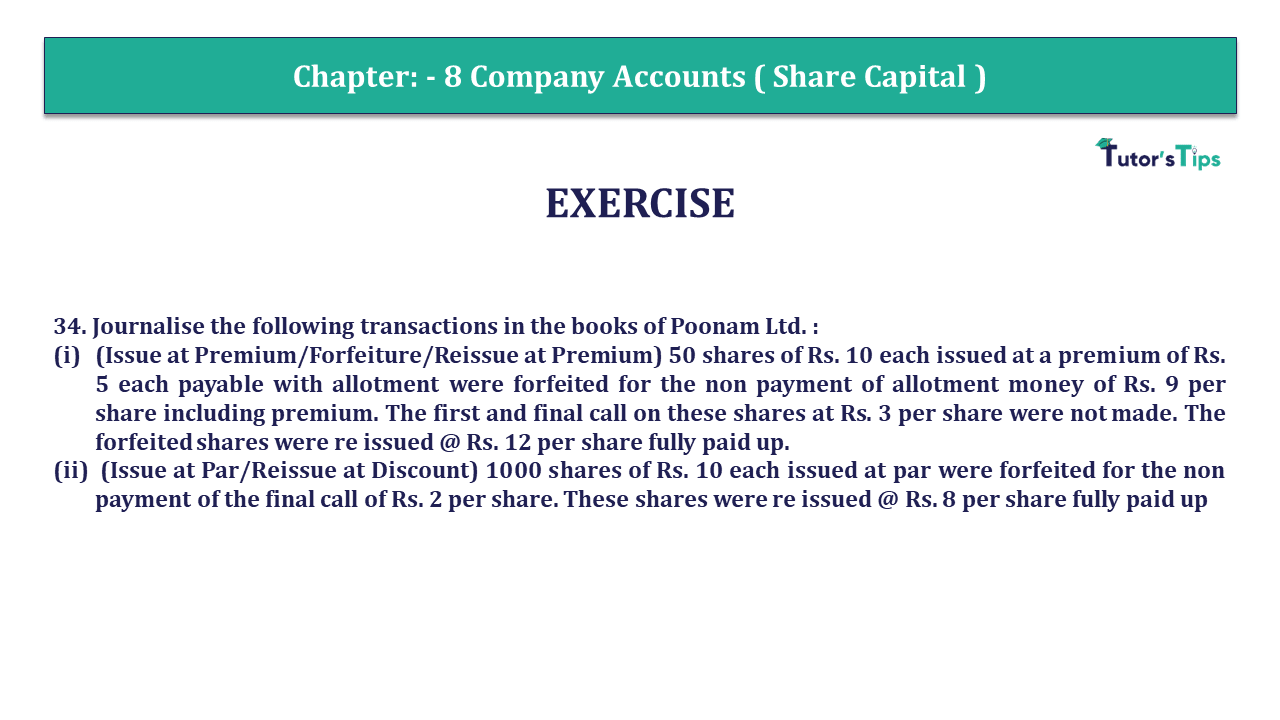

Question 34 Chapter 8 of +2-Part-1

34. Journalise the following transactions in the books of Poonam Ltd. :

(i) (Issue at Premium/Forfeiture/Reissue at Premium) 50 shares of Rs. 10 each issued at a premium of Rs. 5 each payable with allotment were forfeited for the non payment of allotment money of Rs. 9 per share including premium. The first and final call on these shares at Rs. 3 per share were not made. The forfeited shares were re issued @ Rs. 12 per share fully paid up.

(ii) (Issue at Par/Reissue at Discount) 1000 shares of Rs. 10 each issued at par were forfeited for the non payment of the final call of Rs. 2 per share. These shares were re issued @ Rs. 8 per share fully paid up

The solution of Question 34 Chapter 8 of +2 Part-1: –

| Journal |

|||||

| Date | Particulars |

L.F. | Debit | Credit | |

| A) | Share capital A/c (50 X 7) | Dr. | 350 | ||

| Securities Premium Reserve A/c (50X 5) | Dr. | 250 | |||

| To Share Allotment A/c (50X 9) | 450 | ||||

| To Share Forfeited A/c (50X 3) | 150 | ||||

| (Being forfeiture of 50 shares due to non receipt of allotment money @ RS. 9 per share ) | |||||

| Bank A/c (50X 12) | Dr. | 600 | |||

| To Share Capital A/c (50X 10) | 500 | ||||

| To Securities Premium Reserve A/c (50X 2) | 100 | ||||

| (Being reissue of 50 share at premium of Rs. 2 per share ) | |||||

| Share Fortified A/c (150- Nil) | Dr. | 150 | |||

| To Capital Reserve A/c | 150 | ||||

| (Being balance in share fortified transferred to capital reserve) | |||||

| B) | Share capital A/c ( 1000 X 10) | Dr. | 10,000 | ||

| To Share Forfeited A/c ( 1000 X 8) | 8,000 | ||||

| To Share final call A/c ( 1000 X 2) | 2,000 | ||||

| (Being forfeitures of 1000 shares for non receipt of Final call of Rs. 2 per share ) | |||||

| Bank A/c (1000 X 8 ) | Dr. | 8,000 | |||

| Share Fortified A/c (1000X2) | Dr. | 2,000 | |||

| To Share capital A/c (10,000 X 10) | 10,000 | ||||

| (Being fortified shares issued at discount ) | |||||

| Share Fortified A/c (8000-2000) | Dr. | 6,000 | |||

| To Capital Reserve A/c | 6,000 | ||||

| (Being balance in share fortified transferred to capital reserve) | |||||

It all about Question 34 Chapter 8 of +2-Part-1, If you have any problem please comment below.

Forfeiture of shares – Its accounting Entries

End of Solution

Check Out the Solution of all questions of this chapter:

The solution to all questions of Chapter No. 8 – Company Accounts (Share Capital) Class 12 Usha Publication – 2024 is shown as follows, click on the image of the question to get the solution.

Thanks for completing the chapter. If you understand the question or we have helped you with your homework, please share our website on your social media. We are delighted to help you out.

Thanks again.

End of Post

Download a PDF of Chapter No. 8 – Company Accounts (Share Capital):

If you want to download a PDF of this chapter then you can do it. Check out our PDF file on our Store page.

Chapter-Wise Solution of Usha Publication Accountancy – Part 2 Class 12 – Session 2024-25 as per the PSEB curriculum

Check out Solutions to all questions of the every chapter shown as under. The Solution of Accountancy – Part 2 Class 12 – Session 2024-25 is provided as per the new book published by Usha Publication.

Chapter No. 8 – Company Accounts (Share Capital)

Chapter No. 9 – Company Accounts (Issue of Debentures)

Chapter No. 10 – Company Accounts (Redemption of Debentures)

Chapter No. 11 – Financial Statements of a Company

Chapter No. 12 – Financial Statement Analysis

Chapter No. 13 – Tools of Financial Statement Analysis- Comparative and Common Size

Chapter No. 14 – Accounting Ratios

Chapter No. 15 – Cash Flow Statement

Also, Check out our Comprehensive Chapter-wise solution of Advanced Accountancy Part 2 Class 12 by Unimax Publication

- Chapter No. 1 – Company Accounts (Share Capital)

- Chapter No. 2 – Issue of Debentures

- Chapter No. 3 – Redemption of Debentures

- Chapter No. 4 – Financial Statements of a Company (Balance Sheet Only)

- Chapter No. 5 -Financial Statement Analysis

- Chapter No. 6 – Tools/Methods of Financial Analysis

- Chapter No. 7 – Ratio Analysis

- Chapter No. 8 – Cash Flow Statement

Check out Part 1 of both books.

In Class 12th the accountancy has 2 books i.e. Part 1 and Part 2. The Books related to the Part 1 are shown above. but If you want to know more about Part 1, you can check it out from the following links. We have provided the links to both books i.e. Accountancy Part 1 by Usha Publication and Advanced Accountancy Part 2 by Unimax Publication.

1. Accountancy – Part 1 Class 12 – Session 2024-25 By Usha Publication

2. Advanced Accountancy Part 1 Class 12 by Unimax Publication