Question 12 Chapter 4 – Unimax Class 12 Part 1

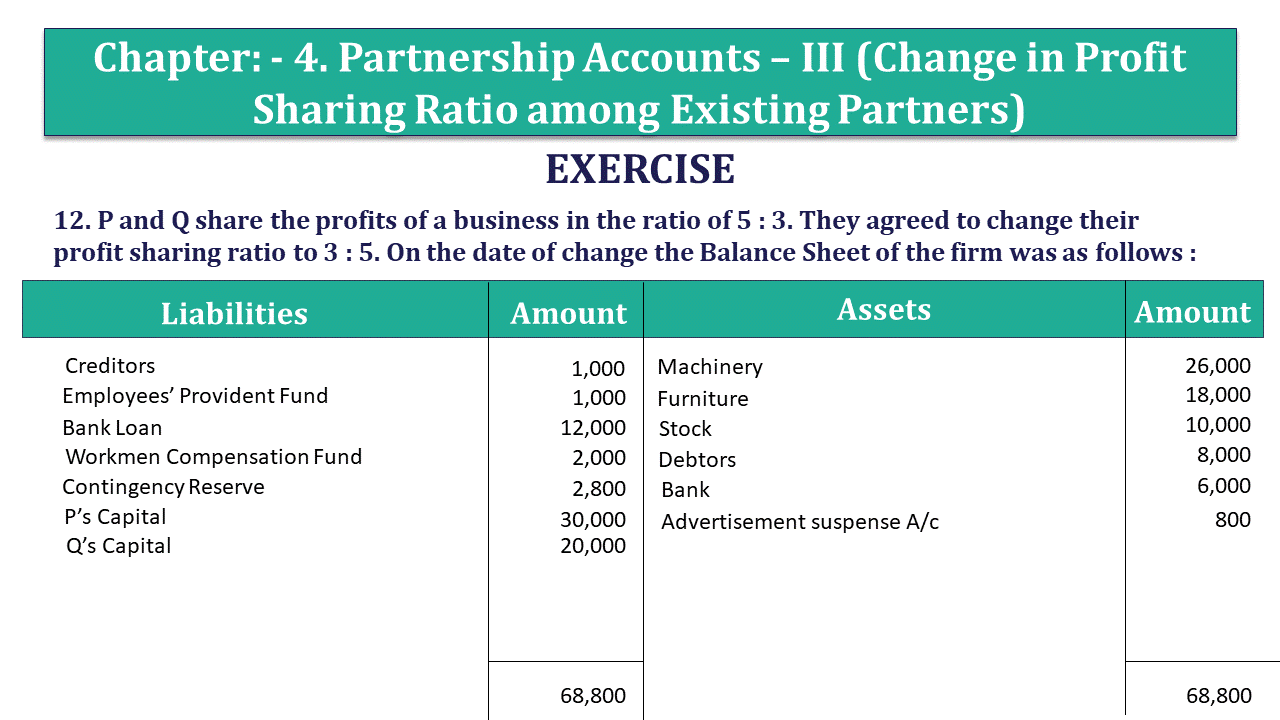

12. P and Q share the profits of a business in the ratio of 5 : 3. They agreed to change their profit sharing ratio to 3 : 5. On the date of change the Balance Sheet of the firm was as follows :

| Liabilities | Amount | Assets | Amount | |

| Creditors | 1,000 | Machinery | 26,000 | |

| Employees’ Provident Fund | 1,000 | Furniture | 18,000 | |

| Bank Loan | 12,000 | Stock | 10,000 | |

| Workmen Compensation Fund | 2,000 | Debtors | 8,000 | |

| Contingency Reserve | 2,800 | Bank | 6,000 | |

| P’s Capital | 30,000 | Advertisement suspense A/c | 800 | |

| Q’s Capital | 20,000 | |||

| 68,800 | 68,800 |

There also decide that :

1. Goodwill of the firm be valued at 4 years’ purchase of Super profits. The average super profits of the last three years are Rs. 20,000, while the normal profits that can be earned with Capital employed are Rs. 12,000.

2. Furniture be appreciated by Rs. 6,000 and value of stock to be reduced by 20%. You are required to prepare Revaluation Account, Partners’ Capital Accounts and the Balance Sheet of reconstituted Firm. (Accumulated profits and losses are to be distributed and assets will appear at revalued figures in Balance Sheet.)

The solution of Question 12 Chapter 4 – Unimax Class 12 Part 1

Revaluation A/c

| Particulars | Rs. | Particulars | Rs. | |

| To Stock | 2000 | By Furniture | 6000 | |

| To Profit transferred | ||||

| P (4000 X 5/8) | 2500 | |||

| Q (4000 X 3/8) | 1500 | 4000 | ||

| 6000 | 6000 |

Capital Accounts

| Particulars | P | Q | Particulars | P | Q |

| To P’s Capital A/c (Share of goodwill) | _ | 8000 | By Balance b/d | 30000 | 20000 |

| To Advertisement suspense A/c | 500 | 300 | By Revaluation A/c (Profit) | 2500 | 1500 |

| To Balance c/d | 43000 | 15000 | By Q’s Capital a/c (share of goodwill) | 8000 | _ |

| By workmen comp. fund | 1250 | 750 | |||

| By Reserves A/c | 1750 | 1050 | |||

| 43500 | 23300 | 43500 | 23300 |

Balance Sheet of Reconstituted firm

| Liabilities | Rs. | Assets | Rs. | |

| Creditors | 1000 | Bank | 6000 | |

| Bank Loan | 12000 | Debtors | 8000 | |

| Employees provident fund | 1000 | Stock | 8000 | |

| Capital Accounts | Furniture | 24000 | ||

| P : | 43300 | Machinery | 26000 | |

| Q : | 15000 | 58000 | ||

| 72000 | 72000 |

Working Note :

Calculation of Sacrifice/Gain

| Old Share | New Share | Difference |

| P 5/8 | 3/8 | 2/8 (Sacrifice) |

| Q 3/8 | 5/8 | 2/8 (Gain) |

2. Calculation of goodwill

Super Profits = Average Profits – Normal Profits

= Rs. 20000 – Rs. 12000 = Rs. 8000

Goodwill = Rs. 8000 X 4 = Rs. 32000

Q will pay to P, share of goodwill

i.E (32000 X 1/4) = Rs. 8000, sacrificed by P.

What is Partnership – Meaning and Its 4 Types

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication