Question 30 Chapter 6 – Unimax Class 12 Part 1 – 2021

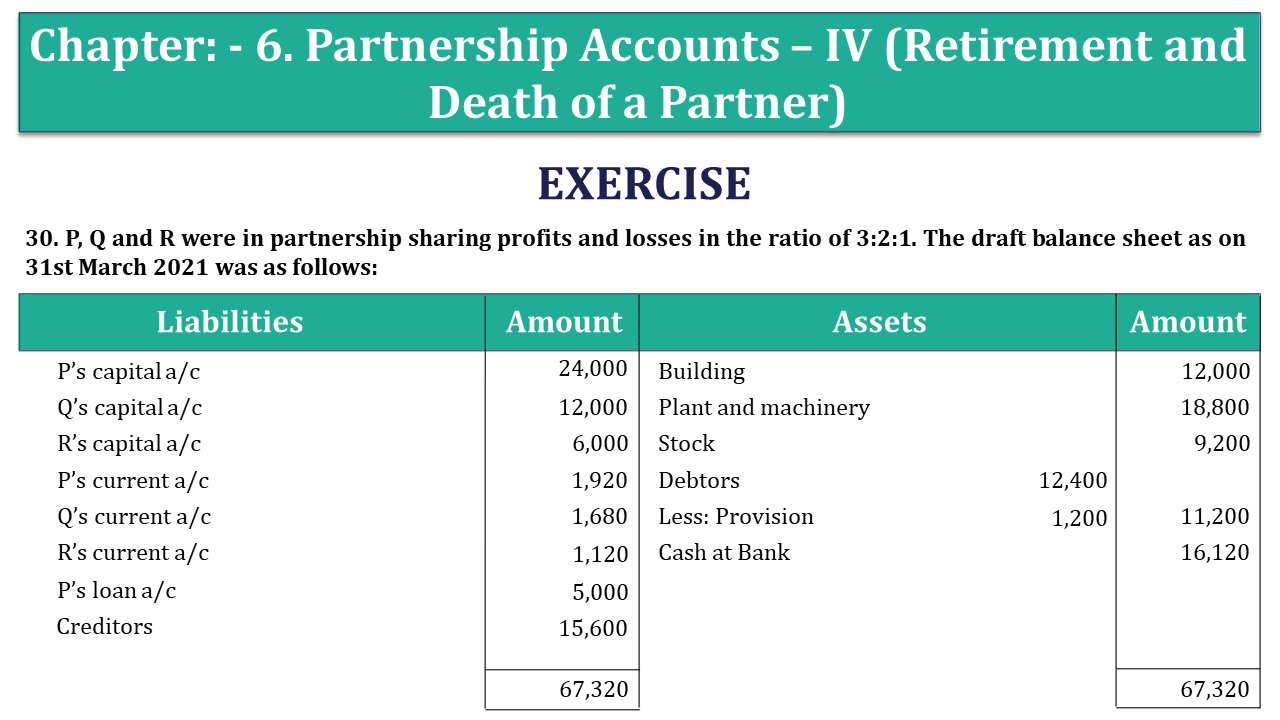

30. P, Q and R were in partnership sharing profits and losses in the ratio of 3:2:1. The draft balance sheet as on 31st March 2021 was as follows:

| Liabilities | Amount | Assets |

Amount | ||

| P’s capital a/c | 24,000 | Building | 12,000 | ||

| Q’s capital a/c | 12,000 | Plant and machinery | 18,800 | ||

| R’s capital a/c | 6,000 | Stock | 9,200 | ||

| P’s current a/c | 1,920 | Debtors | 12,400 | ||

| Q’s current a/c | 1,680 | Less: Provision | 1,200 | 11,200 | |

| R’s current a/c | 1,120 | Cash at Bank | 16,120 | ||

| P’s loan a/c | 5,000 | ||||

| Creditors | 15,600 | ||||

| 67,320 | 67,320 | ||||

P retired on 31st March 2021and Q and R continued in partnership sharing profits and losses in the ratio of 2:1. P’s loan was repaid on 1st April 2021 and it was agreed that the remaining balance due to him, other than that of the current a/c, should remain as loan to the partnership.

For the purpose of P’s retirement, it was agreed that:

- Building be revalued at ₹ 24000 and Plant and Equipment at ₹ 15800.

- The provision for bad debts was to be increased by ₹400.

- A provision of ₹ 500 included in creditors was no longer to be repaid.

- ₹1200 was to be written off from the stock in respect of damaged items

included there in. - A provision of ₹4240 made in respect of outstanding legal charges.

- The goodwill of the firm to be valued at ₹14400.

• You are required to prepare revaluation account, capital a d current accounts of partners, balance sheet of Q, R as on 1st April 2021.

The solution of Question 30 Chapter 6 – Unimax Class 12 Part 1: –

Revaluation A/c

| Particulars | Rs. | Particulars | Rs. | ||

| To plant and machinery | 3,000 | By building | 12,000 | ||

| To provision for bad debts | 400 | By creditors | 500 | ||

| To stock | 1200 | ||||

| To provision for outstanding legal charges | 4,240 | ||||

| To profit on revaluation transferred to current a/c | |||||

| P (3/6) | 1830 | ||||

| Q (2/6) | 1220 | ||||

| R (1/6) | 610 | 3,660 | |||

| 12,500 | 12,500 |

Partners current accounts

| Particulars | P | Q | R | Particulars | P | Q | R |

| To P’s current a/c | 4,800 | 2,400 | By Balance b/d | 1,920 | 1,680 | 1,120 | |

| To cash a/c | 10,950 | By revaluation a/c (profit) | 1,830 | 12,220 | 610 | ||

| By Q’s current a/c | 4,800 | ||||||

| By R’s current a/c | 2,400 | ||||||

| By balance c/d | 1,900 | 670 | |||||

| 10,950 | 4,800 | 2,400 | 10,950 | 4,800 | 2,400 |

Partners capital accounts

| Particulars | P | Q | R | Particulars | P | Q | R |

| To P’s loan a/c | 24,000 | By Balance b/d | 24,000 | 12,000 | 6,000 | ||

| To balance c/d | 12,000 | 6,000 | |||||

| 24,000 | 12,000 | 6,000 | 24,000 | 12,000 | 6,000 |

Balance sheet (After retirement)

| Liabilities | Amount | Assets | Amount | ||

| Creditors | 15,100 | Building | 24,000 | ||

| P’s loan a/c | 24,000 | Plant and machinery | 15,800 | ||

| Q’s capital a/c | 12,000 | Stock | 8,000 | ||

| R’s capital a/c | 6,000 | Debtors | 12,400 | ||

| Outstanding legal charges | 4,240 | (-) prov. | 1,600 | 10,800 | |

| Cash at Bank (16120-5000-10950) | 170 | ||||

| Q’s current a/c | 1,900 | ||||

| R’s current a/c | 670 | ||||

| 61,340 | 61,340 |

Retirement of a Partner – Explained with Illustration

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication