Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

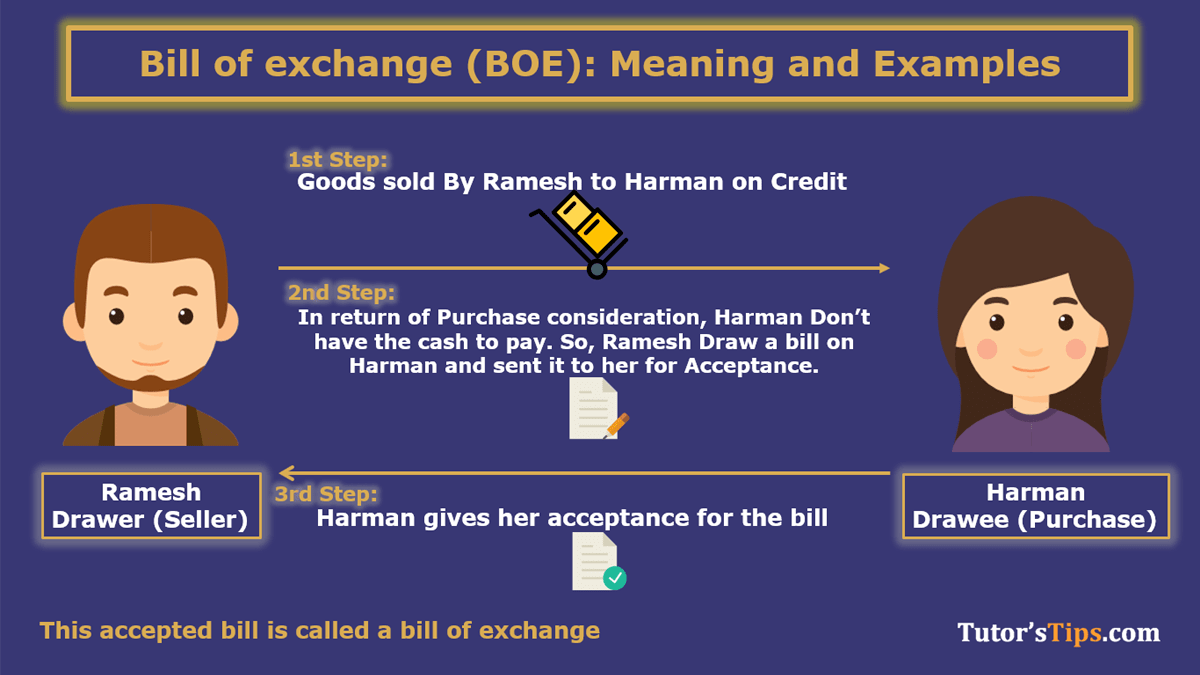

विनिमय बिल (Bill Of Exchange) एक ऐसा साधन है जिसमें एक निश्चित अवधि के बाद किसी निश्चित व्यक्ति (person) को कुछ राशि का भुगतान करने का वादा होता है। यह (Bill Of Exchange) आम तौर पर लेनदार (निर्माता या दराज) द्वारा अपने देनदार (स्वीकर्ता या ड्रेवे) पर तैयार किया जाता है और देनदार यह स्वीकार करता है कि वह एक निश्चित अवधि या विशिष्ट तिथि के बाद निर्माता (दराज) को पैसे का भुगतान करेगा। इसे(Bill Of Exchange) उस व्यक्ति द्वारा स्वीकार किया जाना चाहिए जिसे इसे बनाया गया है या उसकी ओर से किसी अन्य व्यक्ति द्वारा। स्वीकृति के बिना, इस दस्तावेज़ का कोई मूल्य नहीं है।

"विनिमय का बिल (Bills Of Exchange) एक बिना शर्त के आदेश को लिखने में एक उपकरण है, जो निर्माता द्वारा हस्ताक्षरित होता है, एक निश्चित व्यक्ति को केवल एक निश्चित राशि का भुगतान करने के लिए निर्देश देता है, या एक निश्चित व्यक्ति को, या किसी व्यक्ति के आदेश पर साधन। "

-Section 5 of India's Negotiable Instruments Act, 1881

इसमें तीन पक्ष शामिल हैं, जिन्हें निम्नानुसार दिखाया गया है: -इसमें तीन पक्ष शामिल हैं, जिन्हें निम्नानुसार दिखाया गया है: -

आहर्ता वह व्यक्ति है जो अपने देनदार पर विनिमय का बिल बनाता है और वह इसमें उल्लेखित धन का एक रिसीवर भी होगा। वस्तुओं और सेवाओं के विक्रेता को एक दराज के रूप में जाना जाता है (उम्मीद है कि कुछ मामले आगे बताएंगे)।

द्रव्य वह व्यक्ति होता है जिसे बिल का आदान-प्रदान किया जाता है और वह बिल की परिपक्वता के समय इसमें उल्लिखित राशि का भुगतान करेगा। वस्तुओं और सेवाओं की खरीद को एक घबराहट के रूप में जाना जाता है (उम्मीद है कि कुछ मामले आगे बताएंगे)। ड्रेवे को स्वीकारकर्ता के रूप में भी जाना जाता है क्योंकि वह उल्लिखित राशि का भुगतान निर्दिष्ट तिथि पर या एक विशिष्ट अवधि के बाद करने की स्वीकृति देता है।

जिस व्यक्ति को भुगतान किया जाता है उसे भुगतानकर्ता के रूप में जाना जाता है। मूल रूप से, बिल के दराज को आदाता के रूप में जाना जाता है, लेकिन कुछ मामलों में जिसमें बिल को ड्रावर द्वारा अपने पास नहीं रखा जाता है, तो भुगतानकर्ता वह व्यक्ति होगा जिसके पास बिल है। निम्नलिखित मामलों में दराज को आदाता के रूप में नहीं माना जाएगा: -

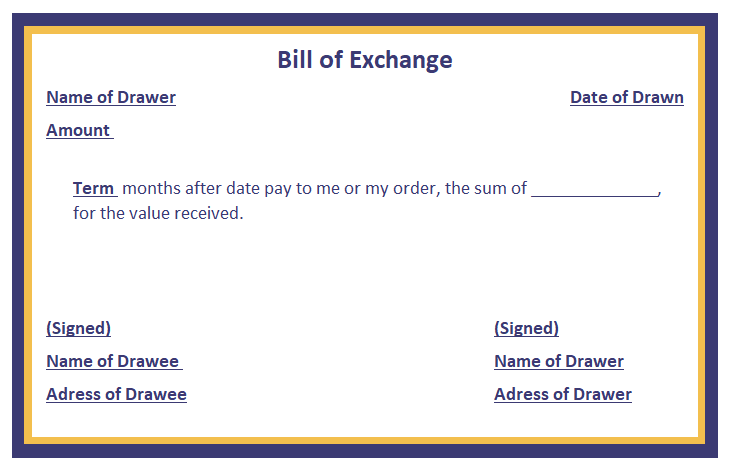

एक्सचेंज के बिलों में निम्नलिखित सामग्रियां शामिल हैं: -

"बिल ऑफ एक्सचेंज" शीर्षक का उल्लेख दस्तावेज़ के चेहरे पर किया जाएगा।

इस पर एक बिल तैयार करने की तारीख लिखी जानी चाहिए।

देय राशि को उस पर आंकड़ों में और शब्दों में भी वर्णित किया जाएगा।

इस पर विशिष्ट तिथि या बिल की अवधि का उल्लेख किया जाएगा। शब्द का अर्थ है 2 महीने या 3 महीने आदि। यह शब्द बिल का कार्यकाल है और बिल की तारीख से चलता है। बिल की कुल अवधि के अलावा 3 दिनों की एक अनुग्रह अवधि होगी।

हर बिल की एक विशिष्ट पहचान संख्या होती है। उस पर इसका उल्लेख किया जाएगा।

विधेयक पर दोनों पक्षों के नाम का उल्लेख किया जाएगा।

बिल पर दोनों पक्षों के हस्ताक्षर भी हैं।

निम्न छवि बीओई के नमूने को दिखाती है।

ये एक्सचेंज के बिल के कुछ सबसे पुराने मूल दस्तावेज हैं।

एक्सचेंज, रंगून, बर्मा का 1939 बिल।

लंदन में एक्सचेंज का 1870 का बिल ब्रिटिश फॉरेन बिल रेवेन्यू स्टैम्प के साथ देय है

विनिमय के बिलों का लेखा-जोखा निम्नलिखित हैडिंग और सबहेडिंग के तहत वर्णित किया जा सकता है: -

मामले में, जहां ड्रॉ परिपक्वता की तिथि पर बिल की राशि का भुगतान करता है, क्योंकि बिल को परिपक्वता तिथि पर सम्मानित किया जाता है। नीचे बताई गई स्थिति के चार प्रकार हैं: -...

दराज बिल की परिपक्वता तिथि तक बिल रखता है और उस तारीख को बिल को विधिवत भुगतान किया जाता है। फिर नीचे दी गई तालिका में दिखाई गई इन प्रक्रिया का लेखांकन उपचार: -

मान लीजिए कि ड्रावर का नाम X है और ड्रेव का नाम Y है

| S. No. | Transactions | In the Books of Drawer | In the Books of Drawee | ||

|---|---|---|---|---|---|

| 1 | When goods sold to Mr Y by Mr X. | Y's A/c

To Sales A/c (Being goods sold to Mr Y, on credit ) |

Dr. | Purchase A/c

To X's A/c (Being goods Purchase from Mr X, on credit ) |

Dr. |

| 2 | Bill is drawn by Mr X, on the Mr Y and duly accepted by the Mr Y | Bills Receivable A/c

To Y's A/c (Being the acceptance received of the bill receivable from Mr Y) |

Dr. | X's A/c

To Bills Payable A/c (Being acceptance of the bill given to Mr X ) |

Dr. |

| 3 | On maturity, the bill is duly paid by the Mr Y | Bank A/c

To Bills receivable A/c (Being payment received against the bill receivable) |

Dr. | Bills Payable A/c

To Bank A/c (Being payment made against the bills receivable ) |

Dr. |

दराज ने बिल की परिपक्वता की तारीख से पहले बैंक से बिल में छूट दी और बिल को परिपक्वता तिथि पर विधिवत भुगतान किया गया। फिर नीचे दी गई तालिका में दिखाई गई इन प्रक्रिया का लेखांकन उपचार: -

फर्स्ट और सेकंड जर्नल एंट्री उपरोक्त प्रकार के साथ ही रहती है। तृतीय पत्रिका प्रविष्टि केवल निम्न तालिका में दर्शाई गई दराज की पुस्तकों में बदली जाएगी: -

| S. No. | Transactions | In the Books of Drawer | In the Books of Drawee | ||

|---|---|---|---|---|---|

| 3 | Bill is discounted by the drawer from the bank | Bank A/c

Discount A/c To Bills Receivable A/c (Being B/R discounted from the bank account before the maturity date) |

Dr.

Dr. |

No entry | |

| 3 | On maturity, the bill is duly paid by the Mr Y | No entry | Bills Payable A/c

To Bank A/c (Being payment made against the bills receivable ) |

Dr. | |

यह परिपक्वता की तारीख से पहले प्राप्य बिलों के खिलाफ भुगतान करने के लिए बैंक की राशि से ब्याज की राशि है। ब्याज की राशि की गणना शेष अवधि के लिए की जाएगी जब तक बिलों की परिपक्वता प्राप्य नहीं हो जाती।

जब ड्रॉअर बिलों का समर्थन करता है, तो उसके लेनदार को प्राप्त होने वाला बिल एक्सचेंज के बिल के समर्थन के रूप में जाना जाता है और बिल को विधिवत परिपक्वता तिथि पर भुगतान किया जाता है। फिर नीचे दी गई तालिका में दिखाई गई इन प्रक्रिया का लेखांकन उपचार: -

फर्स्ट और सेकंड जर्नल एंट्री उपरोक्त प्रकार के साथ ही रहती है। तृतीय पत्रिका प्रविष्टि केवल निम्न तालिका में दर्शाई गई दराज की पुस्तकों में बदली जाएगी: -

*Suppose the X have creditor named Mr Z: -

| S. No. | Transactions | In the Books of Drawer | In the Books of Drawee | ||

|---|---|---|---|---|---|

| 3 | Bill is endorsed by the drawer to his/her Creditor. | Z's A/c

To Bills Receivable A/c (Being B/R endorse to Mr Z) |

Dr. | No entry | |

| 3 | On maturity, the bill is duly paid by the Mr Y | No entry | Bills Payable A/c

To Bank A/c (Being payment made against the bills receivable ) |

Dr. | |

यहां पूरी प्रक्रिया में शामिल तीसरा व्यक्ति होगा। तो, हमें इस व्यक्ति के लिए भी किताबें तैयार करनी होंगी। यह नीचे दिखाया गया है: -

| S. No. | Transactions | In the Books of Endorsee | |

|---|---|---|---|

| 1 | Bill is endorsed by the drawer to his/her Creditor. | Bills Receivable A/c

To X's A/c (Being B/R received from Mr X) |

Dr. |

| 2 | On maturity, the bill is duly paid by the Mr Y | Bank A/c

To Bills receivable A/c (Being payment received against the bill receivable) |

Dr. |

जब ड्रॉअर ने अपने बैंक को परिपक्वता तिथि पर बिल के संग्रह के लिए प्राप्य बिलों को भेजा तो उसे संग्रह के लिए भेजे गए बिल के रूप में जाना जाता है और बिल को विधिवत परिपक्वता तिथि पर भुगतान किया जाता है। फिर नीचे दी गई तालिका में दिखाई गई इन प्रक्रिया का लेखांकन उपचार: -

फर्स्ट और सेकंड जर्नल एंट्री उपरोक्त प्रकार के साथ ही रहती है। तृतीय पत्रिका प्रविष्टि को केवल निम्न तालिका में दर्शाई गई दराज की पुस्तकों में दो-भाग में बदला और पोस्ट किया जाएगा: -

| S. No. | Transactions | In the Books of Drawer | In the Books of Drawee | ||

|---|---|---|---|---|---|

| 3 | Bill sent for collection to the bank by Mr X. | Bill sent for collection A/c

To Bills Receivable A/c (Being B/R endorse to the Mr Z) |

Dr. | No entry | |

| 4 | On maturity, the bill is duly paid by the Mr Y | Bank A/c

To Bills sent for collection A/c (Being payment collected by the bank against the bill receivable) |

Dr. | Bills Payable A/c

To Bank A/c (Being payment made against the bills receivable ) |

Dr. |

यदि परिपक्वता की तिथि पर बिल की राशि का भुगतान नहीं किया जाता है तो मामले में परिपक्वता तिथि पर बिल का अनादर किया जाता है। नीचे बताई गई स्थिति के चार प्रकार हैं: -

सभी जर्नल प्रविष्टियाँ समान हैं, लेकिन केवल अंतिम लेन-देन सभी मामलों में बदल जाएगा, निम्न तालिका में दिखाया गया है: -

| S. No. | Transactions | In the Books of Drawer | In the Books of Drawee | ||

|---|---|---|---|---|---|

| 3 | 1st Case

Retain by the drawer, till the date of maturity. |

Y's A/c

To Bills Receivable A/c To Cash A/c (noting charges If any) (Being B/R dishonoured on the maturity and noting charges paid to the bank) |

Dr. | Bills Payable A/c

Noting Charges A/c To X's A/c (Being B/P dishonoured on the maturity and noting charges paid to the bank by Mr X ) |

Dr.

Dr. |

| 3 | 2nd Case

A bill discounted by the drawer from the bank before the maturity date. |

Y's A/c

To Bank A/c (add: noting charges If any) (Being B/R dishonoured on the maturity and noting charges paid to the bank) |

Dr. | Bills Payable A/c

Noting Charges A/c To X's A/c (Being B/P dishonoured on the maturity and noting charges paid to the bank by Mr X ) |

Dr.

Dr. |

| 3 | 3rd Case

Endorse the bill by the drawer to his/her creditor . |

Y's A/c

To Z's A/c (add: noting charges If any) (Being B/R dishonoured on the maturity and noting charges paid by Mr Z to the bank) |

Dr. | Bills Payable A/c

Noting Charges A/c To X's A/c (Being B/P dishonoured on the maturity and noting charges paid to the bank by Mr X ) |

Dr.

Dr. |

| 3 | 4th Case

The bill sent for collection . |

Y's A/c

To Bill sent fro collection A/c To Bank A/c (noting charges If any) (Being B/R dishonoured on the maturity and noting charges paid to the bank) |

Dr. | Bills Payable A/c

Noting Charges A/c To X's A/c (Being B/P dishonoured on the maturity and noting charges paid to the bank by Mr X ) |

Dr.

Dr. |

| S. No. | Transactions | In the Books of Endorsee | |

|---|---|---|---|

| 2 | On maturity, the bill is duly paid by the Mr Y | X's A/c

To Bills receivable A/c To Cash A/c (noting charges If any) (Being B/R dishonoured on the maturity and noting charges paid to the bank) |

Dr. |

कभी-कभी, बिल स्वीकार करने वाला पाता है कि वह बिल की देय तिथि पर बिल की राशि का भुगतान नहीं कर सकता है। बिल के अनादर से बचने के लिए, वह दराज से अनुरोध कर सकता है कि वह बिल को कुछ ब्याज के साथ या बिना ब्याज के नवीनीकृत करे। यदि ड्रॉअर इसके लिए सहमत होता है तो उन्होंने पुराने बिल को रद्द कर दिया और ब्याज राशि के साथ या ब्याज राशि (नकद में प्राप्त ब्याज) के साथ एक नया बिल बना सकते हैं।

तो, बिल का लेखांकन उपचार नीचे दिखाया गया है: -

| S. No. | Transactions | In the Books of Drawer | In the Books of Drawee | ||

|---|---|---|---|---|---|

| 1 | Cancellation of the Old bill | Y's A/c

To Bills Receivable A/c (Being old bill cancelled before the maturity date ) |

Dr. | Bills payable A/c

To X's A/c (Being old bills payable cancelled before the maturity date ) |

Dr. |

| 2 | Interest charges on the amount of the bill for the extended period.

if paid in cash by Mr Y |

Cash A/c

To Interest A/c (Being interest received on the amount due from Mr Y) |

Dr. | Interest A/c

To Cash A/c (Being interest paid to Mr x on the amount due to him ) |

Dr. |

| 2 | If interest not paid in cash | Y's A/c

To Interest A/c ( Being interest due on the amount due from Mr Y ) |

Dr. | Interest A/c

To X's A/c (Being interest due to Mr X ) |

Dr. |

| 3. | When the new bill received from Mr Y | Bills Receivable A/c

To Y's A/c (Being acceptance received of the new bill) |

Dr. | X's A/c

To Bills Payable A/c (Being acceptance given for new bill ) |

Dr. |

कभी-कभी, स्वीकर्ता के पास बिल की परिपक्वता तिथि से पहले बिल का भुगतान करने के लिए पर्याप्त निधि होती है। दराज कुछ छूट देगा क्योंकि परिपक्वता से पहले भुगतान की गई राशि।

तो, बिल का लेखांकन उपचार नीचे दिखाया गया है: -

| S. No. | Transactions | In the Books of Drawer | In the Books of Drawee | ||

|---|---|---|---|---|---|

| 1 | When Y paid cash for the bills before the due date. | Cash A/c

Rebate A/c To Bills Receivable A/c (Being Bill retire before the due date and allow the rebate) |

Dr.

Dr. |

Bills payable A/c

To X's A/c To Rebate A/c (Being Bill retire before the due date and received the rebate) |

Dr. |

कभी-कभी, स्वीकर्ता को अदालत द्वारा दिवालिया घोषित कर दिया जाएगा। जब उसके पास अपनी देनदारियों का भुगतान करने के लिए नकदी या संपत्ति नहीं है।

तो, बिल का लेखांकन उपचार नीचे दिखाया गया है: -

| S. No. | Transactions | In the Books of Drawer | In the Books of Drawee | ||

|---|---|---|---|---|---|

| 1 | When Acceptor or Drawee declare insolvent. ( pass journal entry as same with Bill dishonoured ) | Y's A/c

To Bills Receivable A/c (Being Bill dishonoured due to Drawee declare insolvent ) |

Dr. | Bills payable A/c

To X's A/c (Being Bill dishonoured due to insolvency ) |

Dr. |

| 2 | Some portion of the total amount due received | Cash A/c

Bad Debts A/c To Y's A/c (Being only some portion is recovered from the Y's due to the declare insolvent) |

Dr. | X's A/c

To Cash A/c To Deficiency A/c (Being the amount due to X settled ) |

Dr. |

| 2 | When nothing could be recovered from the total amount due. | Bad Debts A/c

To Y's A/c (Being nothing could be recovered from the Y's due to the declare insolvent) |

Dr. | X's A/c

To Deficiency A/c (Being the amount due to X write off ) |

Dr. |

धन्यवाद, कृपया शेयर करें

यदि आपका कोई प्रश्न है तो टिप्पणी करें

लेखाशास्त्र और वाणिज्य शिक्षक (Accounting & Commerce Educator)

सरबजीत सिंह (Sarbjit Singh) के पास B.Com और M.Com की डिग्री है और उन्हें डबल एंट्री बुककीपिंग, वित्तीय लेखांकन और व्यावसायिक अध्ययन सिखाने का 12 से अधिक वर्षों का अनुभव है।

इस लेख में "Bill of exchange (BOE): Meaning and Examples - In Hindi" को विस्तार से समझाया गया है, जिसमें परिभाषाएं, अवधारणाएं, मुख्य नियम और Hindi से संबंधित महत्वपूर्ण विवरण शामिल हैं।

हाँ, यह अध्ययन सामग्री कक्षा 11 और 12 के वाणिज्य (Commerce), लेखांकन (Accounting) और अर्थशास्त्र (Economics) के छात्रों के साथ-साथ CA फाउंडेशन की परीक्षाओं के लिए भी अत्यंत उपयोगी है।

आप हमारे मुख्य अभ्यास केंद्र (Practice Center) पर जाकर इसी विषय से संबंधित प्रश्नों और ऑनलाइन क्विज़ का अभ्यास कर सकते हैं।

{kind=link}