Question 8 Chapter 2 – Unimax Class 12 Part 1

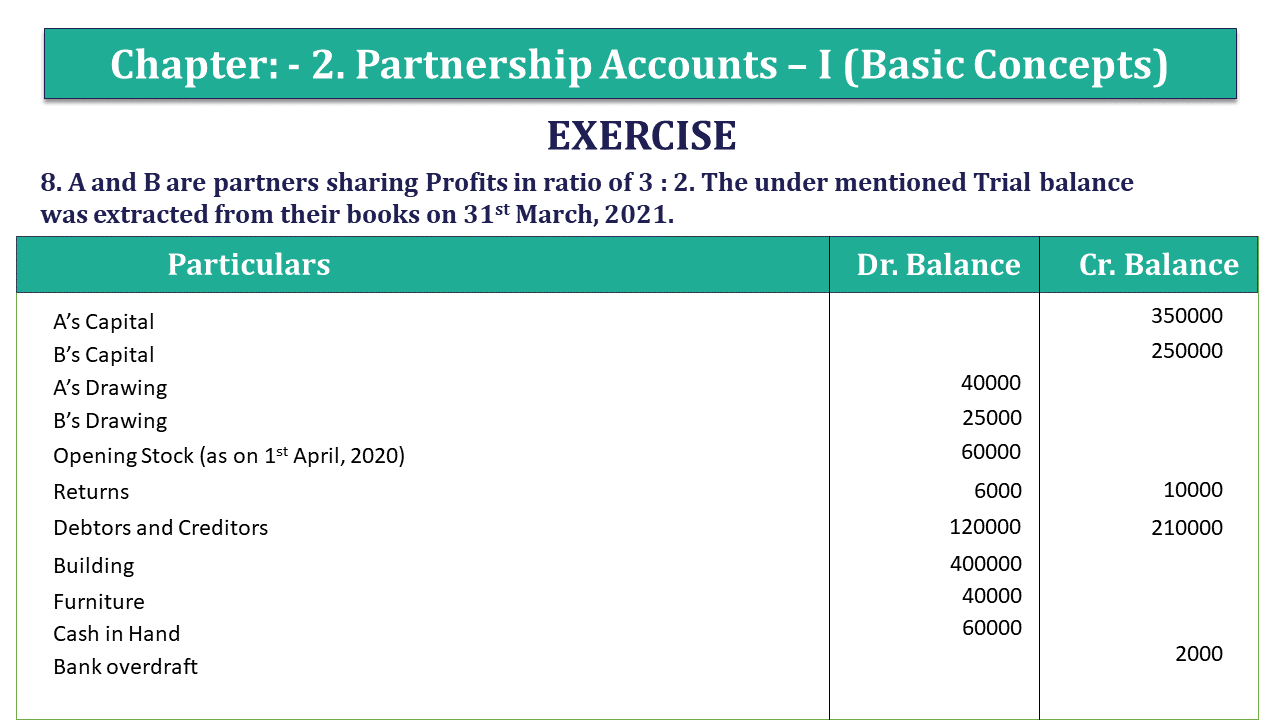

8. A and B are partners sharing Profits in ratio of 3 : 2. The under mentioned Trial balance was extracted from their books on 31st March, 2021.

| Particulars | Dr. Balance | Cr. Balance |

| A’s Capital | 350000 | |

| B’s Capital | 250000 | |

| A’s Drawing | 40000 | |

| B’s Drawing | 25000 | |

| Opening Stock (as on 1st April, 2020) | 60000 | |

| Returns | 6000 | 10000 |

| Debtors and Creditors | 120000 | 210000 |

| Building | 400000 | |

| Furniture | 40000 | |

| Cash in Hand | 60000 | |

| Bank overdraft | 2000 | |

| 64000 | ||

| Rent | 24000 | |

| Advertising expenditure | 13000 | |

| Travelling expenses | 15000 | |

| Telephone Charges | 17000 | |

| Carriage Inwards | 23700 | |

| Carriage Outwards | 14300 | |

| Commission | 20000 | |

| Bills Receivable | 20000 | |

| Motor Van | 100000 | |

| Purchases and Sales | 1000000 | 1200000 |

| 2042000 | 2042000 |

You are required to prepare the Profit and Loss Account and Profit and Loss Appropriation Account for the year ended 31st March, 2021 and a Balance Sheet as on that date. The following adjustments are to be made :

(i) The value of stock on 31st March, 2021 was Rs. 82000.

(ii) Create a provision of 5% on debtors for doubtful debts.

(iii) Charge depreciation on Furniture at 15%, on Building at 2% and on Motor Van at 5%.

(iv) Provide for outstanding rent Rs. 2400 and outstanding telephone bill Rs. 2800.

(v) Partners are entitled to interest on Capital @ 5% per annum.

The solution of Question 8 Chapter 2 – Unimax Class 12 Part 1:

Trading And Profit & Loss Account For the year ended March. 31, 2006.

| Particulars | Rs. | Particulars | Rs. | ||

| To Opening Stock | 60000 | By Sale | 1200000 | ||

| To Purchases | 100000 | Less Return | 6000 | 1194000 | |

| Less Returns | 10000 | 990000 | By Closing Stock | 82000 | |

| To Carriage inward | 23700 | ||||

| To Gross Profit c/d | 202300 | ||||

| 1276000 | 1276000 | ||||

| To Depreciation | By Gross Profit b/d | 202300 | |||

| – Furniture | 6000 | By Commission | 20000 | ||

| – Building | 8000 | ||||

| – Motor Van | 5000 | 19000 | |||

| To Provision for bad debts | 6000 | ||||

| To Rent | 24000 | ||||

| Add Outstanding | 2400 | 26400 | |||

| To Telephone Bills | 17000 | ||||

| Add Outstanding | 2800 | 19800 | |||

| To Salary | 64000 | ||||

| To Advertisement | 13000 | ||||

| To Travelling expense | 15000 | ||||

| To Carriage Outward | 14300 | ||||

| To Net Profit | |||||

| – A | 26880 | ||||

| – B | 17920 | 44800 | |||

| 222300 | 222300 |

Profit & Loss Appropriation Account For the year ended March. 31, 2006.

| Particulars | Rs. | Particulars | Rs. | |

| To Interest on Capital | By Net Profit | 44800 | ||

| – A | 17500 | |||

| – B | 12500 | 30000 | ||

| To Share of Profit | ||||

| – A (3/5) | 8880 | |||

| – B (2/5) | 5920 | 14800 | ||

| 44800 | 44800 |

Balance Shee As on 31.3.2006

| Liabilities | Amount | Assets | Amount | ||

| Creditors | 210000 | Building | 400000 | ||

| Bank Overdraft | 2000 | Less Dep. | 8000 | 392,000 | |

| Outstanding Rent | 2400 | Furniture | 40,000 | ||

| Outstanding Bills | 2800 | Less Dep. | 6,000 | 34000 | |

| A’s Capital | 3,50000 | Motor Van | 100000 | ||

| Add Interest | 17500 | Less: Depreciation | 5000 | 95000 | |

| Add Net Profit | 8880 | Cash in hand | 60000 | ||

| Less Drawings | 40,000 | 336380 | Bills receivable | 20000 | |

| B’s Capital | 250000 | Debtors | 120000 | ||

| Add Interest | 12500 | Less Provision | 6000 | 114000 | |

| Add Net Profit | 5920 | Stock | 82000 | ||

| Less Drawings | 25000 | 243420 | |||

| 797000 | 797000 |

https://tutorstips.com/not-for-profit-organisations/

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication