Question 39 Chapter 1 of Class 12 Part – 1

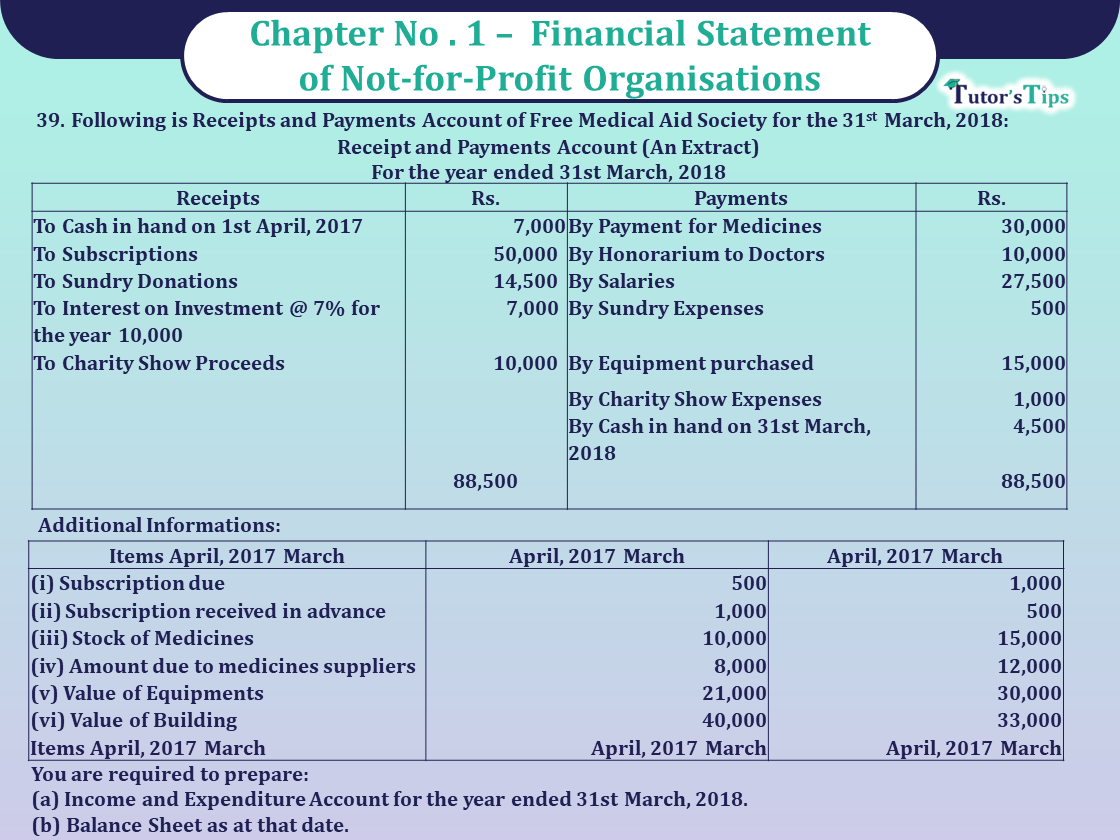

39. Following is Receipts and Payments Account of Free Medical Aid Society for the

31st March, 2018:

Receipt and Payments Account (An Extract)

For the year ended 31st March, 2018

| Receipts | Rs. | Payments | Rs. |

| To Cash in hand on 1st April, 2017 | 7,000 | By Payment for Medicines | 30,000 |

| To Subscriptions | 50,000 | By Honorarium to Doctors | 10,000 |

| To Sundry Donations | 14,500 | By Salaries | 27,500 |

| To Interest on Investment @ 7% for the year 10,000 | 7,000 | By Sundry Expenses | 500 |

| To Charity Show Proceeds | 10,000 | By Equipment purchased | 15,000 |

| By Charity Show Expenses | 1,000 | ||

| By Cash in hand on 31st March, 2018 | 4,500 | ||

| 88,500 | 88,500 |

Additional Informations:

| Items April, 2017 March | April, 2017 March | April, 2017 March |

| (i) Subscription due | 500 | 1,000 |

| (ii) Subscription received in advance | 1,000 | 500 |

| (iii) Stock of Medicines | 10,000 | 15,000 |

| (iv) Amount due to medicines suppliers | 8,000 | 12,000 |

| (v) Value of Equipments | 21,000 | 30,000 |

| (vi) Value of Building | 40,000 | 33,000 |

You are required to prepare:

(a) Income and Expenditure Account for the year ended 31st March, 2018.

(b) Balance Sheet as at that date

The solution of Question 39 Chapter 1 of Class 12 Part – 1: –

Income and Expenditure Account

For the year ended on 31st March, 2018

| Expenditure |

Amount | Income |

Amount | ||

| To Medicines consumed: | |||||

| Payment for Medicines | 30,000 | By Subscriptions | 50,000 | ||

| Add: Opening Stock of Medicines | 10,000 | Add. Outstanding at the end | 1,000 | ||

| Add: Outstanding amount for Medicine Suppliers at the end | 12,000 | Less: Outstanding in the beginning | (500) | ||

| Less: Closing Stock of Medicine | (15,000) | Add: Received in Advance (beginning) 1,000 | 1,000 | ||

| Less: Outstanding amount for Medicine Suppliers in the beginning | (8,000) | 29,000 | Less: Received in Advance (end) | (500) | 51,000 |

| To Honorarium to Doctors | 10,000 | By Sundry Donations | 14,500 | ||

| To Salaries | 27,500 | By Interest on Investments | 7,000 | ||

| To Sundry expenses | 500 | By Charity Show Proceeds | 10,000 | ||

| To Depreciation on Equipments | Less: Charity Show Expenses | 1,000 | 9,000 | ||

| Equipment Purchased | 15,000 | ||||

| Add Opening Stock of Equipment | 21,000 | ||||

| 36,000 | |||||

| Less: Closing stock of Equipment | 30,000 | 6,000 | |||

| To Depreciation on Building (40,000-38,000) 2,000 | 2,000 | ||||

| To Surplus | 6,500 | ||||

| 81,500 | 81,500 | ||||

Opening Balance Sheet (as at 1st April 2017)

| Liabilities |

Amount | Assets |

Amount | |

| Subscriptions Received in Advance | 1,000 | Cash in hand | 7,000 | |

| Amount due to Medicines Suppliers | 8,000 | Investments | 1,00,000 | |

| Capital Fund (Balancing figure) | 1,69,500 | Outstanding Subscriptions | 500 | |

| Stock of medicines | 10,000 | |||

| Equipments | 21,000 | |||

| Building | 40,000 | |||

| 1,78,500 | 1,78,50 | |||

Balance Sheet (as at 1st March 2018)

| Liabilities | Amount | Assets | Amount | |

| Subscriptions Received in Advance | 1,000 | Cash in hand | 4,500 | |

| Amount due to Medicines Suppliers | 8,000 | Investments | 1,00,000 | |

| Capital Fund (Balancing figure) | 1,69,500 | Outstanding Subscriptions | 1,000 | |

| Add. Surplus | 6,500 | Stock of medicines | 15,000 | |

| Equipments | 30,000 | |||

| Building | 38,000 | |||

| 1,88,500 | 1,88,50 | |||

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of all Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

Chapter No. 1 – Accounting Not for Profit Organisations

Chapter No. 2 – Partnership Accounts – I (Introduction)

Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Chapter No. 8 – Company Accounts (Share Capital)

Chapter No. 9 – Company Accounts (Issue of Debentures)

Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

Chapter No. 1 – Financial Statements of a Company

Chapter No. 2 – Financial Statement Analysis

Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

Chapter No. 4 – Ratio Analysis

Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication