Question 40 Chapter 6 of +2-A

Table of Contents

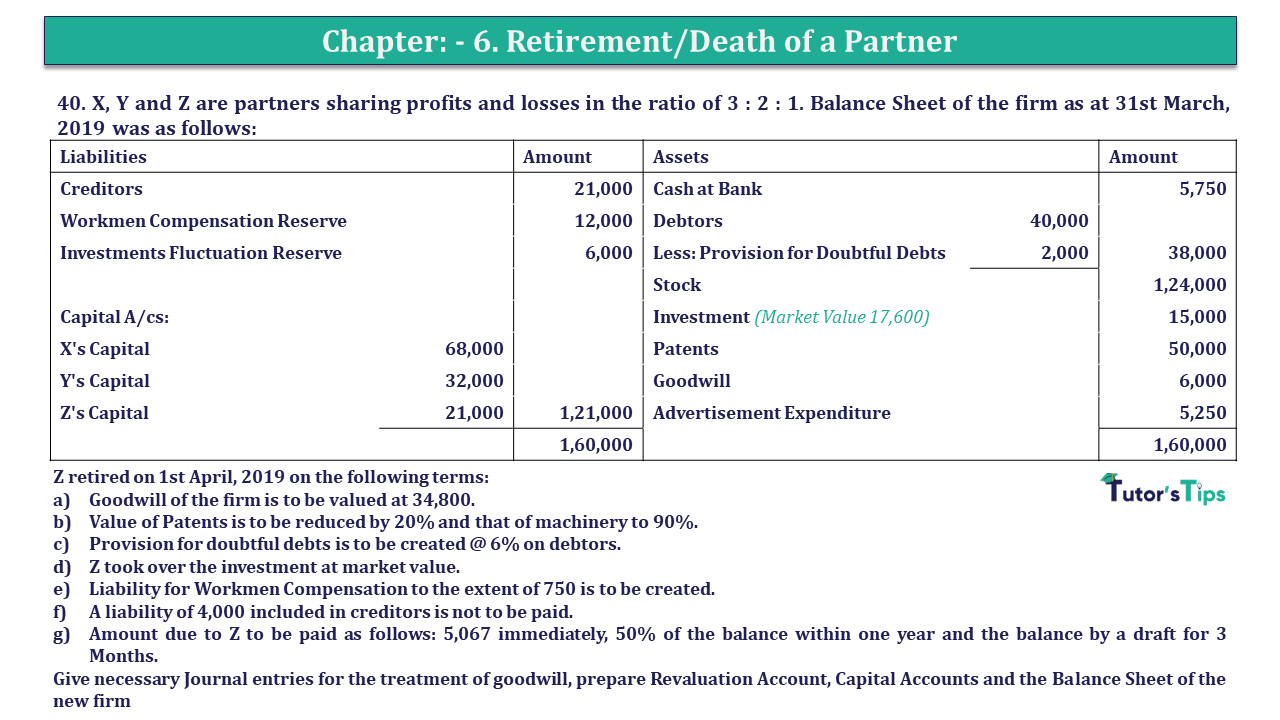

40. X, Y, and Z are partners sharing profits and losses in the ratio of 3: 2: 1. The Balance Sheet of the firm as of 31st March 2019 was as follows:

| Liabilities | Amount | Assets | Amount | ||

| Creditors | 21,000 | Cash at Bank | 5,750 | ||

| Workmen Compensation Reserve | 12,000 | Debtors | 40,000 | ||

| Investments Fluctuation Reserve | 6,000 | Less: Provision for Doubtful Debts | 2,000 | 38,000 | |

| Stock | 1,24,000 | ||||

| Capital A/cs: | Investment (Market Value 17,600) | 15,000 | |||

| X’s Capital | 68,000 | Patents | 50,000 | ||

| Y’s Capital | 32,000 | Goodwill | 6,000 | ||

| Z’s Capital | 21,000 | 1,21,000 | Advertisement Expenditure | 5,250 | |

| 1,60,000 | 1.60.000 | ||||

Z retired on 1st April 2019 on the following terms:

- Goodwill of the firm is to be valued at 34,800.

- The value of Patents is to be reduced by 20% and that of machinery to 90%.

- Provision for doubtful debts is to be created @ 6% on debtors.

- Z took over the investment at market value.

- Liability for Workmen Compensation to the extent of 750 is to be created.

- A liability of 4,000 included in creditors is not to be paid.

- Amount due to Z to be paid as follows: 5,067 immediately, 50% of the balance within one year, and the balance by a draft for 3 Months.

Give necessary Journal entries for the treatment of goodwill, prepare Revaluation Account, Capital Accounts, and the Balance Sheet of the new firm

The solution of Question 40 Chapter 6 of +2-A: –

Journal Entries

| Date | Particulars |

L.F. | Debit | Credit | |

| X’s Capital A/c | Dr. | 3,000 | |||

| Y’s Capital A/c | Dr. | 2,000 | |||

| Z’s Capital A/c | Dr. | 1,000 | |||

| To Goodwill A/c | 6,000 | ||||

| (Being existing goodwill transferred to Partners′ Capital Accounts in their old ratio i.e. 5:3:2) | |||||

| X’s Capital A/c | Dr. | 3,480 | |||

| Y’s Capital A/c | Dr. | 2,320 | |||

| To Z’s Capital A/c | 5,800 | ||||

| (Being share of the goodwill of retiring partner credit to his capital account) | |||||

| Revaluation Account |

|||||

| Particular |

Amount | Particular | Amount | ||

| To Patents A/c | 2,000 | By Investments A/c | 2,600 | ||

| To Machinery | 5,000 | 17,600 – 15,000 | |||

| To Prov. for Doubtful Debts | 400 | By Creditors A/c | 4,000 | ||

| By Loss transferred to | |||||

| A’s Capital A/c | 400 | ||||

| B’s Capital A/c | 267 | ||||

| C’s Capital A/c | 133 | 2,000 | |||

| 7,400 | 7,400 | ||||

| Partners’ Capital Account |

|||||||

| Part. | X | Y | Z |

Part. |

X | Y | Z |

| To Goodwill A/c | 3,000 | 2,000 | 1,000 | By Balance B/d | 1,00,000 | 60,000 | 50,000 |

| To Revaluation A/c | 400 | 267 | 133 | By X’s Capital A/c | – | – | 3,480 |

| To Z’s Capital A/c | 3,480 | 2,320 | – | By Y’s Capital A/c | 2,320 | ||

| To Adv. Exp. A/c | 2,625 | 1,750 | 875 | By WCR A/c | 5,625 | 3,750 | 1,875 |

| To Investments A/c | – | – | 17,600 | By Inv. Flu. Reserve A/c | 3,000 | 2,000 | 1,000 |

| To Bank A/c | – | – | 5,067 | ||||

| To Bills Payable A/c | – | – | 2,500 | ||||

| To Z’s Loan A/c | – | – | 2,500 | ||||

| To Balance c/d | 67,120 | 31,413 | – | ||||

| 76,625 | 37,750 | 29,625 | 76,625 | 37,750 | 29,625 | ||

| Balance Sheet |

|||||

| Liabilities |

Amount | Assets | Amount | ||

| Sundry Creditors | 17,000 | Cash at Bank | 683 | ||

| Workmen Compensation Claim | 750 | 5,750 – 5,067 | |||

| Bills Payable | 2,500 | Stock | 30,000 | ||

| Patents | 8,000 | ||||

| Debtors | 40,000 | ||||

| Z’s Loan | 2,500 | Less: Prov. For D/D | 2,400 | 37,600 | |

| Capital: | Stock | 1,12,000 | |||

| X’s Capital | 67,120 | 1,24,000 – 12,000 | |||

| Y’s Capital | 31,413 | 41,200 | Machinery | 45,000 | |

| 1,21,283 | 1,21,283 | ||||

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication