Question no 15 Chapter 1 V K Publication class 12

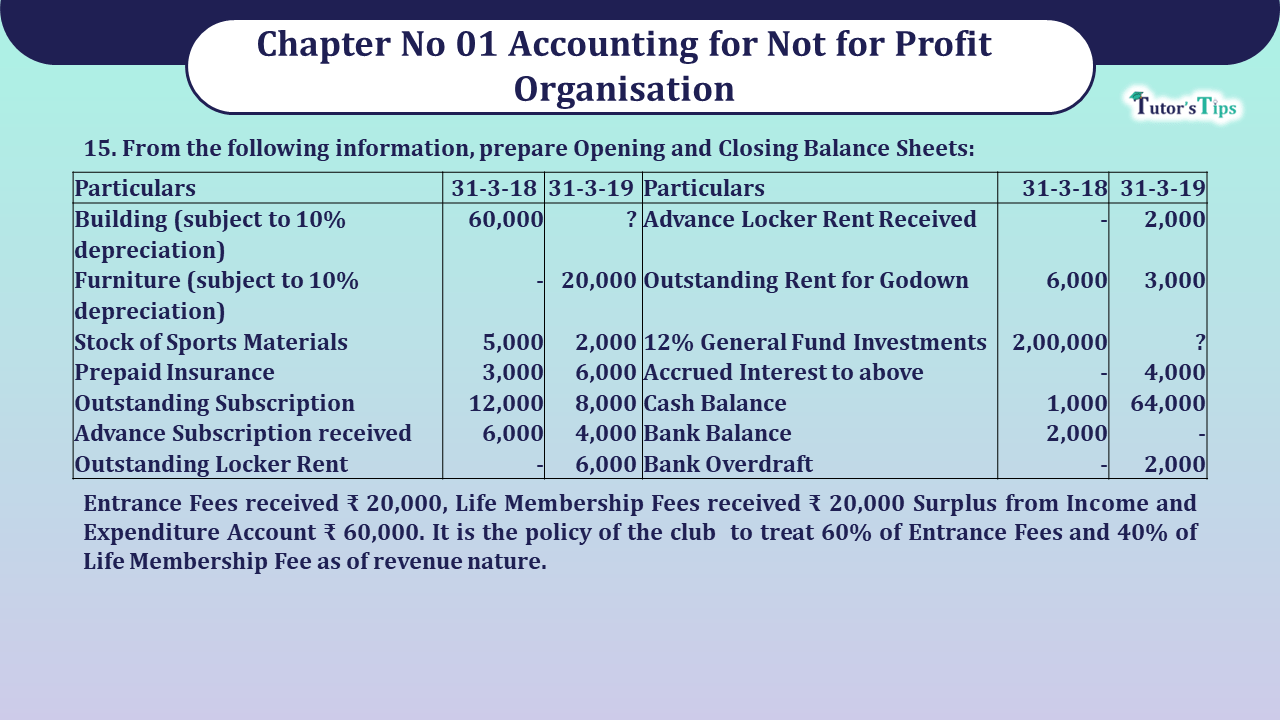

15. From the following information, prepare Opening and Closing Balance Sheets:

| Particulars | ₹ 2018 | ₹ 2019 | Particulars | ₹ 2018 | ₹ 2019 |

| Building (subject to 10% depreciation) | 60,000 | – | Subscription received in advance | – | 2,000 |

| Furniture (subject to 10% depreciation) | – | 20,000 | Outstanding Subscriptions | 6,000 | 3,000 |

| Stock of Sports Materials | 5,000 | 2,000 | Outstanding Expenses | 2,00,000 | – |

| Prepaid Insurance | 3,000 | 6,000 | – | 4,000 | |

| Outstanding Subscription | 12,000 | 8,000 | 1,000 | 64,000 | |

| Advance Subscription received | 6,000 | 4,000 | 2,000 | – | |

| Outstanding Locker Rent | – | 6,000 | – | 2,000 |

Entrance Fees received ₹ 20,000, Life Membership Fees received ₹ 20,000 Surplus from Income and Expenditure Account ₹ 60,000. It is the policy of the club to treat 60% of Entrance Fees and 40% of Life Membership Fee as of revenue nature.

The Solution of Question No 15 Chapter No 01 – V K Publications Class 12

| Opening Balance Sheet as at 31st March 2018 | |||||

| Liabilities | Amount | Assets | Amount | ||

| Subscriptions received in advance | 6,000 | Cash | 1,000 | ||

| Outstanding Rent for Godown | 6,000 | Bank | 2,000 | ||

| Capital Fund (Balancing figure) | 2,71,000 | General Fund Investments | 2,00,000 | ||

| Outstanding Subscriptions | 12,000 | ||||

| Sports Materials | 5,000 | ||||

| Building | 60,000 | ||||

| Prepaid Insurance | 3,000 | ||||

| 2,83,000 | 2,83,000 | ||||

| Closing Balance Sheet as at 31st March 2018 | |||||

| Liabilities | Amount | Assets | Amount | ||

| Subscriptions received in advance | 4,000 | Building | 60,000 | ||

| Outstanding Rent for Godown | 3,000 | Less: Depreciation 6,000 | 6,000 | 54,000 | |

| Bank overdraft | 2,000 | Furniture | 20,000 | ||

| Life membership fees (20,000-8,000) | 12,000 | Less: Depreciation | 2,000 | 18,000 | |

| Entrance fees (20,000- 12,000) | 8,000 | Stock of Sports Material | 2,000 | ||

| Capital Fund | 2,71,000 | Prepaid Insurance | 6,000 | ||

| Add: Surplus | 60,000 | 3,31,000 | Outstanding Subscriptions | 8,000 | |

| Advance Locker Rent Received | 2,000 | General Fund Investment (with accrued lnterest) (2,00,000+4,000) | 2,04,000 | ||

| Cash Balance | 64,000 | ||||

| Outstanding Locker Rent | 6,000 | ||||

| 2,83,000 | 2,83,000 | ||||

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Not-for-Profit Organisations – Meaning and Overview

What is Receipt and Payment account – format in Excel & PDF

What is Incomes and Expenditures Account – format in Excel & PDF

What is subscription in NPO – Treatments and Examples:

Also, Check out the solved question of all Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST): An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Computers and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software: Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)

Check out V. K. Publication Class 12 @ Oficial Website of V. K. Publication