Question 48 Chapter 8 – Unimax Publication Class 12 Part 2 – 2021

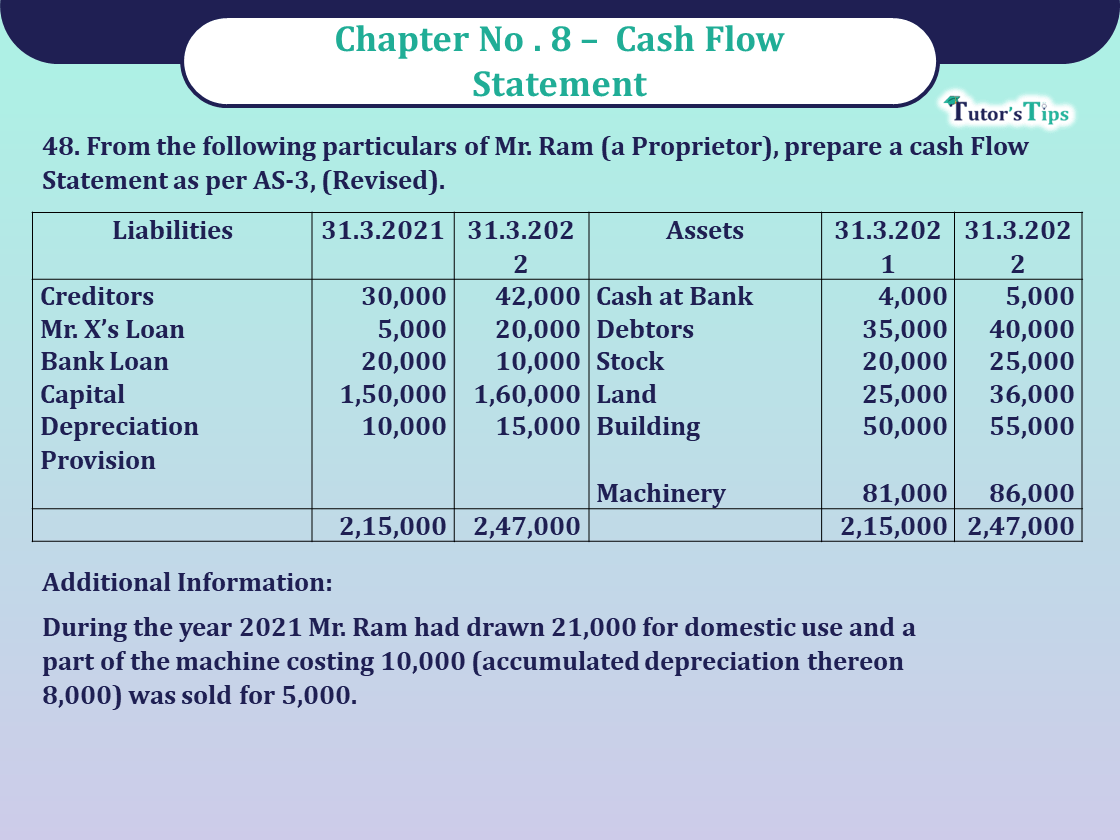

48. From the following particulars of Mr. Ram (a Proprietor), prepare a cash Flow Statement as per AS-3, (Revised).

BALANCE SHEETS

| Liabilities | 31.3.2021 | 31.3.2022 | Assets | 31.3.2022 | 31.3.2022 |

| Creditors | 30,000 | 42,000 | Cash at Bank | 4,000 | 5,000 |

| Mr. X’s Loan | 5,000 | 20,000 | Debtors | 35,000 | 40,000 |

| Bank Loan | 20,000 | 10,000 | Stock | 20,000 | 25,000 |

| Capital | 1,50,000 | 1,60,000 | Land | 25,000 | 36,000 |

| Depreciation Provision | 10,000 | 15,000 | Building | 50,000 | 55,000 |

| Machinery | 81,000 | 86,000 | |||

| 2,15,000 | 2,47,000 | 2,15,000 | 2,47,000 |

Additional Information:

During the year 2021 Mr. Ram had drawn 21,000 for domestic use and a part of the machine costing 10,000 (accumulated depreciation thereon 8,000) was sold for 5,000.

The solution of Question 48 Chapter 8 – Unimax Publication Class 12 Part 2-2021 : –

CASH FLOW STATEMENT (INDIRECT METHOD)

FOR THE YEAR ENDED 31.3.2022(AS-3(REVISED)

| Particulars | ₹ | ₹ | |

| (A)cash flow from operating activities | |||

| Net Profit before tax and extraordinary items | 31,000 | ||

| Adjustment for: | |||

| Depreciation on Machine | 13,000 | ||

| Gain on Sale of Machine | (3,000) | ||

| Operating profit before working Capital changes | 41,000 | ||

| Add: Increase in Current Liabilities: | |||

| Creditors | 12,000 | ||

| 53,000 | |||

| Less: Increase in Current Assets: | |||

| Debtors | ₹ 5,000 | ||

| Stock | ₹ 5,000 | (10,000) | |

| Net Cash from Operating Activities | 43,000 | 43,000 | |

| B. Cash Flow from investing Activities | |||

| Purchase of Land | (11,000) | ||

| Purchase of Machinery | (15,000) | ||

| Purchase of Building | (5,000) | ||

| Sale of Machine | 5,000 | ||

| Net Cash used in investing Activities | (26,000) | (26,000) | |

| C. Cash Flow from Financing Activities: | |||

| Funds from Raising Loan from Mr. X | 15,000 | ||

| Repayment of Bank Loan | (10,000) | ||

| Drawings of X | (21,000) | ||

| Net Cash used in Financing Activities | (16,000) | (16,000) | |

| Net Increase in cash and cash equivalents | 1,000 | ||

| Cash and cash equivalents at the beginning of the period | 4,000 | ||

| Cash and cash equivalents at the End of the period | 5,000 | ||

Working Notes:

CAPITAL ACCCOUNT

| Particulars | ₹ | Particulars | ₹ |

| To Bank A/c | 21,000 | By Balance c/d | 1,50,000 |

| To Balance C/d | 1,60,000 | By Profit and Loss, A/c | 31,000 |

| 1,81,000 | 1,81,000 | ||

| By Balance b/d | 1,60,000 |

MACHINERY ACCCOUNT

| Particulars | ₹ | Particulars | ₹ |

| To Balance b/d | 81,000 | By Provision for Depreciation A/c | 8,000 |

| To Gain on Sale of Machinery | 3,000 | By Bank A/c (Sale) | 5,000 |

| To Bank A/c (b/f) (Purchase) | 15,000 | By Balance c/d | 86,000 |

| 99,000 | 99,000 |

PROVISION FOR DEPRECIATION ACCCOUNT

| Particulars | ₹ | Particulars | ₹ |

| To Machinery A/c | 8,000 | By Depreciation b/d | 10,000 |

| Bank Balance c/d | 15,000 | By Depreciation A/c | 13,000 |

| (Depreciation during the year) | |||

| 23,000 | 23,000 | ||

| By Balance b/d | 15,000 |

Alternatively, Machinery Account and Machinery Sold Account can be Clubbed Together.

MACHINERY ACCCOUNT

| Particulars | ₹ | Particulars | ₹ |

| To Balance b/d | 81,000 | By Machinery Sold A/c | 10,000 |

| To Bank A/c (Purchase) | 15,000 | By Balance c/d | 86,000 |

| 96,000 | 96,000 | ||

| To Balance b/d | 86,000 |

PROVISION FOR DEPRECIATION ACCCOUNT

| Particulars | ₹ | Particulars | ₹ |

| To Machinery A/c | 8,000 | By Balance b/d | 10,000 |

| Bank Balance c/d | 15,000 | By Depreciation A/c | 13,000 |

| (Depreciation during the year) | |||

| 23,000 | 23,000 | ||

| By Balance b/d | 15,000 |

MACHINERY ACCCOUNT

| Particulars | ₹ | Particulars | ₹ |

| To Machinery A/c | 10,000 | By Provision for Depreciation A/c | 8,000 |

| To Gain on Sale of Machinery | 3,000 | By Bank A/c | 5,000 |

| 13,000 | 13,000 |

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

What is the cash flow statement? why do we need to prepare?

Unimax Publication – Accountancy PSEB Class 12 – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Change in Profit sharing ratio among Existing Partners )

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Unimax Publication – Accountancy PSEB (Class 12) – Part – II – Solution

- Chapter No. 1 – Company Accounts (Share Capital)

- Chapter No. 2 – Company Accounts (Issue of Debentures)

- Chapter No. 3 – Company Accounts (Redemption of Debentures)

- Chapter No. 4 – Financial Statements of a Company

- Chapter No. 5 – Financial Statement Analysis

- Chapter No. 6 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 7 – Ratio Analysis

- Chapter No. 8 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2023@ Official Website of Sultan Chand Publication