Question 28 Chapter 3 of +2-A

Table of Contents

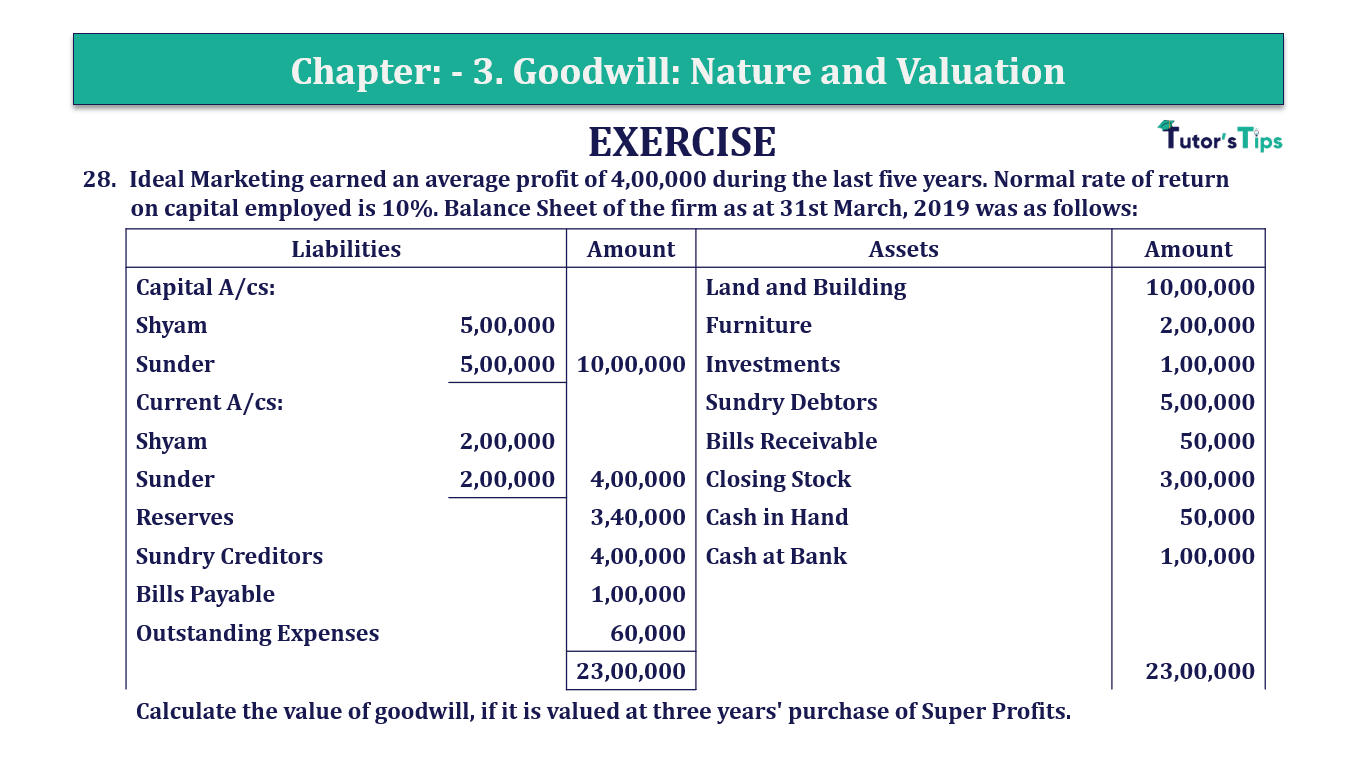

28. Ideal Marketing earned an average profit of 4,00,000 during the last five years. The normal rate of return on capital employed is 10%. Balance Sheet of the firm as at 31st March 2019 was as follows:

| Liabilities | Amount | Assets | Amount | |

| Capital A/cs: | Land and Building | 10,00,000 | ||

| Shyam | 5,00,000 | Furniture | 2,00,000 | |

| Sunder | 5,00,000 | 10,00,000 | Investments | 1,00,000 |

| Current A/cs: | Sundry Debtors | 5,00,000 | ||

| Shyam | 2,00,000 | Bills Receivable | 50,000 | |

| Sunder | 2,00,000 | 4,00,000 | Closing Stock | 3,00,000 |

| Reserves | 3,40,000 | Cash in Hand | 50,000 | |

| Sundry Creditors | 4,00,000 | Cash at Bank | 1,00,000 | |

| Bills Payable | 1,00,000 | |||

| Outstanding Expenses | 60,000 | |||

| 23,00,000 | 23,00,000 |

Calculate the value of goodwill, if it is valued at three years’ purchase of Super Profits.

The solution of Question 28 Chapter 3 of +2-A:

| Super Profit | = | Actual average Profit- Normal Profit |

| Actual average Profit | = | Average Profit + or -Adjustments (if any) |

| = | 4,00,000- 0 (-) | |

| = | 4,00,000 |

| Normal Profit | = | Capital Employed | X | Normal Rate of Return |

| 100 |

| = | 16,40,000 | X | 10 | |

| 100 | ||||

| = | 1,64,000 |

| Capital Employed | = | Total Assets – Non-Trade Investments- Outside Liabilities |

| = | 23,00,000-1,00,000-5,60,000 | |

| = | 16,40,000 | |

| Super Profit | = | 4,00,000-1,64,000 |

| = | 2,36,000 |

Number of years’ purchase = 3

| Goodwill | = | Super Profit X number of years of purchase |

| Goodwill | = | 2,36,000X 3 |

| Goodwill | = | 7,08,000 |

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication