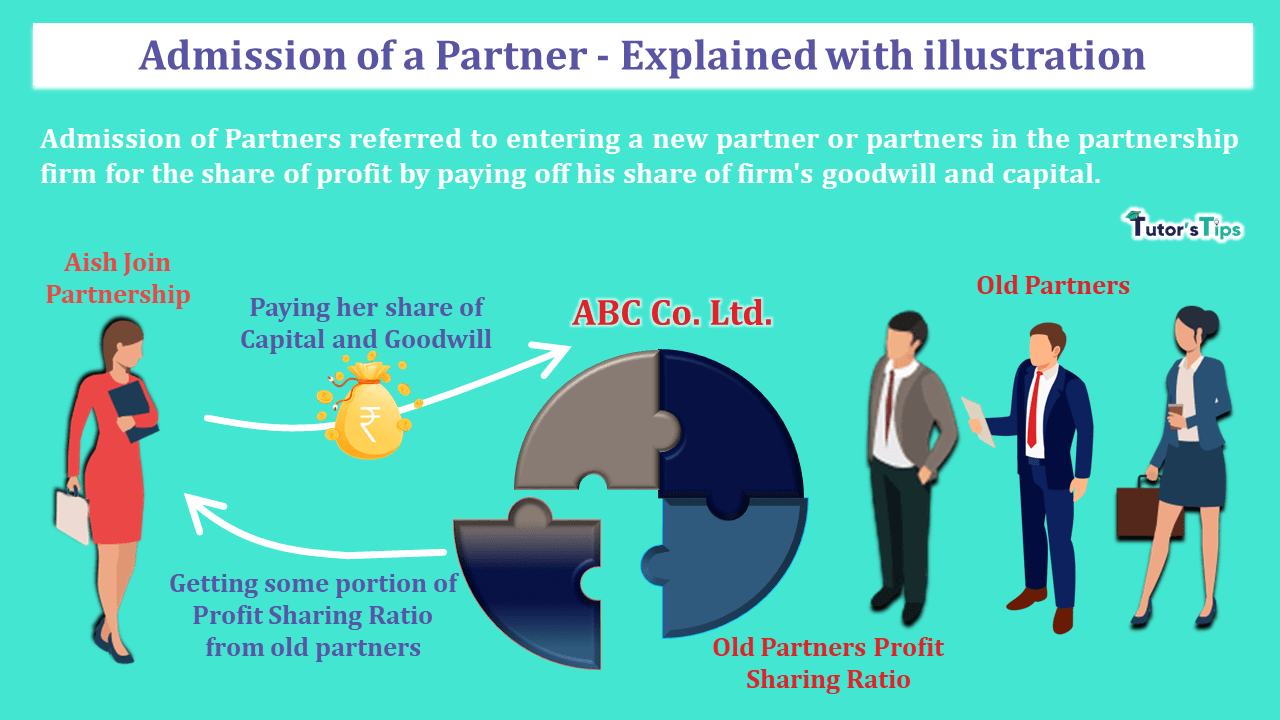

Admission of Partner referred to entering a new partner or partners in the partnership firm for the share of profit and paying off his or their share of the firm’s goodwill and capital. When the firm needs more funding or services/knowledge to grow their business then they approach to the new partner(s) against share in the profit of the firm with the consent of all old partners.

What is the Admission of Partner: –

The admission of the partner refers to the situation where an individual joins the existing partnership firm and the old partners are agree to sacrifice their share of profit. This is the mode of reconstitution of Partnership Because, with the admission of a new partner, there is a need to create a new agreement/deed between all partner including new partner and ends the existing agreement/deed.

There will be New profit sharing ration among all partners because the all(minimum one) old partners will sacrifice some portion of their profit share in the firm and the new partner will get some portion of the share of profit as per the deal with the old partners.

According to Section 31 of the Indian Partnership Act, 1932,

A person can be admitted as a new partner:

- if it is so agreed in the Partnership Deed, or

- in the absence of the above if all the partners agree for the admission.

after admission, the new partner gets the following two rights: –

- Right to share future profits of the firm, and

- Right to share in the assets of the firm.

at the same time, he becomes liable for any liability of the business incurred after admission and any loss incurred by the firm.

Effects of Admission of Partner: –

There will be the numbers of effects affecting the partnership and some of them are shown as follows: –

1. New Partnership Deed:

There should be a new partnership Deed/agreement between all partners included the new partner with all of new terms and condition acceptable to all partners. The old agreement will be abolished.

2. Share of Capital and Goodwill:

As per the agreement between the new partner and old partners, New partner has to bring his share of capital and goodwill in the firm as per his share of profits of the firm.

3. Adjustment for Reserve and Accumulated profit/loss: –

The old partners have to make the adjustment for the Reserve and Accumulated profit/loss in their old profit sharing ratio because these items are related to the period before the Admission of Partner.

4. Revaluation of Assets and Liabilities: –

At the time of admission of a partner, if old partners decide to know the true financial position of the firm then there will need to reevaluate all assets and liabilities of the firm.

5. Adjustment of the share of goodwill brought by the new Partner: –

The old partners will make adjustment of the share of goodwill brought by the new partners in their sacrificing ratio.

Adjustments required on the Admission of Partner: –

The adjustment which is required to make after the admission of the new partner is shown as following and these all are already explained in the previous articles, So please click on the name and check out these all article one by one.

- Change in Profit Sharing Ratio

- Valuation of Goodwill

- Adjustment for the Reserves, Accumulated profits/losses and Deferred revenue expenses.

- Revaluation of Assets and Liabilities

- Adjustment of Capital in Partnership

Thanks for reading the topic

please comment your feedback whatever you want. If you have any question please ask us by commenting.

Check out T.S. Grewal’s +2 Book 2020 @ Official Website of Sultan Chand Publication