Question 51 Chapter 8 -Unimax Publication Class 12 Part 2 – 2021

Balance Sheets of A as on 1.1.22 and 31.12.22 were as follows:

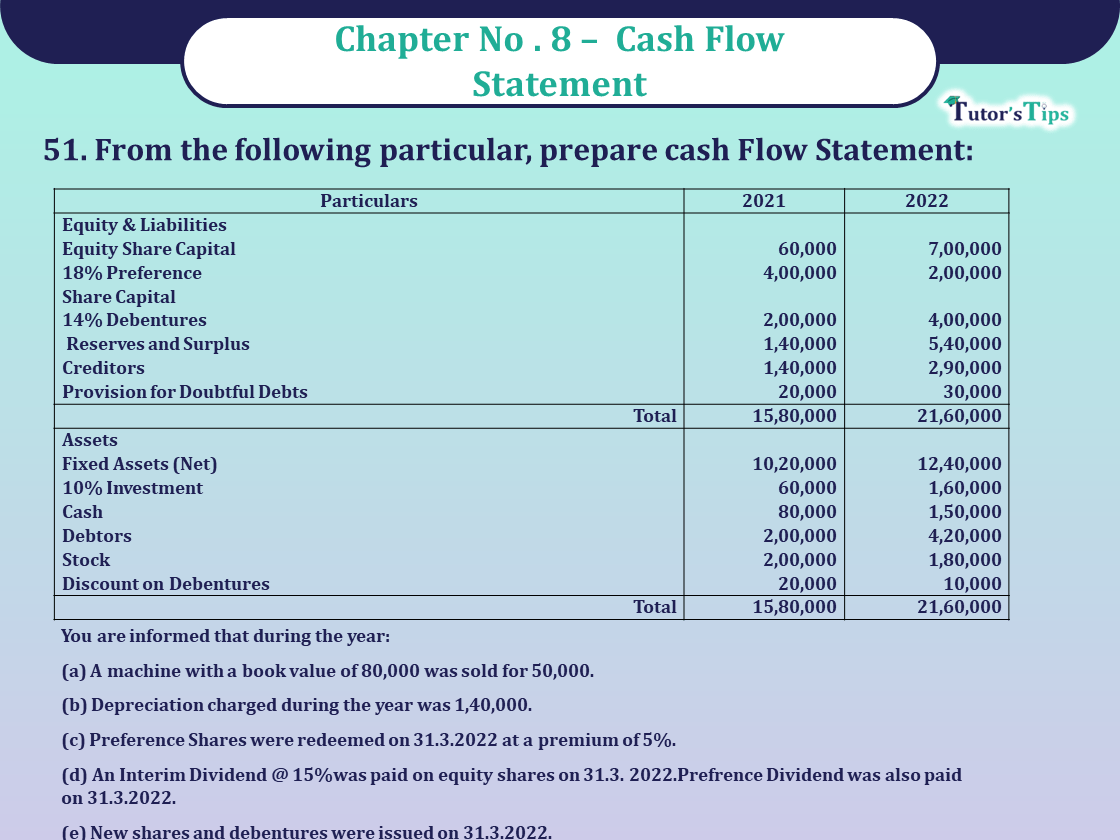

| Particulars | ₹ | ₹ | |

| Equity & Liabilities | |||

| Equity Share Capital | 6,00,000 | 7,00,000 | |

| 18% Preference | 4,00,000 | 2,00,000 | |

| Share Capital | |||

| 14% Debentures | 2,00,000 | 4,00,000 | |

| Reserves and Surplus | 2,20,000 | 5,40,000 | |

| Creditors | 1,40,000 | 2,90,000 | |

| Provision for Doubtful Debts | 20,000 | 30,000 | |

| Total | 15,80,000 | 21,60,000 | |

| Assets | |||

| Fixed Assets (Net) | 10,20,000 | 12,40,000 | |

| 10% Investment | 60,000 | 1,60,000 | |

| Cash | 80,000 | 1,50,000 | |

| Debtors | 2,00,000 | 4,20,000 | |

| Stock | 2,00,000 | 1,80,000 | |

| Discount on Debentures | 20,000 | 10,000 | |

| Total | 15,80,000 | 21,60,000 | |

You are informed that during the year:

(a) A machine with a book value of 80,000 was sold for 50,000.

(b) Depreciation charged during the year was 1,40,000.

(c) Preference Shares were redeemed on 31.3.2022 at a premium of 5%.

(d) An Interim Dividend @ 15%was paid on equity shares on 31.3. 2022.Prefrence Dividend was also paid on 31.3.2022.

(e) New shares and debentures were issued on 31.3.2022

The solution of Question 51 Chapter 8 – Unimax Publication Class 12 Part 2-2021 : –

CASH FLOW STATEMENT

FOR THE YEAR ENDED 31st DEC,2022

| Particulars | ₹ | ₹ | |

| A. Cash Flow from Operating Activities | |||

| Net Profit as per Reserve & surplus | 3,20,000 | ||

| Add: Pref. share Dividend | 72,000 | ||

| Interim Dividend | 90,000 | 1,62,000 | |

| 4,82,000 | |||

| Add: Less on sale of machinery | 30,000 | ||

| Depreciation charged | 1,40,000 | ||

| Premium on redemption of pref. shares | 10,000 | ||

| Interest on debentures | 28,000 | ||

| Discount on issue of debentures written off | 10,000 | 2,18,000 | |

| 7,00,000 | |||

| Less: Interest on Investment | (6000) | (6000) | |

| Operating profit before working Capital charges | 6,94,000 | ||

| Add: Increase in Current Liabilities | |||

| Creditors 1,50,000 | |||

| Provision on for doubtful debts 10,000 | |||

| Decrease in Current Assets | |||

| Stock 20,000 | 1,80,000 | 1,80,000 | |

| 8,74,000 | |||

| Add: Increase in Current liabilities | |||

| Debtors | (200,000) | (200,000) | |

| Cash Flow Operating Activities | 6,54,000 | ||

| B. Cash Flow from investing Activities | |||

| Purchase of fixed assets | (4,40,000) | ||

| Purchase of fixed Investment | (1,00,000) | ||

| Receipt of Interest Investment | 6000 | ||

| Sale of fixed assets | 50,000 | (4,84,000) | |

| Cash used in investing activities | |||

| C. Cash Flow from Financing Activities | |||

| Issue Equity share Capital | 1,00,000 | ||

| Redemption of pref. Shares (2,00,000+10,000) | (2,10,000) | ||

| Issue of Debentures | 200,000 | ||

| Payment of Equity Share dividend | (90,000) | ||

| Payment of preference share dividend | (72,000) | ||

| Payment of Interest on Debentures | (28,000) | ||

| Cash used in Financing Activities | (100,000) | ||

| Net Increase in cash and cash equivalents | 70,000 | ||

| Opening Cash Balance | 80,000 | ||

| Closing Cash Balance | 1,50,000 | ||

Working Notes:

Fixed Assets A/c

| Particulars | ₹ | Particulars | ₹ |

| To balance b/d | 10,20,000 | By Bank A/c (sale) | 50,000 |

| To cash A/c (Purchase) | 4,40,000 | BY P&L A/c (loss on assets sold) | 30,000 |

| BY P&L A/c(Dep) | 1,40,000 | ||

| To balance c/d | 12,40,000 | ||

| 14,60,000 | 14,60,000 |