 | Building | (35,000 + 5,000) | 40,000 | |

| Raman | 12,730 | 63,730 | Furniture | (5,000 – 500) | 4,500 |

| 1,06,150 | 1,06,150 | ||||

Working Note:-

Calculation of Sacrificing Ratio

Old Ratio of Rajesh and Ravi = 3 : 2

New Ratio of Rajesh, Ravi and Raman = 5 : 3 : 2

Sacrificing Ratio = Old Ratio − New Ratio

| Rajesh’s New Ratio | = | 3 | – | 5 |

| 5 | 10 |

| = | 6 – 5 | |

| 10 |

| = | 1 | |

| 10 |

| Ravi’s New Ratio | = | 2 | – | 3 |

| 5 | 10 |

| = | 4 – 3 | |

| 10 |

| = | 1 | |

| 10 |

Sacrificing Ratio = 1 : 1

Calculation of Goodwill

| Actual Capital of all Partners before adjustment of goodwill | = | Rajesh’s Capital + Ravi’s Capital + Raman’s Capital |

| = | 31,190 + 16,460 + 16,000 | |

| Goodwill | = | Rs 63,650 |

Calculation of Raman’s share of goodwill

| Capitalized value on the basis of Raman’s share | = | 16,000 | X | 10 |

| 2 | ||||

| = | 80,000 |

Calculation of Goodwill

| Goodwill of the Firm | = | Capitalised value of the firm- Actual Capital of the all partner before adjustement of goodwill |

| = | 80,000 – 63,650 | |

| Goodwill | = | 16,350 |

| Raman’s share of Goodwill | = | 16,350 | X | 2 |

| 10 | ||||

| = | 3,270 |

Adjustment of Raman’s share of goodwill

| Rajesh and Ravi each Capital Accounts will be credited by | = | 3,270 | X | 1 |

| 2 | ||||

| = | 1,635 |

| Date | Particulars |

L.F. | Debit | Credit | |

| Raman’s Capital A/c | Dr | 3,270 | |||

| To Rajesh’s Capital A/c | 1,635 | ||||

| To Ravi’s Capital A/c | 1,635 | ||||

| (Raman’s share of goodwill adjusted) cash) |

|||||

Distribution of Profit on Revaluation (in old ratio)

| Rajesh will get | = | 3,650 | X | 3 |

| 5 | ||||

| = | 2,190 |

| Ravi will get | = | 3,650 | X | 2 |

| 5 | ||||

| = | 1,460 |

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication