Question 17 Chapter 8 – Unimax Publication Class 12 Part 2 – 2021

Table of Contents

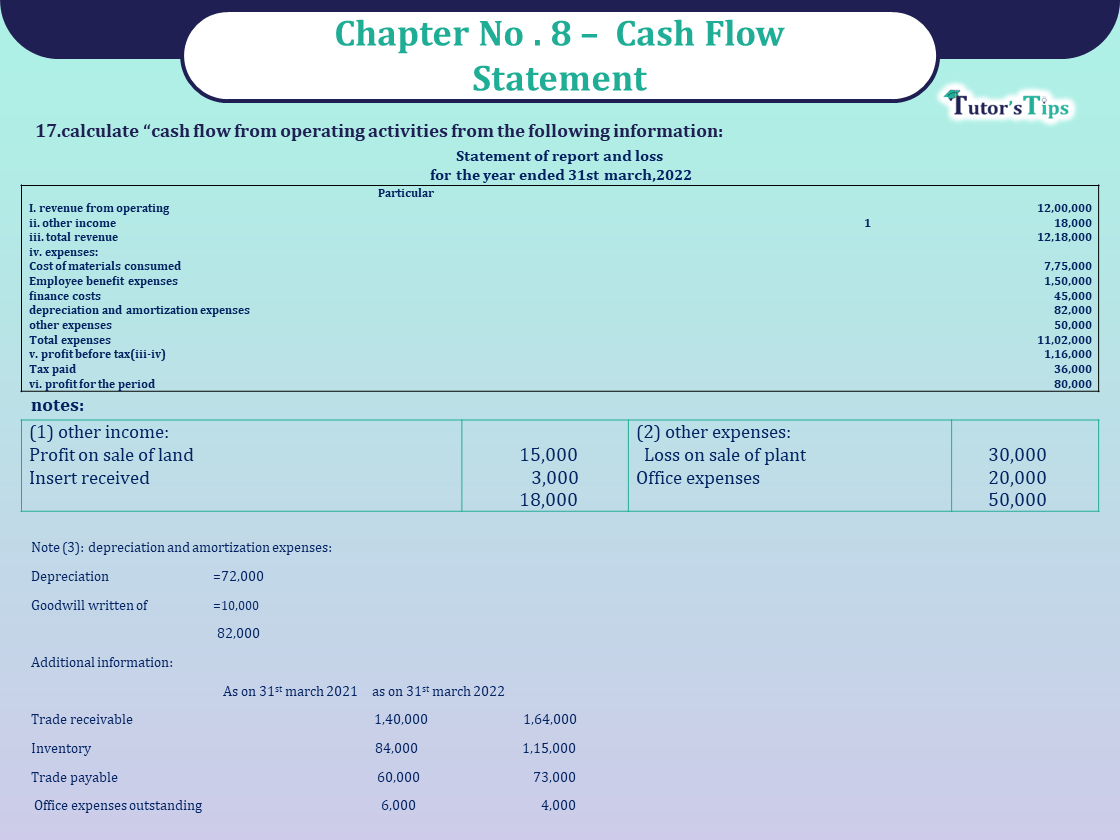

17.calculate “cash flow from operating activities from the following information:

Statement of report and loss

for the year ended 31st march,2022

| Particulars | Note no. | Amount ₹ |

| I. revenue from operating | 12,00,000 | |

| ii. other income | 1 | 18,000 |

| iii. total revenue | 12,18,000 | |

| iv. expenses: | ||

| Cost of materials consumed | 7,75,000 | |

| Employee benefit expenses | 1,50,000 | |

| finance costs | 45,000 | |

| depreciation and amortization expenses | 82,000 | |

| other expenses | 2 | 50,000 |

| Total expenses | 11,02,000 | |

| v. profit before tax(iii-iv) | 1,16,000 | |

| Tax paid | 36,000 | |

| vi. profit for the period | 80,000 |

Notes:

| (1) other income: | ₹ | (2) other expenses: | ₹ |

| Profit on sale of land | 15,000 | Loss on sale of plant | 30,000 |

| Insert received | 3,000 | Office expenses | 20,000 |

| 18,000 | 50,000 |

Note (3): depreciation and amortization expenses:

| Depreciation | = | 72,000 |

| Goodwill written of | = | 10,000 |

| 82,000 |

Additional information:

| As on 31st March 2021 | As on 31st March 2022 | |

| Trade receivable | 1,40,000 | 1,64,000 |

| Inventory | 84,000 | 1,15,000 |

| Trade payable | 60,000 | 73,000 |

| Office expenses outstanding | 6,000 | 4,000 |

The solution of Question 17 Chapter 8 – Unimax Publication Class 12 Part 2-2021 : –

Cash flow from operating activities

for the year ended 31st march ,2022

| ₹ | ||

| Net profit before tax (note1) | 1,16,000 | |

| Adjustment for non-cash and non- operating items: | ||

| Add: finance costs | 45,000 | |

| Depreciation | 72,000 | |

| Goodwill written off | 10,000 | |

| Loss on sale of plant | 30,000 | |

| 2,73,000 | ||

| Less: profit on sale of land | 15,000 | |

| Insert received | 3,000 | 18,000 |

| Operating profit before working capital change | 2,55,000 | |

| Add: increase in current liabilities: | ||

| Trade payable | 13,000 | |

| 2,68,000 | ||

| Less: increase in current assets: | ||

| Trade receivables | 24,000 | |

| Inventory | 31,000 | |

| Less: decrease in current liabilities: | ||

| Outstanding exp. | 2,000 | 57,000 |

| Cash generated from operating activities | 2,11,000 | |

| Less: tax paid | (36,000) | |

| Net cash from operating activities | 1,75,000 | |

Note: (1) calculation of net profit before Tax:

| Profit for the period | = | 80,000 |

| Add: provision for Tax (Tax paid) | = | 36,000 |

| 1,16,000 |

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

What is the cash flow statement? why do we need to prepare?

Unimax Publication – Accountancy PSEB Class 12 – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Change in Profit sharing ratio among Existing Partners )

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Unimax Publication – Accountancy PSEB (Class 12) – Part – II – Solution

- Chapter No. 1 – Company Accounts (Share Capital)

- Chapter No. 2 – Company Accounts (Issue of Debentures)

- Chapter No. 3 – Company Accounts (Redemption of Debentures)

- Chapter No. 4 – Financial Statements of a Company

- Chapter No. 5 – Financial Statement Analysis

- Chapter No. 6 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 7 – Ratio Analysis

- Chapter No. 8 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2023@ Official Website of Sultan Chand Publication