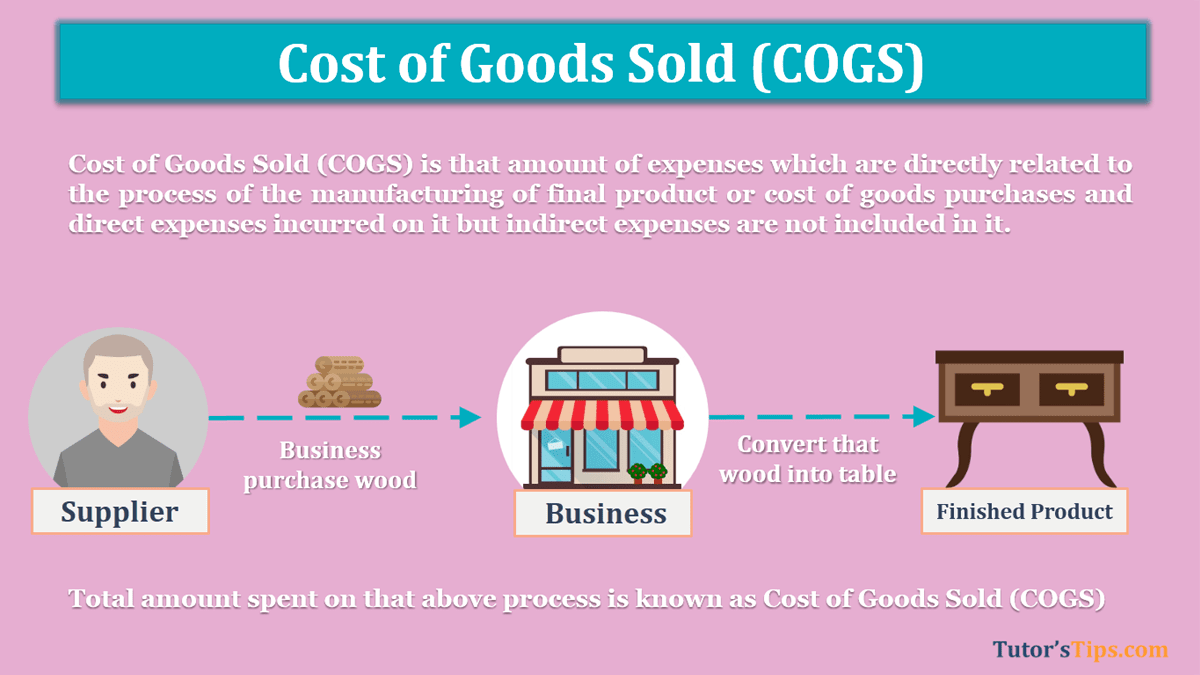

Cost of Goods Sold (COGS) is the amount of expenses that are directly related to the process of the manufacturing of the final product or cost of goods purchases and direct expenses incurred on it but indirect expenses are not included in it.

In all direct cost of the product in known as Cost of Goods Sold (COGS)

To understand the meaning of Cost of Goods Sold (COGS) more simply, first we have to divide the business into two types. These are shown below:

Types of Business:

- Production Business

- Trading Business.

1. Production Business: –

In the Production Business, the amount which has spent by the business to produce finished products is known as the cost of goods sold (COGS). Examples are shown below: –

- Amount paid to purchase a Raw Material

- All Direct Expenses

2. Trading Business: –

The amount of expenses which has been spent by the business on the purchase of goods and bring these goods in-store is known as the cost of goods sold(COGS). It includes the purchase price of goods and all expenses incurred on the process of Purchase.

The formula of Cost of Goods Sold

COGS = Opening Inventory + Net Purchase + Direct Expenses – Closing Inventory

- Opening Inventory means the value of inventory which is available at the start of the financial year or the period for which we want to calculate the COGS. In financial year start from 01-April and ends on 31-march.

- Net Purchase means total purchase less purchase return within the current financial year or the period for which we want to calculate the COGS.

- Direct Expenses means that amount which the business spent on purchases of the material within the Financial year or the period for which we want to calculate the COGS.

- Closing Inventory means the value of inventory which is left at the end of the financial year or the period for which we want to calculate the COGS. In financial year start from 01-April and ends on 31-march.

Example for Cost of Goods Sold:

Example 1 for Production Business:

- Opening Inventory

- Raw Materials Rs. 50,000

- Work in progress Rs. 35,000

- Finished Stock Rs. 85,000

- Total Purchase Rs. 9,00,000

- Purchase Return Rs. 27,000

- Direct Expenses

- Carriage Paid Rs. 17,000

- Wages Rs. 1,80,000

- Factory Power Rs. 50,000

- Closing Inventory

- Raw Materials Rs. 70,000

- Work in progress Rs. 13,000

- Finished Stock Rs. 97,000

Solution: –

COGS= Opening Inventory + Net Purchase + Direct Expenses – Closing Inventory

= (50,000 + 35,000 + 85,000) + (9,00,000 – 27,000) + (17,000 + 1,80,000 + 50,000) – (79,000 + 13,000 + 97,000)

COGS = Rs. 11,10,000/-

Example 2 for Production Business:

- Opening Inventory Rs. 67,000

- Total Purchase Rs. 4,37,000

- Purchase Return Rs. 37,000

- Direct Expenses

- Carriage Paid Rs. 17,000

- Octroi Rs. 3,000

- Closing Inventory Rs. 88,000

Solution:-

COGS= Opening Inventory + Net Purchase + Direct Expenses – Closing Inventory

= 67,000 + (4,37,000 – 37,000) + (17,000 + 3,000) – 88,000

COGS=3,99,000/-

You can also read the following topics: –

- Assets – Meaning, Definition, Types and Examples

- Liabilities – Meaning, Types and Examples

- What is Capital – Meaning and Example

Thanks Please share with your friends

Comment if you have any question

Check out Financial Accounting Books @ Amazon.in