Question 32 Chapter 6 – Unimax Class 12 Part 1 – 2021

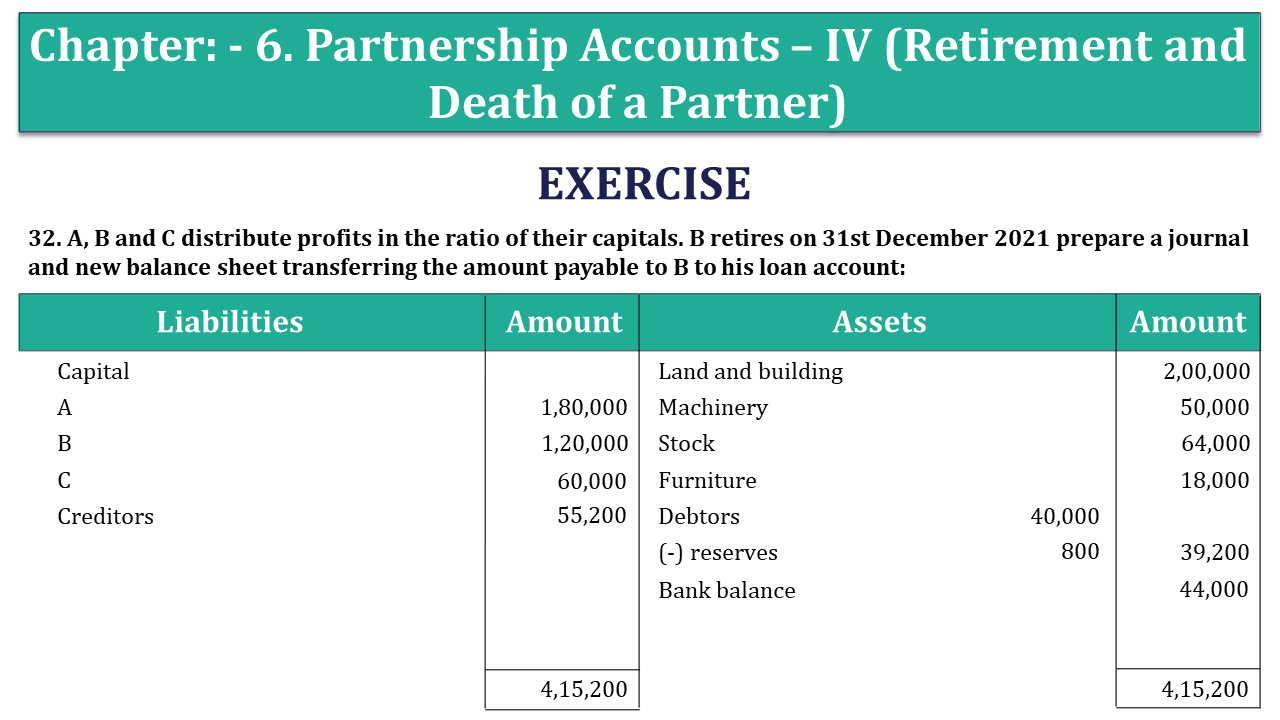

32. A, B and C distribute profits in the ratio of their capitals. B retires on 31st December 2021 prepare a journal and new balance sheet transferring the amount payable to B to his loan account:

| Liabilities | Amount | Assets |

Amount | ||

| Capital | Land and building | 2,00,000 | |||

| A | 1,80,000 | Machinery | 50,000 | ||

| B | 1,20,000 | Stock | 64,000 | ||

| C | 60,000 | Furniture | 18,000 | ||

| Creditors | 55,200 | Debtors | 40,000 | ||

| (-) reserves | 800 | 39,200 | |||

| Bank balance | 44,000 | ||||

| 4,15,200 | 4,15,200 | ||||

Insurance premium (previously debited to profit and loss account ) ₹6000 to be treated as unexpired.

Provision for doubtful debtsto be brouhaha upto 5% on Debtors. Land and building be appreciated by 20%. Provision for repair be maintained at ₹8000. Goodwill of the firm be valued at ₹43200. B’s share shall be adjusted

through capital accounts of A and C whose future profit ratio lies 3:1. • Total capital of the new firm to be ₹224000 in proportion to the sharing ratio (actual cash to be paid off or to be brought in.)

The solution of Question 32 Chapter 6 – Unimax Class 12 Part 1: –

Revaluation account

| Particulars | Rs. | Particulars | Rs. | ||

| To provision for d.d | 1,200 | By prepaid insurance a/c | 6,000 | ||

| To provision for repairs | 8,000 | By building a/c | 40,000 | ||

| To profit on revaluation | |||||

| A | 18,400 | ||||

| B | 12,267 | ||||

| C | 6,133 | 36,800 | |||

| 46,000 | 46,000 |

Partners Capital accounts

| Particulars | A | B | C | Particulars | A | B | C |

| To B’s capital a/c | 10,800 | 3,600 | By balance b/d | 1,80,000 | 1,20,000 | 60,000 | |

| To B’s loan a/c | 14,6667 | By profit on revaluation | 18,400 | 12,267 | 6, 133 | ||

| To bank a/c | 19,600 | 6,533 | By A’s capital a/c | 10,800 | |||

| To balance c/d | 1,68,000 | 56,000 | By C’s capital a/c | 3,600 | |||

| 1,98,400 | 14,6667 | 66,133 | 1,98,400 | 1,46,667 | 66,133 |

Balance sheet

| Liabilities | Amount | Assets | Amount | ||

| Capital a/c | Prepaid insurance | 6000 | |||

| A | 1,68000 | Land and building | 24000 | ||

| B | 56,000 | 2,24,000 | Machinery | 50000 | |

| B’s loan account | 1,46,667 | Stock | 64000 | ||

| Creditors | 55,200 | Furniture | 18000 | ||

| Provision for repairs | 8,000 | Debtors | 40000 | ||

| (-)reserves | 2000 | 38000 | |||

| Bank (44000-19600-6533) | 17867 | ||||

| 4,33,867 | 4,33,867 |

Retirement of a Partner – Explained with Illustration

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication