Question 45 Chapter 6 – Unimax Class 12 Part 1 – 2021

Table of Contents

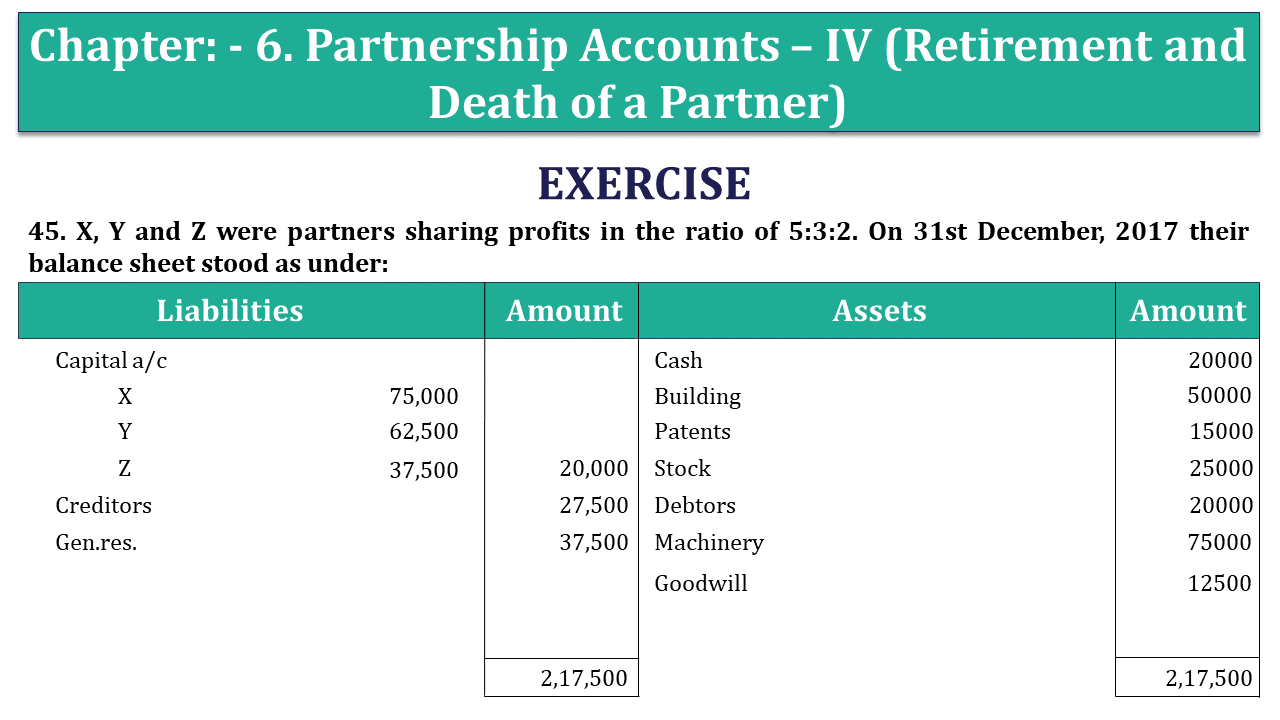

45. X, Y and Z were partners sharing profits in the ratio of 5:3:2. On 31st December, 2017 their balance sheet stood as under:

| Liabilities | Amount | Assets | Amount | |

| Capital a/c | Cash | 20,000 | ||

| X | 75,000 | Building | 50,000 | |

| Y | 62,500 | Patents | 15,000 | |

| Z | 37,500 | 1,75,000 | Stock | 25,000 |

| Creditors | 27,500 | Debtors | 20,000 | |

| Gen.res. | 37,500 | Machinery | 75,000 | |

| Goodwill | 12,500 | |||

| 2,17,500 | 2,17,500 |

Z died on 1st April, 2018. It was agreed that:

- Goodwill was valued 2 ½ years purchase of the average profit of the last four years. Which were 2015 ₹ 2500; 2016 ₹ 30000; 2017₹ 40000 and 2018 ₹ 41500.

- Machinery is valued at ₹ 70000, Patents at ₹ 20000 and building ₹ 62500.

- For the purpose of calculating Z’s share of profit for the year 2019 it was agreed that the same may be calculated based on the average profit of the last 4 years.

- A sum of ₹ 15900 was paid in cash to Z’s executor and the balance in two equal annual installments together with interest @12% p.a.

Give necessary Journal entries to record the above transactions and prepare Z’s executor a/c till it is finally closed.

The solution of Question 45 Chapter 6 – Unimax Class 12 Part 1: –

Y’s capital account

| Particulars | Amount | Assets | Amount |

| Y’s executor‘s loan a/c | 12,800 | By Balance b/d | 20,000 |

| By reserve a/c 3000×2/5 | 6,000 | ||

| By X’s capital a/c | 1,600 | ||

| By P/L susp. a/c 4200×4/12×2/5 (A.P.) | 1500 | ||

| 12,800 | 12,800 |

Journal

| Particulars | L.F. | Debit | Credit | |

| Z’s capital a/c | Dr. | 37,500 | ||

| To Z’s executor a/c | 37,500 | |||

| Gen. Res. a/c | Dr. | 15,000 | ||

| To X’s capital a/c | 7,500 | |||

| To y‘s capital a/c | 4,500 | |||

| To Z’s capital a/c | 3,000 | |||

| X’s capital a/c | Dr. | 8,906 | ||

| Y’s capital a/c | Dr. | 5,344 | ||

| To Z’s executor a/c | 14,250 | |||

| P/L susp. a/c | Dr. | 1,425 | ||

| To Z’s executor a/c | 1,425 | |||

| Revaluation a/c | Dr. | 5,000 | ||

| To Machinery a/c | 5,000 | |||

| Building a/c | Dr. | 12,500 | ||

| To revaluation a/c | 12,500 | |||

| Revaluation a/c | Dr. | 12,500 | ||

| To X’s capital a/c | 6,250 | |||

| To Y’s capital a/c | 3,750 | |||

| To Z’s executors a/c | 2,500 | |||

| X’ capital a/c | Dr. | 6,250 | ||

| Y‘s capital a/c | Dr. | 3,750 | ||

| Z‘s capital a/c | Dr. | 2,500 | ||

| To goodwill a/c | 12,500 | |||

| Z’s executor a/c | Dr. | 15,900 | ||

| To cash a/c | 15,900 | |||

| Z’s executor a/c | Dr. | 40,275 | ||

| To Z’s executor‘s loan a/c | 40,275 | |||

| Interest on loan a/c | Dr. | 4,833 | ||

| To Z’s executor‘s loan a/c | 4,833 | |||

| Z’s executor’s loan a/c | Dr. | 24,971 | ||

| To cash a/c | 24,971 | |||

| Interest on loan a/c | Dr. | 2,416 | ||

| To Z’s executor‘s a/c | 2,416 | |||

| Z’s executor’s loan a/c | Dr. | 22,553 | ||

| To cash a/c | 22,553 |

Z’s Executor‘s a/c

| Particulars | Amount | Particulars | Amount |

| To Goodwill a/c | 2,500 | By Z’s capital a/c | 37,500 |

| To cash a/c | 15,900 | By Gen. Res. a/c 15000×2/10 | 3,000 |

| To Z’s executor’s loan a/c | 40,275 | By X’s capital a/c | 8,906 |

| By Z’s capital a/c | 5,344 | ||

| By profit on rev. | 2,500 | ||

| By S/L susp. a/c 28500×3/12×2/10 | 1,425 | ||

| 58,675 | 58,675 |

Z’s executor’s Loan a/c

| Date | Particulars | Amount | Date | Particulars | Amount |

| 31/3/07 | To cash a/c (20138+4833) | 24,971 | 1/4/06 | By Z’s executor a/c | 40,275 |

| To balance c/d | 20,137 | 31/3/07 | By Int. on loan a/c (12%) | 4,833 | |

| 45,108 | 45,108 | ||||

| 31/3/07 | To cash a/c ((20137+2416) 20137×12/100) | 22,553 | 1/4/07 | By bal. B/d | 20,137 |

| By int. On loan a/c | 2,416 | ||||

| 2416 | 22,555 |

Working note: Z’s share of Goodwill = 2500/4+ 30000/4+ 40000/4 +41500/4 × 2/10× 2.5 =₹ 14250.

Revaluation a/c

| Particulars | Amount | Particulars | Amount | |

| To machinery a/c | 5,000 | By Patents a/c | 5,000 | |

| To profit on revaluation | By building a/c | 12,500 | ||

| X | 6,250 | |||

| Y | 3,750 | |||

| Z | 2,500 | 12,500 | ||

| 17,500 | 17,500 |

Retirement of a Partner – Explained with Illustration

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication