Question No 59 Chapter 1 – UNIMAX Class 12 Part 2 – 2021

Table of Contents

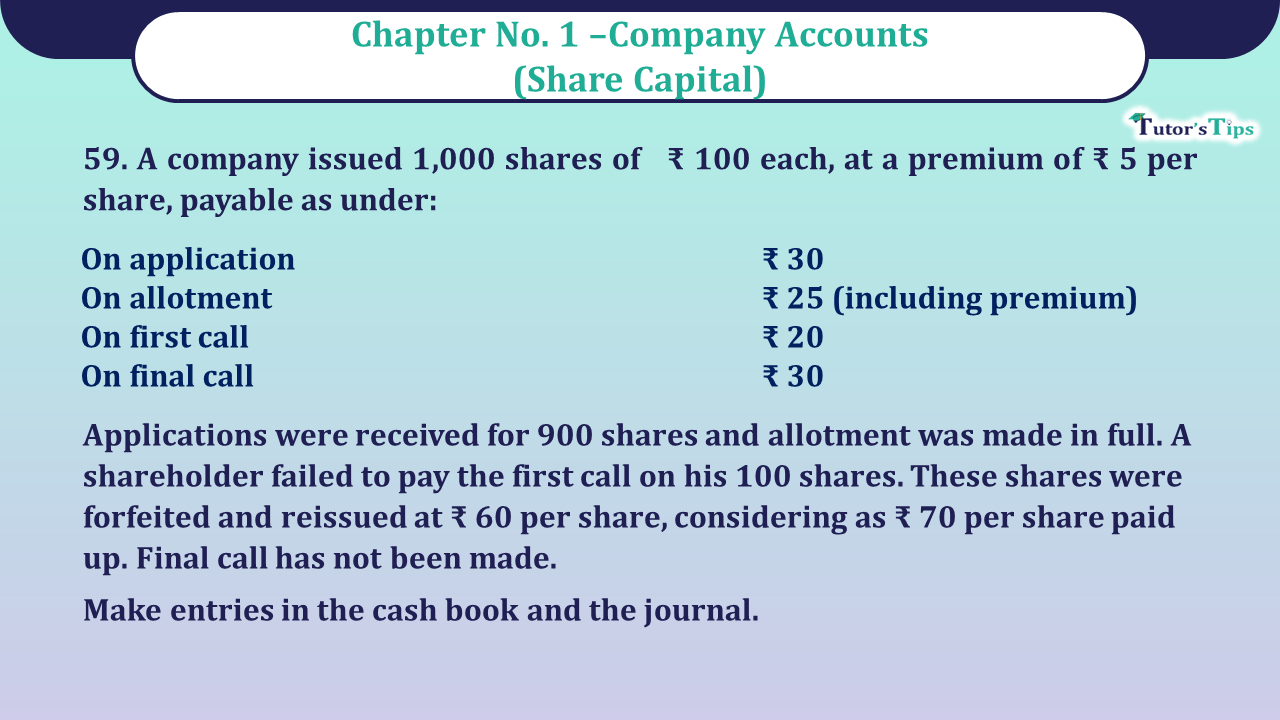

A company issued 1,000 shares of ₹ 100 each, at a premium of ₹ 5 per share, payable as under:

| On application | ₹ 30 |

| On allotment | ₹ 25 (including premium) |

| On first call | ₹ 20 |

| On final call | ₹ 30 |

Applications were received for 900 shares and allotment was made in full. A shareholder failed to pay the first call on his 100 shares. These shares were forfeited and reissued at ₹ 60 per share, considering as ₹ 70 per share paid up. Final call has not been made.

Make entries in the cash book and the journal.

The solution of Question 59 Chapter 1 of +2 Part-2: –

Cash book

|

Date |

Particulars | Amount | Date | Particulars | Amount |

| To share application A/c | 27,000 | By balance c/d | 71,500 | ||

| To share allotment A/c | 22,500 | ||||

| To share first call A/c | 16,000 | ||||

| To share capital A/c | 6,000 | ||||

| 71,500 | 71,500 |

Journal

Books of of Sakshi

| Date | Particulars |

L.F. | Debit | Credit | |

| Bank A/c | Dr. | 27,000 | |||

| To share application A/c | 27,000 | ||||

| (Being application money received on 900 share) | |||||

| Share application A/c | Dr. | 27,000 | |||

| To share capital A/c | 27,000 | ||||

| (Being application money transferred to share capital a/c) | |||||

| Shares allotment A/c | Dr. | 22,500 | |||

| To shares capital A/c | 18,000 | ||||

| To securities premium reserve A/c | 4,500 | ||||

| (Being allotment money due on 9,000 shares @ ₹ 25 per share including premium of ₹ 5 per share) | |||||

| Bank A/c | Dr. | 22,500 | |||

| To shares allotment A/c | 22,500 | ||||

| (Being allotment money received) | |||||

| Share first call A/c | Dr. | 18,000 | |||

| To shares capital A/c | 18,000 | ||||

| (Being first call money due on 900 shares @# ₹ 20 per share) | |||||

| Bank A/c | Dr. | 16,000 | |||

| Calls in arrears A/c | Dr. | 2000 | |||

| To share first call A/c | 18,000 | ||||

| (Being share first call money received on 100 shares) | |||||

| Share capital A/c | Dr. | 7,000 | |||

| To share first call A/c | 2,000 | ||||

| To share forfeited A/c | 5,000 | ||||

| (Being 100 shares forfeited due to non-payment of first call) | |||||

| Bank A/c | Dr. | 6,000 | |||

| Share forfeited A/c | Dr. | 1,000 | |||

| To share capital A/c | 7,000 | ||||

| (Being forfeited shares reissued at ₹ 60, considering ₹ 70 paid up) | |||||

| Share forfeited A/c | Dr. | 4,000 | |||

| To capital reserve A/c | 4,000 | ||||

| (Being the profit on 100 share forfeiture transferred to capital reserve A/c) | |||||

Working Note:

| Amount forfeited on 100 shares | = ₹ 5,000 |

| Less: Discount allowed on reissued share | = ₹ 1,000 |

| Balance credited to capital reserve A/c | = ₹ 400 |

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Share Capital: Meaning, Types, and Classes

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication