Problem 4 Chapter 6 – Unimax

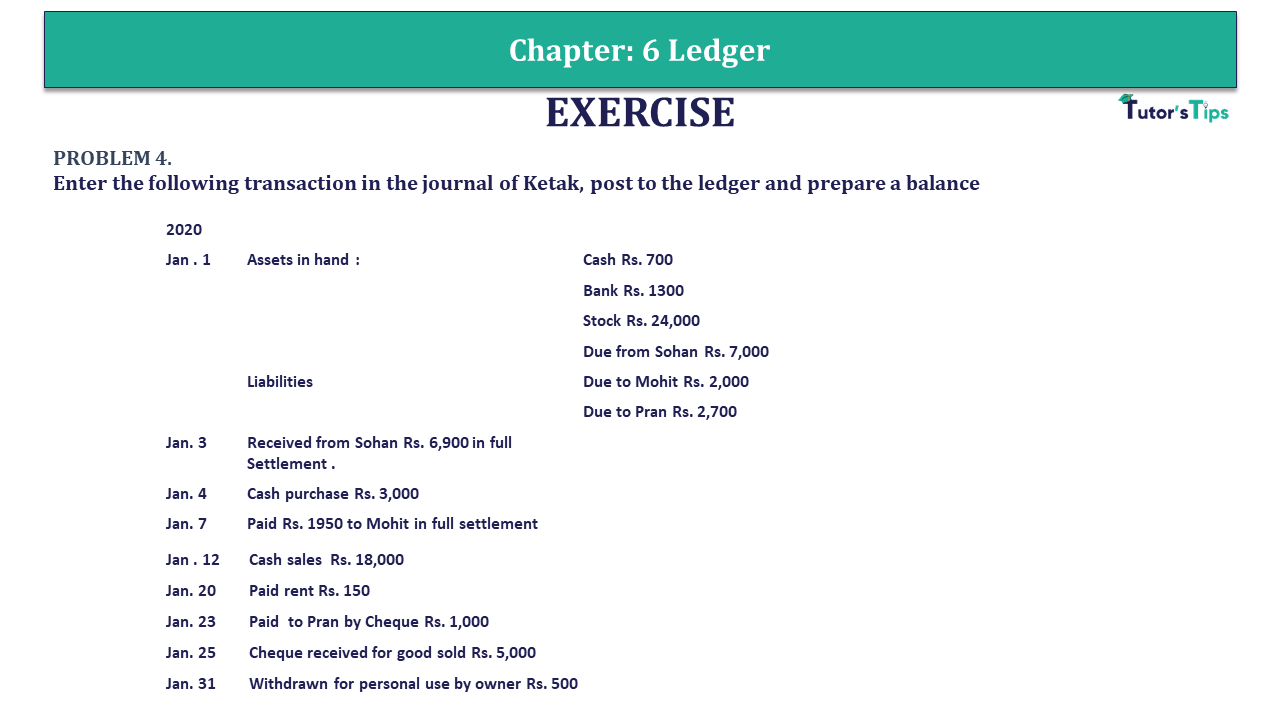

PROBLEM 4.

Enter the following transaction in the journal of Ketak, post to the ledger and prepare a balance

| 2020 | |

| Jan . 1 | Assets in hand: Cash Rs. 700 |

| Bank Rs. 1300 | |

| Stock Rs. 24,000 | |

| Due from Sohan Rs. 7,000 | |

| Liabilities: Due to Mohit Rs. 2,000 | |

| Due to Pran Rs. 2,700 | |

| Jan. 3 | Received from Sohan Rs. 6,900 in full Settlement. |

| Jan. 4 | Cash purchase Rs. 3,000 |

| Jan. 7 | Paid Rs. 1950 to Mohit in full settlement |

| Jan.12 | Cash sales Rs. 18,000 |

| Jan. 20 | Paid rent Rs. 150 |

| Jan. 23 | Paid to Pran by Cheque Rs. 1,000 |

| Jan. 25 | Cheque received for good sold Rs. 5,000 |

| Jan. 31 | Withdrawn for personal use by owner Rs. 500 |

The solution of Problem 4 Chapter 6 – Unimax:

JOURNAL

| Date | Particulars | L.F. | Debit | Credit | |

| 2020 | |||||

| Jan. 1 | Cash A/C | Dr. | 700 | ||

| Bank A/C | Dr. | 1,300 | |||

| Stock A/C | Dr. | 24,000 | |||

| Sohan’s A/c | Dr. | 7,000 | |||

| To Mohit’s A/c | 2,000 | ||||

| To Pran’s A/C | 2,700 | ||||

| To Capital A/c | 28,300 | ||||

| (Being opening balances brought forward) | |||||

| Jan. 3 | Cash A/c | Dr. | 6,900 | ||

| Discount A/c | Dr. | 100 | |||

| To Sohan’s A/c | 7,000 | ||||

| (Being cash received from Sohan in full settlement) | |||||

| Jan. 4 | Purchases A/c | Dr. | 3,000 | ||

| To Cash A/c | 3,000 | ||||

| (Being goods purchased in cash) | |||||

| Jan. 7 | Mohit’s A/c | Dr. | 2,000 | ||

| To Cash A/c | 1,950 | ||||

| To Discount A/C | 50 | ||||

| (Being paid to Mohit in full settlement) | |||||

| Jan. 12 | Cash A/c | Dr. | 18,000 | ||

| To Sales A/c | 18,000 | ||||

| (Being goods sold in cash) | |||||

| Jan. 20 | Rent A/c | Dr. | 150 | ||

| To Cash A/c | 150 | ||||

| (Being rent paid in cash) | |||||

| Jan. 23 | Pran’s A/c | Dr. | 1,000 | ||

| To Bank A/c | 1,000 | ||||

| (Being paid to pran by cheque) | |||||

| Jan. 25 | Bank A/c | Dr. | 5,000 | ||

| To Sales A/c | 5,000 | ||||

| (Being goods sold &cheque received) | |||||

| Jan. 3 | Drawings A/c | Dr. | 500 | ||

| To Cash A/c | 500 | ||||

| (Being cash withdrawn by owner) | |||||

| Grand Total | 64,950 | 64,950 | |||

LEDGER BOOKS OF KETAK :

CASH ACCOUNT

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 1 | To Balance b/d | 700 | Jan. 4 | By Purchases A/c | 3,000 |

| Jan. 3 | To Sohan’s A/c | 6,900 | Jan. 7 | By Mohit’s A/c | 1,950 |

| Jan. 12 | To Sales A/c | 18,000 | Jan. 20 | By Rent A/c | 150 |

| Jan. 31 | By Drawings A/c | 500 | |||

| Jan. 31 | By Balance c/d | 20,000 | |||

| 25,600 | 25,600 | ||||

| Feb. 1 | To Balance b/d | 20,000 |

BANK ACCOUNT

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 1 | To Balance c/d | 1,300 | Jan. 23 | By Pran’s A/c | 20,000 |

| Jan. 25 | To Sales A/c | 5,000 | Jan. 31 | By Balance b/d | 5,300 |

| 6,300 | 6,300 | ||||

| Feb. 1 | To Balance b/d | 5,300 |

STOCK ACCOUNT

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 1 | To Balance c/d | 24,000 | Jan. 31 | By Balance b/d | 24,000 |

| 24,000 | 24,000 | ||||

| Feb. 1 | To Balance b/d | 24,000 |

SOHAN’S ACCOUNT

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 1 | To Balance b/d | 7,000 | Jan. 3 | By Pran’s A/c | 6,900 |

| Jan. 3 | By Balance b/d | 100 | |||

| 7,000 | 7,000 |

MOHIT’S ACCOUNT

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 7 | To Cash A/c | 1,950 | Jan. 1 | By Balance b/d | 2,000 |

| Jan. 7 | To Discount A/c | 50 | |||

| 2,000 | 2,000 |

PRAN’S ACCOUNT

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 23 | To Bank A/c | 1,000 | Jan. 1 | By Balance b/d | 2,700 |

| Jan. 31 | To Balance c/d | 1,700 | |||

| 2,700 | 2,700 | ||||

| Feb. 1 | By Balance b/d | 1,700 |

CAPITAL ACCOUNT

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 31 | To Balance c/d | 28,300 | April 1 | By balance b/d | 16,000 |

| 28,300 | 16,000 | ||||

| Feb. 1 | By Balance b/d | 28,300 |

DISCOUNT A/C

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 3 | To SOHAN’s A/c | 100 | Jan. 7 | By Mohit’s A/c | 50 |

| Jan. 31 | By Balance C/d | 50 | |||

| 100 | 100 | ||||

| Feb. 1 | To Balance b/d | 50 |

PURCHASE A/C

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 4 | To Cash A/c | 3,000 | |||

| Jan. 31 | By Balance C/d | 3,000 | |||

| 3,000 | 3,000 | ||||

| Feb. 1 | To Balance b/d | 3,000 |

SALES ACCOUNT

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 31 | To Balance c/d | 23,000 | Jan. 12 | By Cash A/c | 18,000 |

| Jan. 25 | By Bank A/c | 5,000 | |||

| 23,000 | 23,000 | ||||

| Feb. 1 | To Balance b/d | 23,000 |

RENT A/C

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 20 | To Cash A/c | 150 | Jan. 31 | By Balance C/d | 150 |

| 100 | 150 | ||||

| Feb. 1 | To Balance b/d | 150 |

DRAWINGS A/C

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2020 | 2020 | ||||

| Jan. 20 | To Cash A/c | 500 | Jan. 31 | By Balance C/d | 500 |

| 500 | 500 | ||||

| Feb. 1 | To Balance b/d | 500 |

TRIAL BALANCE OF KETAK AS ON JAN. 31, 2020:

| Date | Name of Accounts | L.F. | Debit (₹) | Credit (₹) |

| 1 | Cash A/c | 20,000 | ||

| 2 | Bank A/c | 5,300 | ||

| 3 | Stock A/c | 24,000 | ||

| 4 | Pran’s A/c | 1,700 | ||

| 5 | Capital A/c | 28,300 | ||

| 6 | Discount A/c | 50 | ||

| 7 | Purchases A/c | 30,000 | ||

| 8 | Sales A/c | 23,000 | ||

| 9 | Rent A/c | 150 | ||

| 10 | Drawings A/c | 500 | ||

| Total | 53,000 | 53,000 |

This is all about the Problem 4 Chapter 6 – Unimax. You can check out the following article to better understand:

Ledger balancing or Closing of ledger account | Ledger

You Can also read all above articles in Hindi on our Hindi Website

Ledger balancing or Closing of ledger account | Ledger – In Hindi

Thanks, Please Like and share with your friends

Comment if you have any doubt in the Problem 4 Chapter 6 – Unimax.

You can also Check out the solved question of other Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST) : An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconlciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may Choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Compurters and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software : Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

You can also Check out the other Books’ Solution: –

- Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

- T.S. Grewal’s Double Entry Book Keeping (Class +1) – Solution

- D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution