Question 41 Chapter 1 of +2-A

Table of Contents

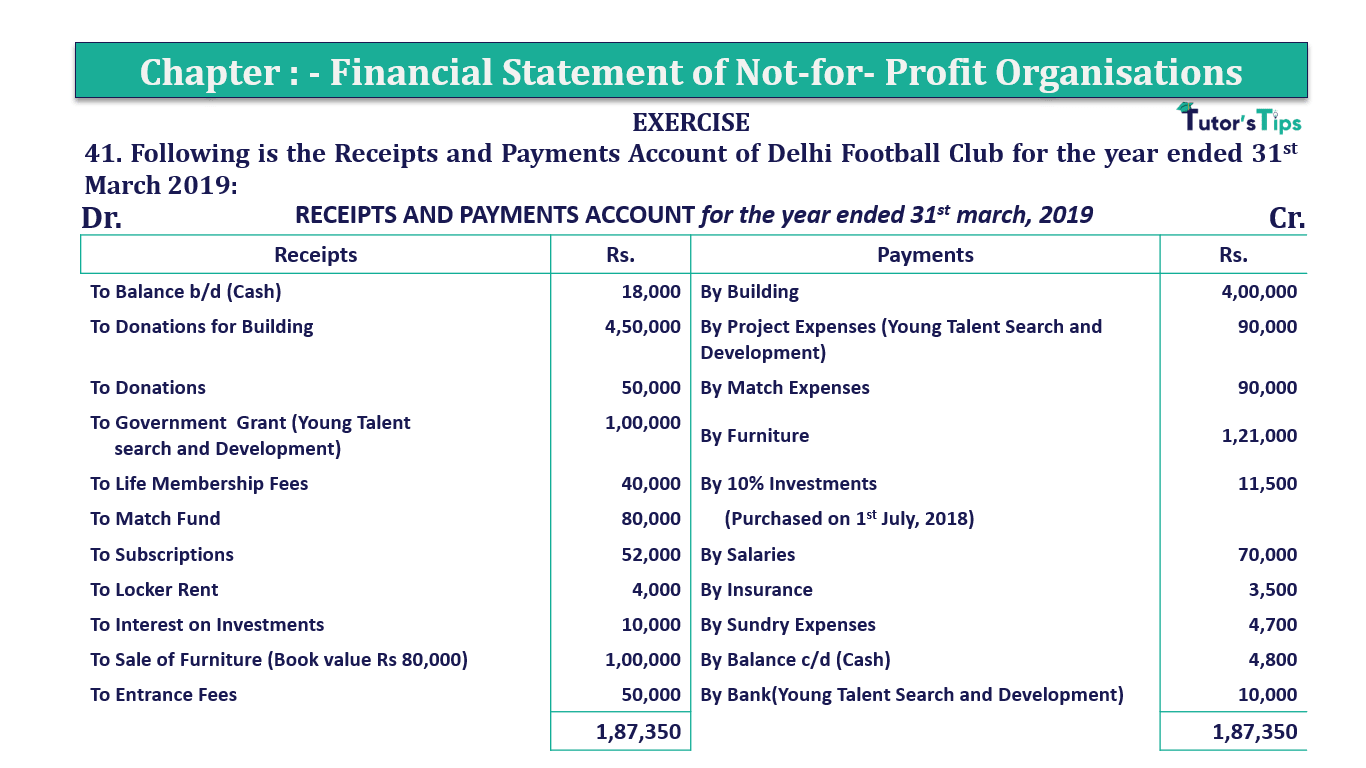

41. Following is the Receipts and Payments Account of Delhi Football Club for the year ended 31st March 2019:

| RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March 2019 | |||

| Receipts | Rs. | Payments | Rs. |

| To Balance b/d (Cash) | 18,000 | By Building | 4,00,000 |

| To Donations for Building | 4,50,000 | By Project Expenses (Young Talent Search and Development) | 90,000 |

| To Donations | 50,000 | By Match Expenses | 90,000 |

| To Government Grant (Young Talent search and Development) | 1,00,000 | By Furniture | 1,21,000 |

| To Life Membership Fees | 40,000 | By 10% of Investments | 11,500 |

| To Match Fund | 80,000 | (Purchased on 1st July 2018) | |

| To Subscriptions | 52,000 | By Salaries | 70,000 |

| To Locker Rent | 4,000 | By Insurance | 3,500 |

| To Interest on Investments | 10,000 | By Sundry Expenses | 4,700 |

| To Sale of Furniture (Book value Rs 80,000) | 1,00,000 | By Balance c/d (Cash) | 4,800 |

| To Entrance Fees | 50,000 | By Bank(Young Talent Search and Development) | 10,000 |

| 1,87,350 | 1,87,350 | ||

Additional Information:

- During the year ended 31st March 2019, the Club had 550 members and each paying an annual subscription of Rs 100.

- Salaries Outstanding as at 1st April 2018 were Rs 10,000 and as at 31st March, 2019 were Rs 5,000.

Prepare Income and Expenditure Account of the Club for the year ended 31st March 2019.

The solution of Question 41 Chapter 1 of +2-A: –

| Income and Expenditure Account (for the year ended 31st March 2018) |

|||||

| Expenditure |

Amount | Income |

Amount | ||

| To Salaries | 70,000 | By Subscription 2018-19 | 52,000 | ||

| Add: – Closing O/s Salary | 5,000 | Add O/s Sub. for 2018 -19* | 3,000 | 55,000 | |

| Less: – Opening O/s Salary | 10,000 | 65,000 | By Donation | 50,000 | |

| To Insurance | 3,500 | By Locker Rent | 4,000 | ||

| To Sundry Expenses | 4,700 | By Interest on Investment * | 10,000 | ||

| To Match Expenses* | 90,000 | Add: Accrued Interest* | 2,000 | 12,000 | |

| Less: – Match Fund | 80,000 | 10,000 | By Entrance Fees | 50,000 | |

| By Profit on Sale of Furniture* | 20,000 | ||||

| To Surplus(Balancing Figure) | 1,07,800 | ||||

| 1,91,000 | 1,91,000 | ||||

Working Note: –

| Calculate Outstanding Subscription for the Year 2017-18 |

|

| Particulars |

Amount |

| Total Subscription due of the year 2018-19 | |

| (Numbers of Member X Amount of Annual Subscription per member) | |

| 550 Members X 100 Per member | 55,000 |

| Less: – Subscription received During the year for the F/y 2018-19 | 52,000 |

| Outstanding Subscription for the year 2018-19 | 3,000 |

Calculation of Interest on Investment

Interest on Investment = Value of Investment X Rate of Interest X Period

Value of Asset = 1,60,000

Rate of Interest = 10%

Period = from 01/07/18 to 31/03/19 i.e. 9 months

(from the date of purchase to the end of the financial year)

= 1,60,000 X 10/100 X 9/12

Interest on Investment = 12,000/-

| Calculation of Accrued amount of Interest on Investment | |

| Total Amount of Interest on Investment For the F/Y 19-20 | 12,000 |

| Less: – Total Amount Interest on Investment received For the F/Y 19-20 | 10,000 |

| Accrued amount of Interest on Investment For the F/Y 19-20 | 2,000 |

| Calculation of the amount of Profit/loss on the sale of Furniture | |

| Sale Value of Furniture | 1,00,000 |

| Less: – Book Value of Furniture | 80,000 |

| Profit on sale of Furniture | 20,000 |

Not-for-Profit Organisations – Meaning and Overview

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: –

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication