Question 54 Chapter 1 of +2-A

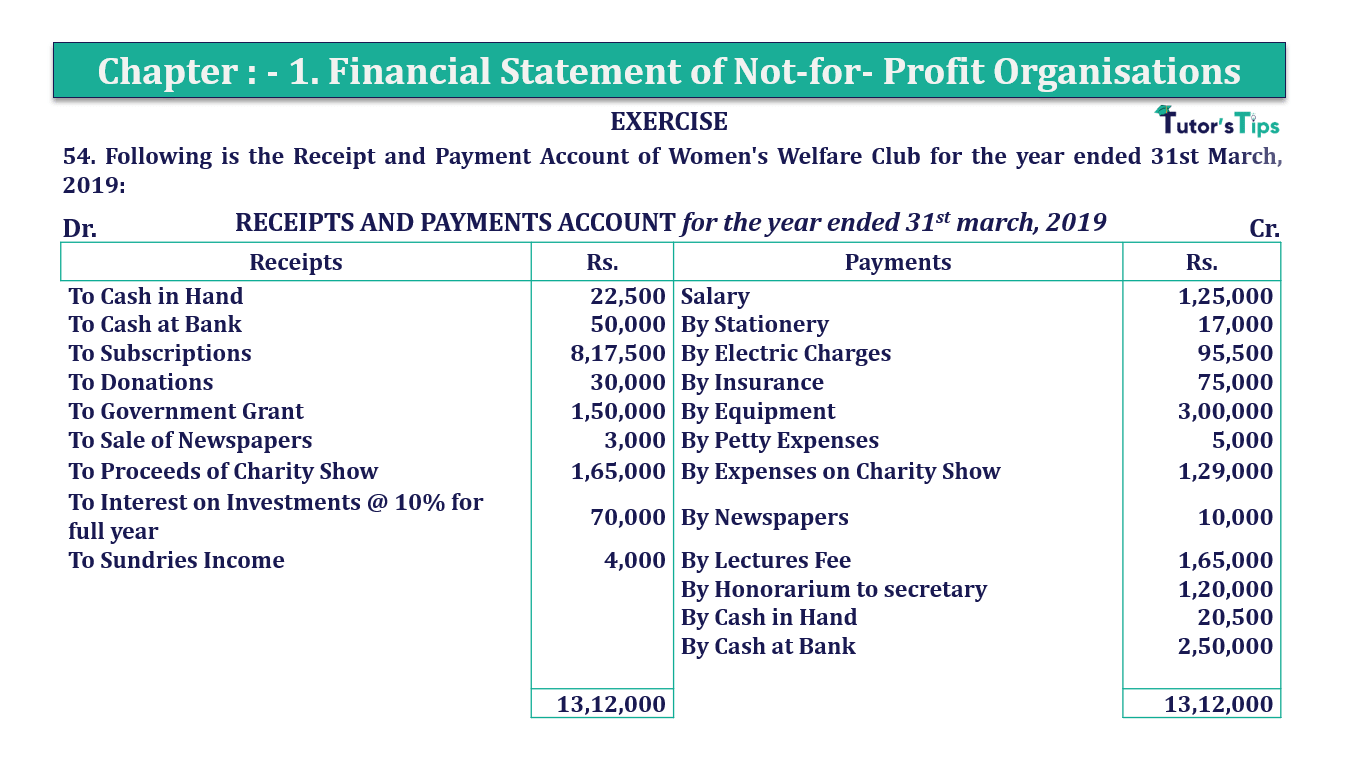

54. Following is the Receipt and Payment Account of Women’s Welfare Club for the year ended 31st March 2019:

| RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March 2019 | |||

| Receipts | Rs. | Payments | Rs. |

| To Cash in Hand | 22,500 | Salary | 1,25,000 |

| To Cash at Bank | 50,000 | By Stationery | 17,000 |

| To Subscriptions | 8,17,500 | By Electric Charges | 95,500 |

| To Donations | 30,000 | By Insurance | 75,000 |

| To Government Grant | 1,50,000 | By Equipment | 3,00,000 |

| To Sale of Newspapers | 3,000 | By Petty Expenses | 5,000 |

| To Proceeds of Charity Show | 1,65,000 | By Expenses on Charity Show | 1,29,000 |

| To Interest on Investments @ 10% for full-year | 70,000 | By Newspapers | 10,000 |

| To Sundries Income | 4,000 | By Lectures Fee | 1,65,000 |

| By Honorarium to the secretary | 1,20,000 | ||

| By Cash in Hand | 20,500 | ||

| By Cash at Bank | 2,50,000 | ||

| 13,12,000 | 13,12,000 | ||

Additional Information:

| Particulars | 1st April 2018 | 31st March 2019 |

| (₹) | (₹) | |

| Outstanding Salaries | 12,000 | 18,000 |

| Insurance Prepaid | 7,000 | 3,000 |

| Subscription Outstanding | 37,500 | 25,000 |

| Subscription received in advance | 17,500 | 10,000 |

| Electricity Charges outstanding | … | 12,500 |

| Stock of Stationery | 22,500 | 7,000 |

| Equipment | 2,56,000 | 5,02,000 |

| Building | 12,00,000 | 11,40,000 |

Prepare Income and Expenditure Account for the year ended 31st March, 2019,and Balance Sheet as on that date.

The solution of Question 54 Chapter 1 of +2-A:

| Books of Rama Krishna Mission Charitable Hospital Income and Expenditure Account (for the year ended 31st March 2019) |

||||||

| Expenditure |

Amount | Income |

Amount | |||

| To Stationery | 32,500 | By Subscriptions *1 | 8,17,500 | |||

| To Electricity Charges | 95,500 | Add: O/s at the end | 25,000 | |||

| Add: O/s at the end | 12,500 | 1,08,000 | Adv. in the Beginning | 17,500 | ||

| To Salary | 1,25,000 | Less: O/s in the Beginning | 37,500 | |||

| Add: O/s at the end | 18,000 | Adv. at the end | 10,000 | 8,12,500 | ||

| Less: O/s Beginning | 12,000 | 1,31,000 | By Donations | 30,000 | ||

| To Insurance | 75,000 | By Government Grant | 1,50,000 | |||

| Add: O/s at the end | 7,000 | By Sale of Old Newspapers | 3,000 | |||

| Less: O/s Beginning | 3,000 | 79,000 | By Income from Charity Show | |||

| To Petty Expenses | 5,000 | Proceeds of Charity Show | 1,65,000 | |||

| To Newspaper | 10,000 | Less: O/s in the Beginning | 1,29,000 | 36,000 | ||

| To Lectures Fees | 1,65,000 | By Interest on Investments | 70,000 | |||

| To Honorarium to Secretary | 1,20,000 | By Sundries Income | 4,000 | |||

| To Depreciation on Equipment *2 | 54,000 | |||||

| To Depreciation on Building*3 | 60,000 | |||||

| By Deficit (Balancing Figure) | 3,41,000 | |||||

| 7,99,500 | 7,99,500 | |||||

* Means: – see the working note for calculation

| Balance Sheet (for the year ended 31st March 2018) |

||||

| Liabilities |

Amount | Assets |

Amount | |

| Outstanding Salary | 12,000 | Prepaid Insurance | 7,000 | |

| Subscription Received in Advance | 17,500 | Subscription Outstanding | 37,500 | |

| Stock of Stationery | 22,500 | |||

| Equipment | 2,56,000 | |||

| Building | 12,00,000 | |||

| Capital Fund (Balancing Figure) | 22,66,000 | Cash |

22,500 |

|

| Bank | 50,000 | |||

| 10% Investments *4 | 7,00,000 | |||

| 22,95,500 | 22,95,500 | |||

| Balance Sheet (for the year ended 31st March 2019) |

||||||

| Liabilities |

Amount | Assets |

Amount | |||

| Capital Fund | 22,66,000 | 1,000 | Prepaid Insurance | 3,000 | ||

| Add: Surplus | 3,41,000 | 26,07,000 | Subscription Outstanding | 25,000 | ||

| Outstanding Salary | 18,000 | Stock of Stationery | 7,000 | |||

| Subscription Received in Advance | 10,000 | Equipment | 2,56,000 | |||

| Electricity Charges Outstanding | 12,500 | Add: Purchases | 3,00,000 | 3,16,000 | ||

| Less: Depreciation *2 | 54,000 | 5,02,000 | ||||

| Building | 12,00,000 | |||||

| Less: Depreciation *3 | 60,000 | 11,40,000 | ||||

| Cash | 20,500 | |||||

| Bank | 2,50,000 | |||||

| 10% Investments *1 | 7,00,000 | |||||

| 26,47,500 | 26,47,500 | |||||

* Means: – see the working note for calculation

Working Note: –

*1:- Calculation of Amount of Subscriptions

| Subscription received During the year | 8,17,500 |

| Add: – Subscription outstanding at the end of the year | 25,000 |

| Subscription received in advance in the beginning of the year | 17,500 |

| 8,60,000 | |

| Less: – Subscription outstanding in the beginning of the year | 37,500 |

| Subscription received in advance at the end of the year | 10,000 |

| The amount for subscription credited to the Income and Expenditure A/c | 8,12,500 |

*2:- Calculate Depreciation on Equipment

Depreciation = Opening Balance of Equipment + Equipment Purchased During the year – Closing Balance of Equipment

Opening Balance of Equipment = 2,56,000

Closing Balance of Equipment = 5,02,000

Equipment Purchased During the year = 3,00,000

= 2,56,000 + 3,00,000 – 5,02,000

Depreciation = 54,000

*3:- Calculate Depreciation on Building

Depreciation = Opening Balance of Building + Building Purchased During the year – Closing Balance of Building

Opening Balance of Building = 12,00,000

Closing Balance of Building = 11,40,000

Building Purchased During the year = 0

= 12,00,000 + 0 – 11,40,000

Depreciation = 60,000

*4:- Calculation of the amount of Investment X

| = amount of Interest | X | 100 |

| Rate of Interest |

| 70,000 | X | 100 |

| 10 |

Total on Investment = 7,00,000/-

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: –

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication