Question 34 Chapter 6 – Unimax Class 12 Part 1 – 2021

Table of Contents

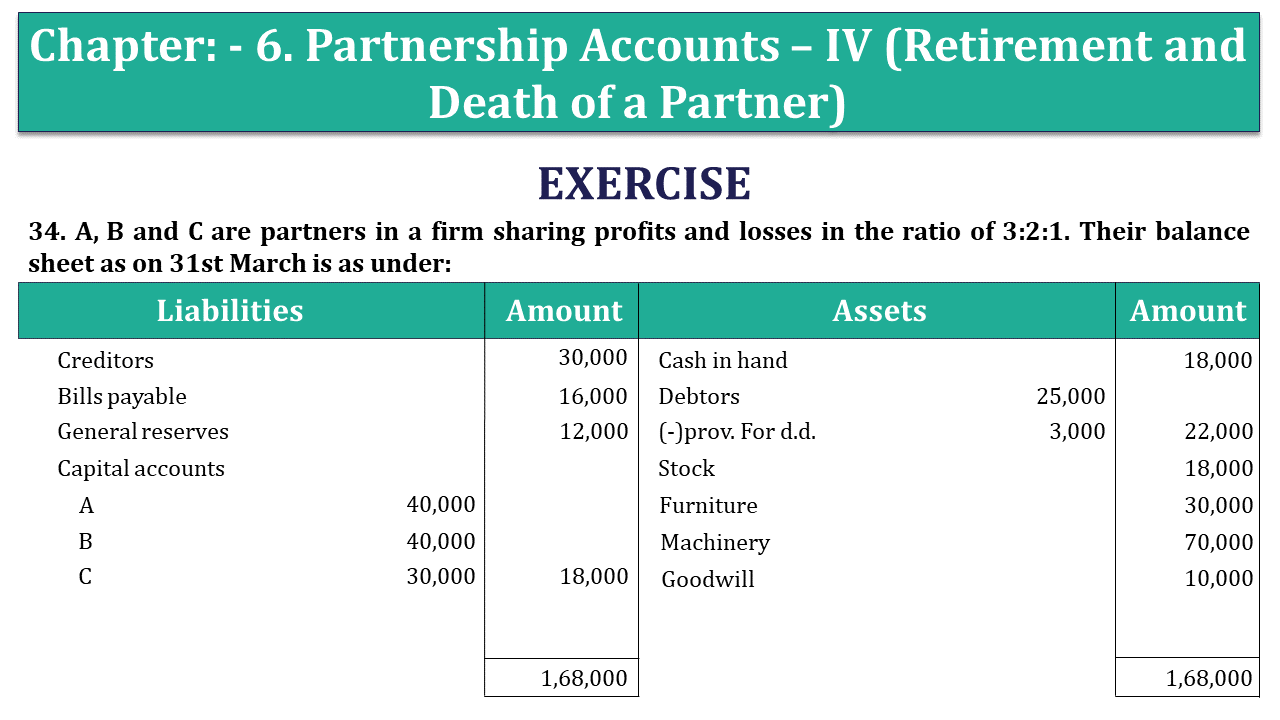

34. A, B and C are partners in a firm sharing profits and losses in the ratio of 3:2:1. Their balance sheet as on 31st March is as under:

| Liabilities | Amount | Assets |

Amount | ||

| Creditors | 30,000 | Cash in hand | 18,000 | ||

| Bills payable | 16,000 | Debtors | 25,000 | ||

| General reserves | 12,000 | (-)prov. For d.d. | 3,000 | 22,000 | |

| Capital accounts | Stock | 18,000 | |||

| A | 40,000 | Furniture | 30,000 | ||

| B | 40,000 | Machinery | 70,000 | ||

| C | 30,000 | 1,10,000 | Goodwill | 10,000 | |

| 1,68,000 | 1,68,000 | ||||

B retires on 1st April 2021 on following terms:

- Provision for doubtful debts be raised by ₹1000.

- Stock to be depreciated by 10% and furniture by 5%.

- There is sn outstanding claim of damage of ₹ 1100 and it is to be provided for.

- Creditors will be written back by ₹6000.

- Goodwill of the firm is values at ₹22000.

- B is paid in full with the cash brought in by A and C in such a manner that their capitals are in proportion to their profit sharing ratio and cash in hand remains at ₹ 10000.

- Prepare revaluation account, partners capital account, balance sheet.

The solution of Question 34 Chapter 6 – Unimax Class 12 Part 1: –

Revaluation account

| Particulars | Rs. | Particulars | Rs. | ||

| To provision for d.d. a/c | 1,000 | By creditors a/c | 6,000 | ||

| To stock a/c | 1,800 | ||||

| To furniture a/c | 1,500 | ||||

| To outstanding claim | 1,100 | ||||

| To profit on revaluation | |||||

| A | 300 | ||||

| B | 200 | ||||

| C | 100 | 600 | |||

| 6,000 | 6,000 |

Partners Capital accounts

| Particulars | A | B | C | Particulars | A | B | C |

| To goodwill a/c | 5,000 | 3333 | 1,667 | By balance c/d | 40,000 | 40,000 | 30,000 |

| To B’s capital a/c | 5,500 | 1,833 | By profit on revaluation | 300 | 200 | 100 | |

| To cash a/c | 48,200 | 2,450 | By A’s capital a/c | 5,500 | |||

| To balance a/c | 78,450 | 26,150 | By C’s capital a/c | 1,833 | |||

| By general reserves a/c | 6,000 | 4,000 | 2,000 | ||||

| By cash a/c | 42,650 | ||||||

| 88,950 | 51,533 | 32,100 | 88,950 | 51,533 | 32,100 |

Balance sheet

| Liabilities | Amount | Assets | Amount | ||

| Creditors (30000-6000) | 24,000 | Cash (18000-42650-48200-2450) | 10,000 | ||

| Bills payable capital a/c | 16,000 | Debtors | 25,000 | ||

| A | 78,450 | (-)prov. | 4,000 | 21,000 | |

| C | 26,150 | 1,04,600 | Stock | 16,200 | |

| Outstanding claim | 1,100 | Furniture | 28,500 | ||

| Machinery | 70,000 | ||||

| 1,45,700 | 1,45,700 |

Retirement of a Partner – Explained with Illustration

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication