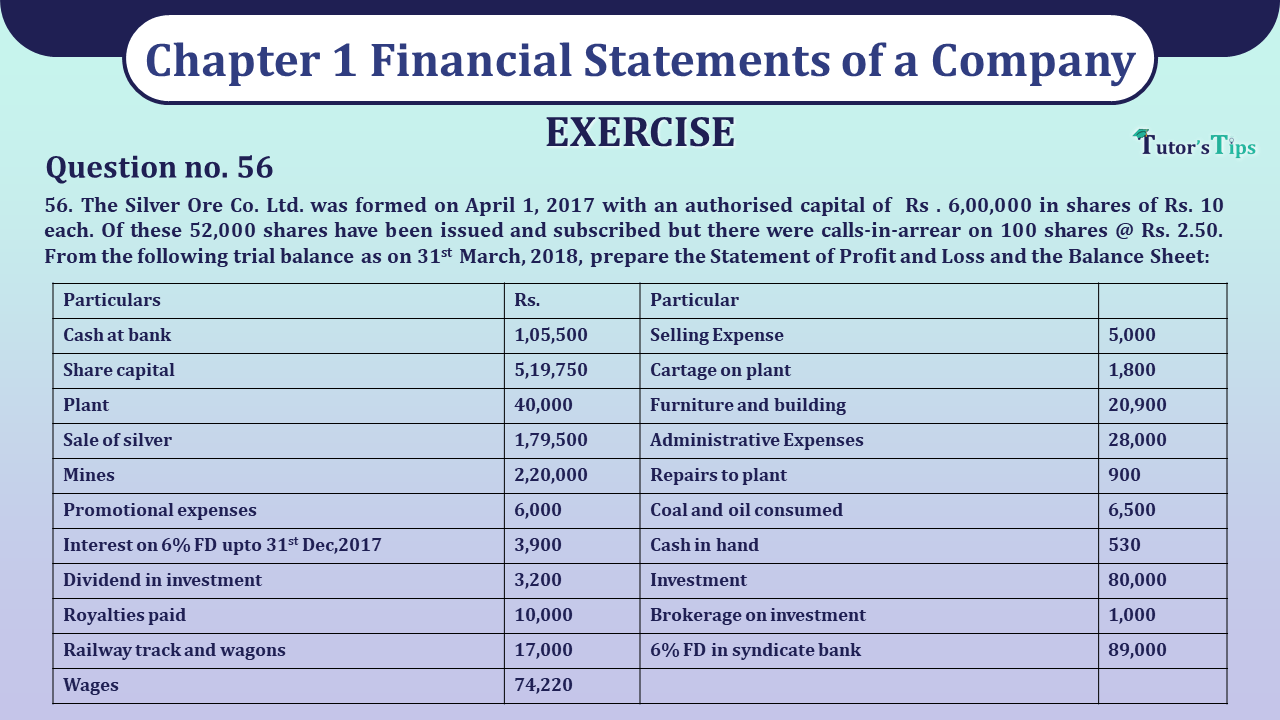

Question 56 Chapter 1 VK Publications Class 12 Part 2 – 2021

56. The Silver Ore Co. Ltd. was formed on April 1, 2017 with an authorised capital of Rs . 6,00,000 in shares of Rs. 10 each. Of these 52,000 shares have been issued and subscribed but there were calls-in-arrear on 100 shares @ Rs. 2.50. From the following trial balance as on 31st March, 2018, prepare the Statement of Profit and Loss and the Balance Sheet:

| Particulars | Rs. | Particulars | Rs. |

| Cash at bank | 1,05,500 | Selling Expense | 5,000 |

| Share capital | 5,19,750 | Cartage on plant | 1,800 |

| Plant | 40,000 | Furniture and building | 20,900 |

| Sale of silver | 1,79,500 | Administrative Expenses | 28,000 |

| Mines | 2,20,000 | Repairs to plant | 900 |

| Promotional expenses | 6,000 | Coal and oil consumed | 6,500 |

| Interest on 6% FD upto 31st Dec,2017 | 3,900 | Cash in hand | 530 |

| Dividend in investment | 3,200 | Investment | 80,000 |

| Royalties paid | 10,000 | Brokerage on investment | 1,000 |

| Railway track and wagons | 17,000 | 6% FD in syndicate bank | 89,000 |

| Wages | 74,220 |

Additional Information:

- Depreciate plant and railway track and wagons by 10%.

- Depreciate Buildings and Furniture by 5%.

- Value of Stock of Silver Ore was Rs. 15,000 on 31st March, 2018.

The solution of Question 56 Chapter 1 VK Publications Class 12 Part 2: –

Statement of Profit and Loss of Silver Ore Co. Ltd. for the year ended 31st March, 2018

| Particulars | Note No. | Current Year Rs. | Previous Year Rs. |

| I. Revenue from Operations (Sales) | 1,79,500 | ||

| II. Other Incomes | 1 | 8,540 | |

| III. Total Revenue ( I+II) | 1,88,040 | ||

| IV. Expenses: | |||

| Cost of Material consumed | 2 | 6,500 | |

| Change in Inventories | 3 | 15,000 | |

| Employee Benefit Expenses | 4 | 74,220 | |

| Depreciation and Amortization Expenses | 5 | 6,745 | |

| Other Expenses | 6 | 52,700 | |

| TOTAL Expenses | 1,25,165 | ||

| V. Profit for the year (III- IV) | 62,875 |

Balance Sheet of Silver Ore Co. Ltd as at 31st March, 2018

| Particulars | Note No. | Current Year Rs. | Previous Year Rs. |

| I. EQUITY AND LIABILITIES | |||

| 1.Shareholders’ Funds | |||

| (a) Share Capitals | 7 | 5,19,750 | |

| (b) Reserves and Surplus | 8 | 62,875 | |

| Total | 5,82,625 | ||

| II. ASSETS | |||

| 1. Non-current Assets | |||

| (a)Fixed Assets | |||

| (i) Tangible Assets | 9 | 2,91,155 | |

| (b) Non-current Investments | 10 | 1,70,440 | |

| 2. Current Assets | |||

| (a) Inventories | 11 | 15,000 | |

| (b) Cash and Cash Equivalents | 12 | 1,06,030 | |

| Total | 5,82,625 |

Notes to Accounts:

| Particulars | Rs. | ||

| 1. Other income | |||

| Interest @6% on F.D. | 3,900 | ||

| Accrued Interest on @6% F.D. (89,000×6/100)- 3900 | 1,440 | ||

| Dividend Received | 3,200 | 8,540 | |

| 2. Cost of Material Consumed: | |||

| Coal and Oil | 6,500 | ||

| 3. Change in Inventories: | |||

| Closing Stock | 15,000 | ||

| 4. Employee Benefit Expenses: | |||

| Wages | 74,220 | ||

| 5. Depreciation and Amortization Expenses: | |||

| Plant | 4,000 | ||

| Railway Track and Wagon | 1,700 | ||

| Building and Furniture | 1,045 | 6,745 | |

| 6. Other Expenses: | |||

| Cartage on Plant | 1,800 | ||

| Repair to Plant | 900 | ||

| Promotional Expenses | 6,000 | ||

| Royalties paid | 10,000 | ||

| Selling Expenses | 5,000 | ||

| Administrative Expenses | 28,000 | ||

| Brokerage on investment | 1,000 | 52,700 | |

| 7. Share Capital | |||

| Authorised Capital: | |||

| 60,000 shares of Rs. 10 each | 6,00,000 | ||

| Issued Capital: | |||

| 52,000 shares of Rs. 10 each | 5,20,000 | ||

| Subscribed Capital: | |||

| Subscribed and fully paid-up (51,900 shares of Rs. 10 each) | 5,19,000 | ||

| Subscribed but not fully paid-up (100 shares of Rs. 10 each) | 1,000 | ||

| Less: Calls-in-Arrear (100x 2.50) | 25 | 750 | 35,200 |

| 8. Reserves and Surplus: | |||

| Surplus, i.e., Balance in Statement of Profit and Loss | 62,875 | ||

| 9. Tangible Assets: | |||

| Mines | 2,20,000 | ||

| Railway Track and Wagon | 17,000 | ||

| Less: Depreciation | 1,700 | 750 | |

| Plant | 40,000 | ||

| Less: Depreciation | 4,000 | 750 | |

| Furniture and Building | 20,900 | ||

| Less: Depreciation | 10,045 | 750 | 2,91,155 |

| 10. Non-current Investments: | |||

| 6% FD in Syndicate Bank | 89,000 | ||

| Accrued Interest on FD | 1,440 | 90,440 | |

| Investments | 80,000 | 91,500 | |

| 11. Inventories: | |||

| Stock | 1,34,700 | ||

| 12. Cash and Cash Equivalents: | |||

| Cash at Bank | 1,05,500 | ||

| Cash in Hand | 530 | 1,06,030 | |

Financial Statements of a Company and Its formats

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication