Question 37 Chapter 6 – Unimax Class 12 Part 1 – 2021

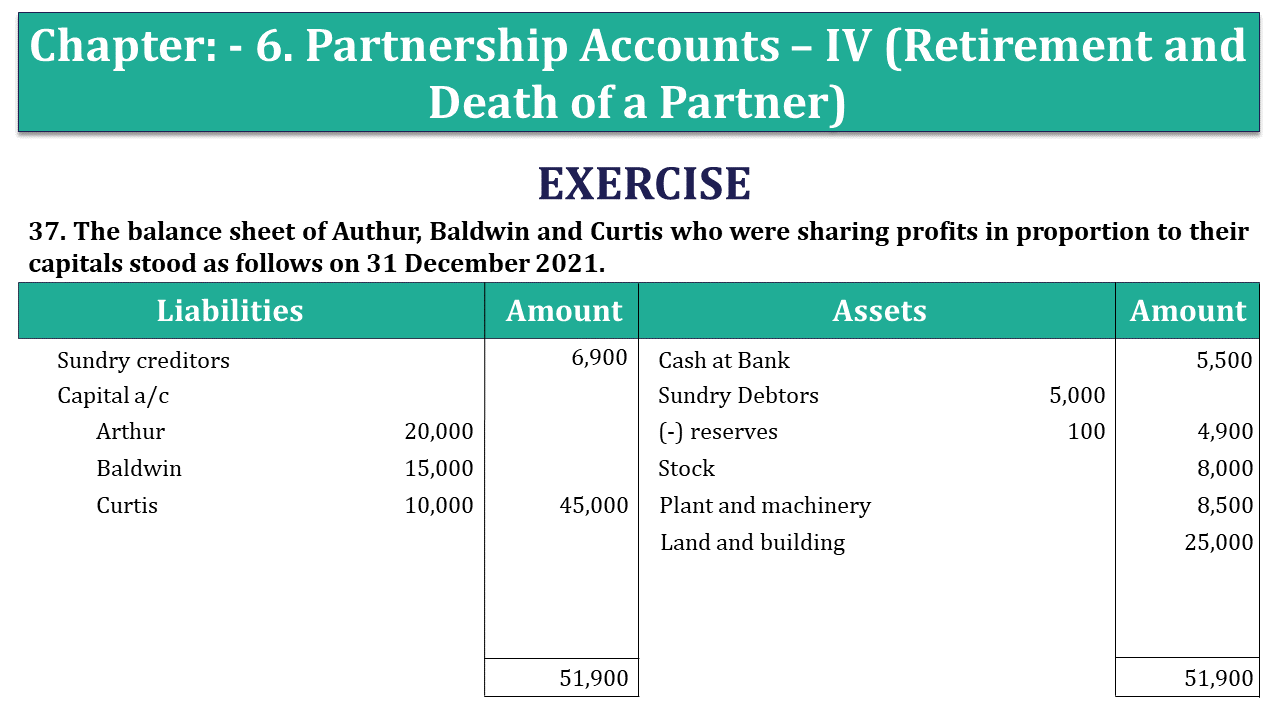

37. The balance sheet of Authur, Baldwin and Curtis who were sharing profits in proportion to their capitals stood as follows on 31 December 2021.

| Liabilities | Amount | Assets |

Amount | ||

| Sundry creditors | 6,900 | Cash at Bank | 5,500 | ||

| Capital a/c | Sundry Debtors | 5,000 | |||

| Arthur | 20,000 | (-)reserves | 100 | 4,900 | |

| Baldwin | 15,000 | Stock | 8,000 | ||

| Curtis | 10,000 | 45,000 | Plant and machinery | 8,500 | |

| land and building | 25,000 | ||||

| 51,900 | 51,900 | ||||

Mr. Baldwin retires and the following readjustments of the assets and liabilities have been agreed upon before the ascertainment of the amount payable by the firm to Mr. Baldwin:

- That the stock be depreciated by 5%

- The reserves for doubtful debts be brought upto 5% on Debtors

- The factory land and building be appreciated by 20%

- A provision of ₹770 be made in respect of outstanding legal charges

- The goodwill for the entire firm as newly constituted be fixed at ₹28000 between Arthur and Curtis in the proportion of five- eight and three-eight after passing entries in their accounts for goodwill (i.e. actual cash to be paid off to or to be brought in by continuing partners as the case may be.)

Pass the journal entries to give effect to the above arrangements and prepare the balance sheet of Arthur and Curtis transferring Baldwin’s share of capital and goodwill to be separate loan account in his name.

The solution of Question 37 Chapter 6 – Unimax Class 12 Part 1: –

Revaluation account

| Particulars | Rs. | Particulars | Rs. | ||

| To stock a/c | 400 | By land and building a/c | 5,000 | ||

| To reserve for d.d. a/c | 150 | ||||

| To provision for legal charges | 770 | ||||

| To profit on revaluation | |||||

| Arthur | 1,635 | ||||

| Baldwin (4:3:2) | 1,227 | ||||

| Curtis | 818 | 3,680 | |||

| 5,000 | 5,000 |

Partners Capital accounts

| Particulars | Arthur | Baldwin | Curtis | Particulars | Arthur | Baldwin | Curtis |

| To Baldwin’s capital a/c | 1,950 | 1,650 | By balance b/d | 20,000 | 15,000 | 10,000 | |

| To Baldwin loan a/c | 19,827 | By profit on revaluation. | 1,635 | 1,227 | 818 | ||

| To cash a/c | 2,185 | By Arthur | 1,950 | ||||

| To balance c/d | 17,500 | 10,500 | By Curtis | 1,650 | |||

| By Cash a/c | 1,332 | ||||||

| 21,635 | 19,827 | 12,150 | 21,635 | 19,827 | 12,150 |

Balance sheet

| Liabilities | Amount | Assets | Amount | ||

| S. Creditors | 6,900 | Cash (5500+1332-2185) | 4,647 | ||

| Capitals | Debtors | 5,000 | |||

| Arthur | 17,500 | (-) reserves | 250 | 4,750 | |

| Curtis | 10,500 | 28,000 | Stock | 7,600 | |

| Baldwin loan a/c | 19,827 | Plant and machinery | 8,500 | ||

| Provision for repairs | 770 | Land and building | 30,000 | ||

| 55,497 | 55,497 |

WORKING NOTE:

Calculation of G.R.:

Arthur =5/8 – 4/9= 45/72-32/72 = 13/72

Curtis = 3/8 – 2/9 = 27/72 – 16/72 = 11/72

G.R. = 13:11.

Retirement of a Partner – Explained with Illustration

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication