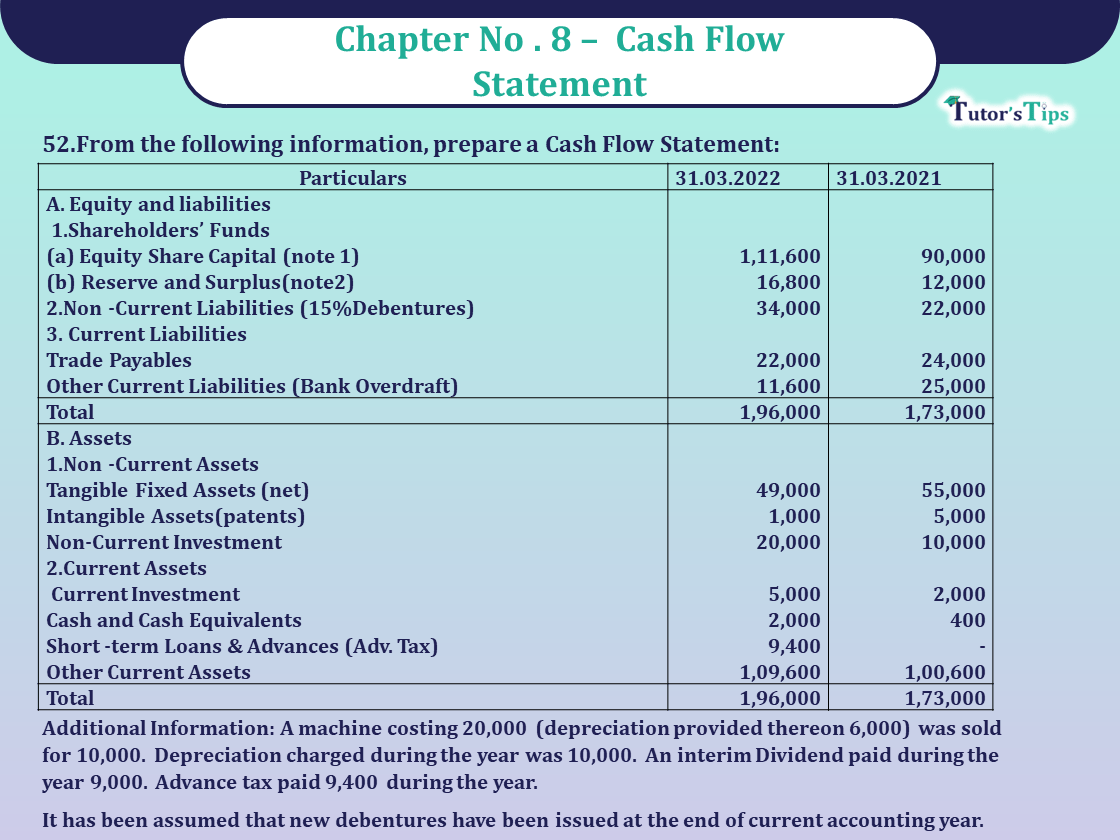

Question 52 Chapter 8 -Unimax Publication Class 12 Part 2 – 2021 52. From the following particular, prepare cash Flow Statement:

| Particulars | 2022 | 2021 |

| Equity & Liabilities | ||

| 2. Non-Current Liabilities (15%Debentures) | ||

| (a) Equity Share Capital (note 1) | 1,11,600 | 90,000 |

| (b) Reserve and Surplus(note2) | 16,800 | 12,000 |

| 1. Non -Current Assets | 34,000 | 22,000 |

| 3. Current Liabilities | ||

| Trade Payables | 22,000 | 24,000 |

| Other Current Liabilities (Bank Overdraft) | 11,600 | 25,000 |

| Total | 1,96,000 | 1,73,000 |

| B. Assets | ||

| 2. Current Assets | ||

| Tangible Fixed Assets (net) | 49,000 | 55,000 |

| Intangible Assets(patents) | 1,000 | 5,000 |

| Non-Current Investment | 20,000 | 10,000 |

| Short-term Loans & Advances (Adv. Tax) | ||

| Current Investment | 5,000 | 2,000 |

| Cash and Cash Equivalents | 2,000 | 400 |

| Short -term Loans & Advances (Adv. Tax) | 9,400 | – |

| Other Current Assets | 1,09,600 | 1,00,600 |

| Total | 1,96,000 | 1,73,000 |

Additional Information: A machine costing 20,000 (depreciation provided thereon 6,000) was sold for 10,000. The depreciation charged during the year was 10,000. An interim Dividend paid during the year 9,000. Advance tax paid 9,400 during the year.

It has been assumed that new debentures have been issued at the end of the current accounting year.

The solution of Question 52 Chapter 8 – Unimax Publication Class 12 Part 2-2021: –

CASH FLOW STATEMENT

FOR THE YEAR ENDED 31st DEC,2022

| Particulars | 2022 | 2021 |

| I. Cash Flow from Operating Activities | 11,800 | |

| A. Net Profit before tax | ||

| B. Adjustments for Non- Cash and Non-Operating items: | ||

| Deprecation on Fixed Assets | 10,000 | |

| Loss on Sale of Machinery | 4,000 | |

| Interest on Debentures | 3,300 | |

| Dividend on Pref. Share | 4,200 | |

| Patents amortized | 4,000 | 25,500 |

| C. Operating Profit before Working Capital Changes | 37,300 | |

| Dividend on pref. Share | ||

| Increase in Other Current Assets | (9000) | |

| Increase in Trade Payables | (2000) | (11,000) |

| E. Net Cash Flow from Operating Activities before tax | 26,000 | |

| F. Less: Tax paid | (9400) | |

| G. Net Cash Inflow from Operating Activities after Tax | 16,900 | |

| II. Cash Flow from investing Activities: | ||

| Sale of Machinery | 10,000 | |

| Purchase of Fixed Assets | (18,000) | |

| Purchase of Non-current Investments | (10,000) | |

| Net Cash used in investing Activities | (18000) | |

| III. Cash Flow from Financing Activities | ||

| Issues of share capital (25,000+2,000) | 27,000 | |

| Issue of debentures | 12,000 | |

| Interest paid on debentures | (3,300) | |

| Interim dividend paid on equity shares | (9000) | |

| Dividend on pref. share | (4200) | |

| Dec. in bank overdraft | (13,400) | |

| Final dividend paid | (10,000) | |

| Redemption of preference shares | (3,400) | |

| Net cash inflow from financing activities | 5700 | |

| iv. net increase in cash and cash equivalents (I + ii + iii) | 4600 | |

| v. opening cash and cash equivalents | 2400 | |

| vi. closing cash and cash equivalents | 7000 |

Working notes:

NOTE 1: SHARE CAPITAL

| Particulars | 31.03.2022 | 31.03.2021 | |

| Equity Share Capital | 80,000 | 55,000 | |

| 12% Preference Share Capital | 31,600 | 35,000 | |

| 1,11,600 | 90,000 | ||

- Advanced tax has not been added back because it has not yet been provided in P& L A/c.

- Fixed Assets Account

| Particulars | ₹ | Particulars | ₹ |

| To balance b/d | 55,000 | By depreciation a/c. | 10,000 |

| To bank a/c (purchase) (b. f) | 18,000 | By bank a/c (sale) | 10,000 |

| By P&L a/c (loss) | 4,000 | ||

| By balance c/d | 49,000 | ||

| 73,000 | 73,000 |

| 1. calculations of net profit before tax | ||

| Closing balance of P & L a/c | 11,800 | |

| Less: opening balance of P& L a/c | (8,000) | |

| Less: Transfer from reserve | (1,000) | |

| Add: interim dividend on equity shares | 9000 | |

| Net profit before tax | 11,800 |