Question 36 Chapter 1 – Unimax Class 12 Part 1

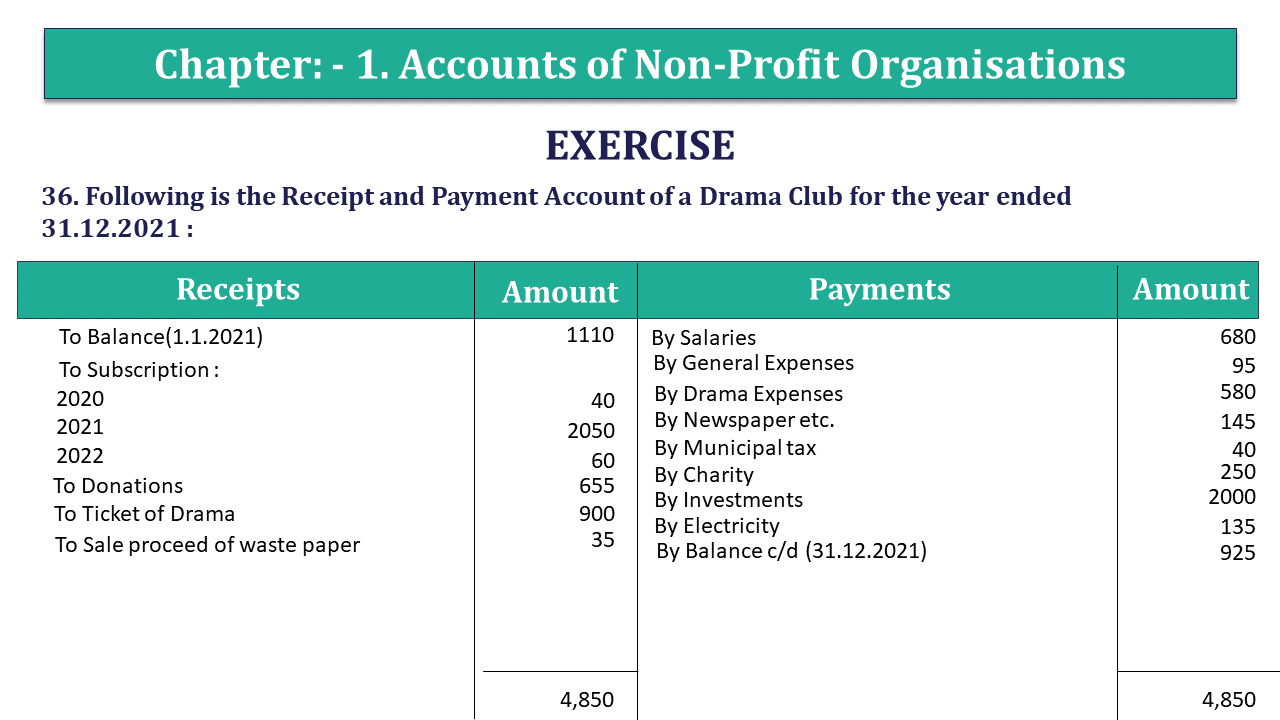

36. Following is the Receipt and Payment Account of a Drama Club for the year ended 31.12.2021 :

| Receipts | Amount | Payments | Amount |

| To Balance(1.1.2021) | 1110 | By Salaries | 680 |

| To Subscription : | By General Expenses | 95 | |

| 2020 | 40 | By Drama Expenses | 580 |

| 2021 | 2050 | By Newspaper etc. | 145 |

| 2022 | 60 | By Municipal tax | 40 |

| To Donations | 655 | By Charity | 250 |

| To Ticket of Drama | 900 | By Investments | 2000 |

| To Sale proceed of waste paper | 35 | By Electricity | 135 |

| By Balance c/d (31.12.2021) | 925 | ||

| 4,850 | 4,850 |

Prepare Income and Expenditure account for the year ended 31.12.2021 and a Balance Sheet on that date keeping in view the following information :

(i) There are 500 members, who pay Rs. 5 pa. Rs. 50 is still in arrears for 2020.

(ii) Municipal tax amounting to Rs. 40 was paid for 1 year upto 31.3.2022, salaries outstanding were Rs. 50.

(iii) A donation of Rs. 50 was promised, but not received during the year.

(iv) 5% depreciation is to be provided on building valued at Rs. 5000.

(v) Interest on investments is due for 3 months, @ 3% p.a.

The solution of Question 36 Chapter 1 – Unimax Class 12 Part 1:

Working Notes : (1) Calculation of expenditure on Salaries for the year 2012.

| Payment made during the year 2012 | 680 |

| Add : Outstanding as on 31-12-12 | 50 |

| 730 |

(2) Calculation of Expenditure on Municipal taxes for the year 2012.

| Payment made during the year 2012 | 40 |

| Less prepaid as on 31/12/12 | 10 |

| 30 |

(3) Calculation of income from subscription for the year 2012 :

| Subscription received during 2012 | 2050 |

| 450 | |

| (2500-2050) | 2500 |

(4) Calculation of income from donation for the year 2012 :

| Donations received during the year 2012 | 655 |

| Add Outstanding as on 31/12/12 | 50 |

| 705 |

(5) Calculation of Capital fund as on 1-1-2012.

Balance Sheet of M/s Drama Club As on 1-1-12.

| Liabilities | Amount | Assets | Amount |

| Capital (B/f) | 6200 | Cash | 1110 |

| Building | 5000 | ||

| Accrued Subscription (50+40) | 90 | ||

| 6200 | 6200 |

Income and Expenditure account of M/s Drama Club

For the year ended on 31st Dec, 2012

| Expenditure | Amount | Income | Amount |

| To salaries | 730 | By subscription | 2500 |

| To general expenses | 95 | By donations | 705 |

| To drama expenses | 580 | By Drama tickets | 900 |

| To Newspaper | 145 | By Sale of old newspaper | 35 |

| To Municipal taxes | 30 | By interest on investment Accrued | 15 |

| To Charity | 250 | ||

| To Electricity | 135 | ||

| To depreciation Building | 250 | ||

| To Excess of Income over Expenditure (Surplus) | 1940 | ||

| 4155 | 4155 |

Balance Sheet of M/s Drama Club As on 31st Dec, 2012

| Liabilities | Amount | Assets | Amount | ||

| Capital Fund | 6200 | Cash | 925 | ||

| Add Surplus | 1940 | 8140 | Subscription Accrued (450+50) | 500 | |

| Subscription prereceived | 60 | Investment | 2000 | ||

| Outstanding Salary | 50 | Accrued Interest | 15 | ||

| Prepaid Municipal Tax | 10 | ||||

| Building | |||||

| Less depreciation @ 5% | 5000 | 4750 | |||

| Outstanding donation | 250 | 4750 | |||

| 8250 | 8250 |

https://tutorstips.com/not-for-profit-organisations/

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication