Question 22 Chapter 2 VK Publications Class 12 Part 2 – 2021

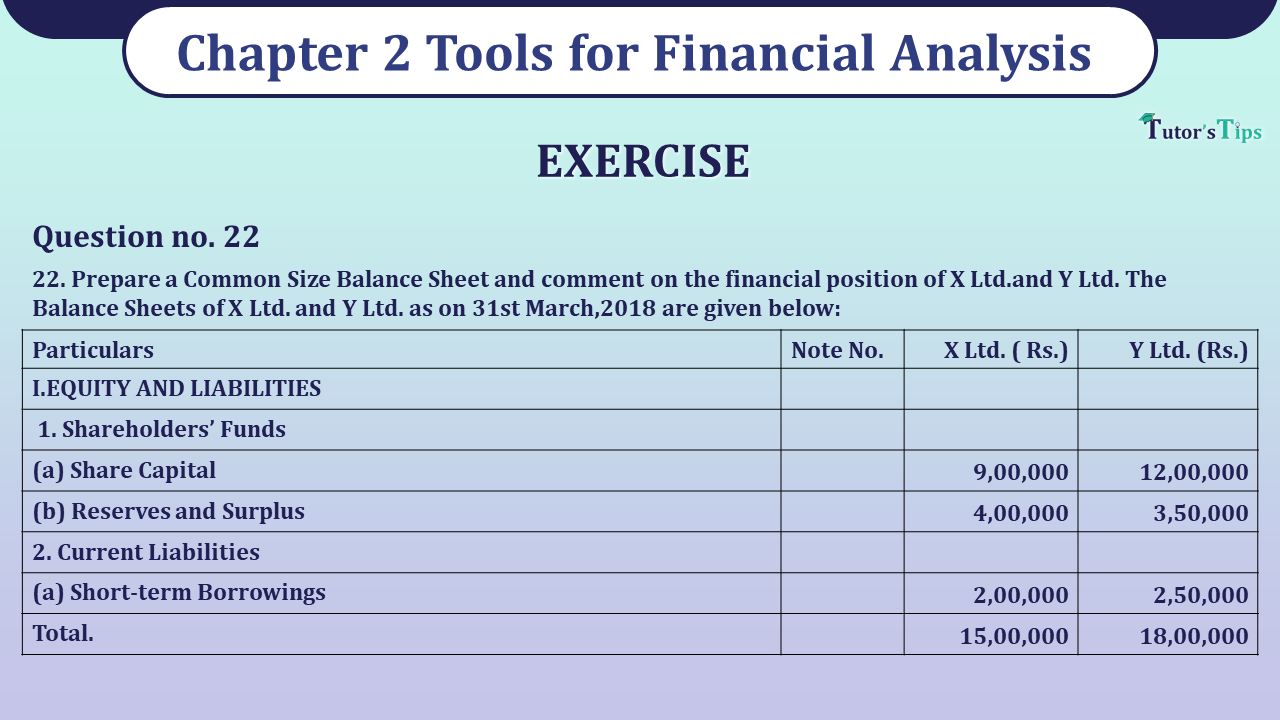

22. Prepare a Common Size Balance Sheet and comment on the financial position of X Ltd.and Y Ltd. The Balance Sheets of X Ltd. and Y Ltd. as on 31st March,2018 are given below:

| Particulars | 2018 (Rs.) | 2017 (Rs.) | |

| I.EQUITY AND LIABILITIES | |||

| 1. Shareholders’ Funds | |||

| (a) Share Capital | 9,00,000 | 12,00,000 | |

| (b) Reserves and Surplus | 4,00,000 | 3,50,000 | |

| 2. Current Liabilities | |||

| (a) Short-term Borrowings | 2,00,000 | 2,50,000 | |

| Total | 15,00,000 | 18,00,000 | |

| II. ASSETS | |||

| 1. Non-Current Asset | |||

| (a) Fixed Assets | 10,00,000 | 16,00,000 | |

| 2. Current Assets | |||

| (a) Cash and Cash Equivalents | 5,00,000 | 2,00,000 | |

| Total | 15,00,000 | 18,00,000 | |

The solution of Question 22 Chapter 2 VK Publications Class 12 Part 2: –

Common Size Balance Sheet Statement For the years ended 31st March, 2017 and 2018

| Particulars | Note | Absolute Amounts | Percentage of the Balance sheet Total | ||

| X Ltd. | Y Ltd. | X Ltd. | Y Ltd. | ||

| Rs. | Rs. | % | % | ||

| I. Equity & Liabilities | |||||

| 1. Shareholder’s Fund | |||||

| a. Share Capital | 9,00,000 | 12,00,000 | 60.00 | 66.67 | |

| b. Reserve & Surplus | 4,00,000 | 3,50,000 | 26.67 | 19.44 | |

| 2. Current Liabilities | |||||

| a. Long term Borrowings | 2,00,000 | 2,50,000 | 13.33 | 13.89 | |

| Total | 15,00,000 | 18,00,000 | 100.00 | 100.00 | |

| II. Assets | |||||

| 1. Non – current Assets | |||||

| a. Fixed Assets | 10,00,000 | 16,00,000 | 66.67 | 88.89 | |

| 2. Current Assets | |||||

| a. Cash & Cash equivalent | 5,00,000 | 2,00,000 | 33.33 | 11.11 | |

| Total | 15,00,000 | 18,00,000 | 100.00 | 100.00 | |

Comment:

(i) The short-term financial position of X Ltd. is better as compared to Y Ltd. as currentliabilities of X Ltd. are 13.33% of total funds invested and current assets are 33.33% ofthese funds. On the other hand, current liabilities of Y Ltd. are 13.89% of total funds and current assets are 11.11% of these funds.

(ii) Y Ltd. has invested more (88.89%) in fixed assets as composed to X Ltd. (66.67%).

(iii) The long-term financial position of both companies is almost equal and sound. Net worth is 86.67% (60 + 26.67) of total funds in case of X Ltd. and 86.11% (66.67 + 19.44) of total : funds in case of Y Ltd.

Financial Statement Analysis and its tools or Techniques

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication