Question 7 Chapter 2 – Unimax Class 12 Part 1

Table of Contents

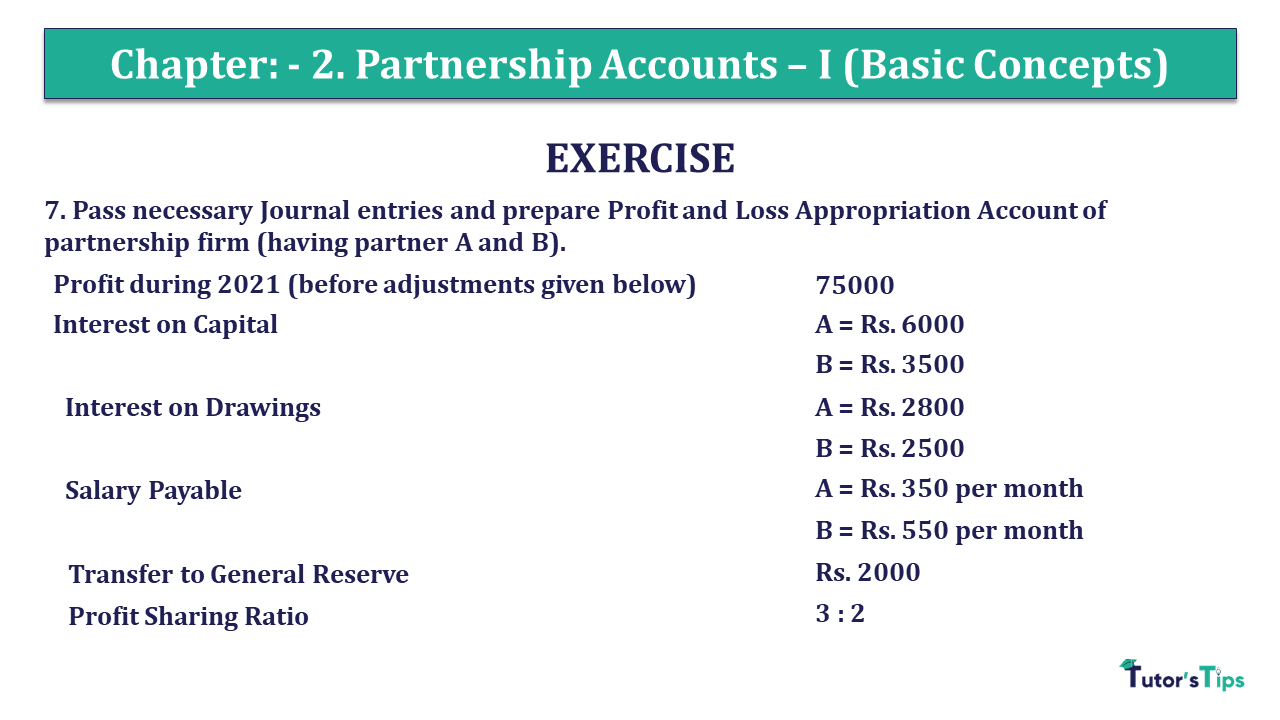

7. Pass necessary Journal entries and prepare Profit and Loss Appropriation Account of partnership firm (having partner A and B).

| Profit during 2021 (before adjustments given below) | 75000 |

| Interest on Capital | A = Rs. 6000 |

| B = Rs. 3500 | |

| Interest on Drawings | A = Rs. 2800 |

| B = Rs. 2500 | |

| Salary Payable | A = Rs. 350 per month |

| B = Rs. 550 per month | |

| Transfer to General Reserve | Rs. 2000 |

| Profit Sharing Ratio |

3 : 2 |

The solution of Question 7 Chapter 2 – Unimax Class 12 Part 1:

Journal Enteries

| Date | Particulars | L.F. | Debit | Credit | |

| Profit and Loss A/c | Dr. | 75,000 | |||

| To Profit and Loss Appropriation A/c | 75,000 | ||||

| (Being balance of net profit transferred to profit and loss appropriation A/c) | |||||

| Interest on capital A/c | Dr. | ||||

| To A’s Capital A/c | 6,000 | ||||

| To B’s Capital A/c | 3,500 | ||||

| (Being interest on capital provided to partners A &B ) | |||||

| Profit and Loss Appropriation A/c | Dr. | 9,500 | |||

| To Interest on capital A/c | 9,500 | ||||

| (Being transfer of interest on capital to Profit and Loss Appropriation A/c) | |||||

| A’s capital A/c | Dr. | 2,800 | |||

| B’s capital A/c | Dr. | 2,500 | |||

| To Interest on Drawings A/c | 5,300 | ||||

| (Being interest charged on partners’s drawings) |

Journal Enteries

| Date | Particulars | L.F. | Debit | Credit | |

| Interest on Drawings A/c | Dr. | 5,300 | |||

| To Profit and Loss Appropriation A/c | 5,300 | ||||

| (Being transfer of interest on drawings to profit and loss appropriation A/c) | |||||

| Salary A/c | Dr. | 10800 | |||

| To A’s Capital A/c | 4200 | ||||

| To B’s Capital A/c | 6600 | ||||

| (Being Salary provided to partners A & B) | |||||

| Profit and Loss Appropriation A/c | Dr. | 10800 | |||

| To Salary A/c | 10800 | ||||

| (Being transfer out of profit to general reserve) | |||||

| Profit and Loss Appropriation A/c | Dr. | 58000 | |||

| To A’s Capital A/c | 34800 | ||||

| To B’s Capital A/c | 23200 | ||||

| (Being distribution of profit among partners A & B in 3:2) |

https://tutorstips.com/not-for-profit-organisations/

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication