Question 2 Chapter 2 VK Publications Class 12 Part 2 – 2021

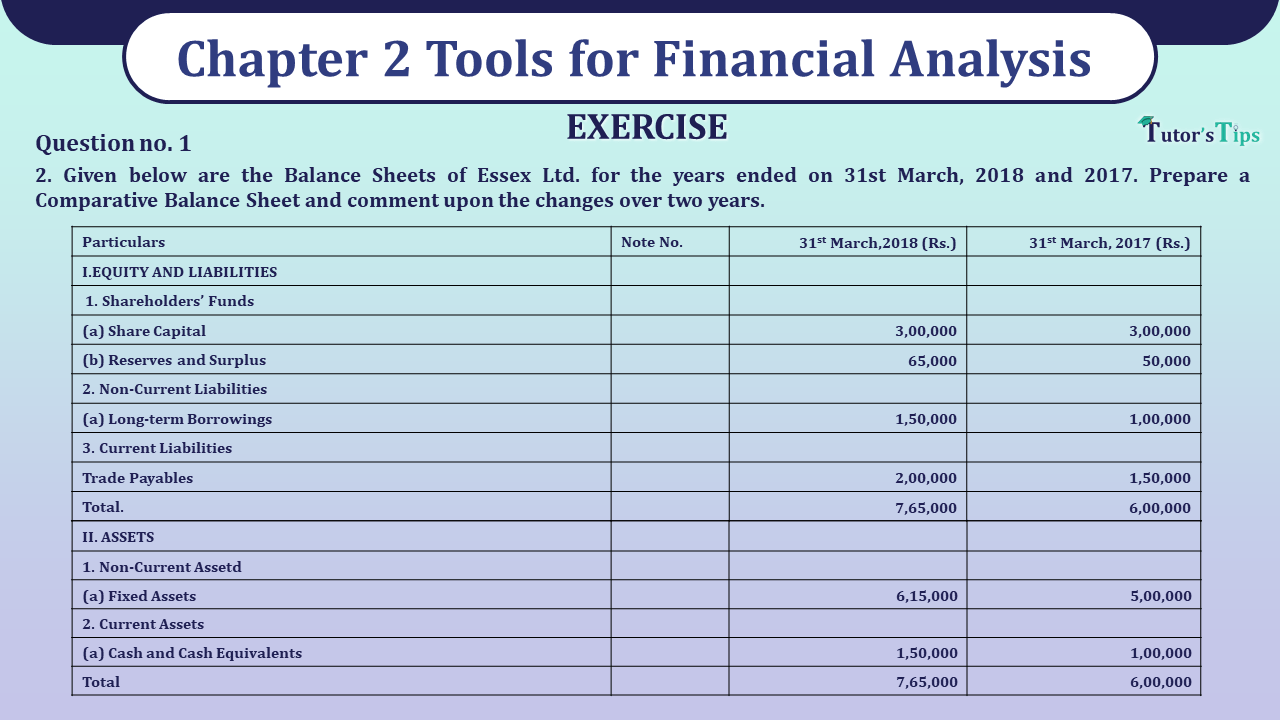

2. Given below are the Balance Sheets of Essex Ltd. for the years ended on 31st March, 2018 and 2017. Prepare a Comparative Balance Sheet and comment upon the changes over two years.

| Particulars | Note No. | 1st March,2018 (Rs.) | 31st March, 2017 (Rs.) |

| I.EQUITY AND LIABILITIES | |||

| 1. Shareholders’ Funds | |||

| (a) Share Capital | 3,00,000 | 3,00,000 | |

| (b) Reserves and Surplus | 65,000 | 50,000 | |

| 2. Non-Current Liabilities | |||

| (a) Long-term Borrowings | 1,50,000 | 1,00,000 | |

| 3. Current Liabilities | |||

| (a) Trade Payables | 2,00,000 | 1,50,000 | |

| Total. | 7,65,000 | 6,00,000 | |

| II. ASSETS | |||

| 1. Non-Current Assetd | |||

| (a) Fixed Assets | 6,15,000 | 5,00,000 | |

| 2. Current Assets | |||

| (a) Cash and Cash Equivalents | 1,50,000 | 1,00,000 | |

| Total | 7,65,000 | 6,00,000 |

The solution of Question 2 Chapter 2 VK Publications Class 12 Part 2: –

Comparitive Balance Sheets of Essex Ltd. As at 31st March, 2017 & 2018

| Particulars | Note | 2016-2017 Rs. | 2017-2018 Rs. | Absolute Change Rs. | Percentage Change % |

| 1 | 2 | 3 | 4 | 5 | |

| A | B | B – A = C | C/A X 100 = D | ||

| I. Equity & Liabilities | |||||

| 1. Shareholder’s Fund | |||||

| a. Share Capital | 3,00,000 | 3,50,000 | 50,000 | 16.67 | |

| b. Reserve & Surplus | 50,000 | 65,000 | 15,000 | 30.00 | |

| 2. Non – current Liabilities | |||||

| a. Long term Borrowings | 1,00,000 | 1,50,000 | 50,000 | 50.00 | |

| 3. Current Liabilities | |||||

| a. Trade payable | 1,50,000 | 2,00,000 | 50,000 | 33.33 | |

| Total | 6,00,000 | 7,65,000 | 1,65,000 | 27.50 | |

| II. Assets | |||||

| 1. Non – current Assets | |||||

| a. Fixed Assets | 5,00,000 | 6,15,000 | 1,15,000 | 23.00 | |

| 2. Current Assets | |||||

| a. Cash & Cash equivalents | 1,00,000 | 1,50,000 | 50,000 | 50.00 | |

| Total | 6,00,000 | 7,65,000 | 1,65,000 | 27.50 |

Comment: The analysis of the above Comparative Balance Sheet gives the following conclusions:

(i) Share Capitäl has increased by Rs. 50,000, i.e .,16.67% increase.

(ii) Reserves and Surplus have increased by Rs. 15,000, i.e., 30% which reflects the increase in profits.

(iii) Long-term Borrowings has increased by 50% which shows the increased participation of debt capital in business.

(iv) Increase of fixed assets means purchase of fixed Assets partly by issue of share capital and partly by debt capital.

(v) Current Liabilities have increased by 33.33% whereas Current assets have increased by 50%. It has resulted in the imcrease in working capital of the firm.

Financial Statement Analysis and its tools or Techniques

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication