Question 44 Chapter 8 – Unimax Publication Class 12 Part 2 – 2021

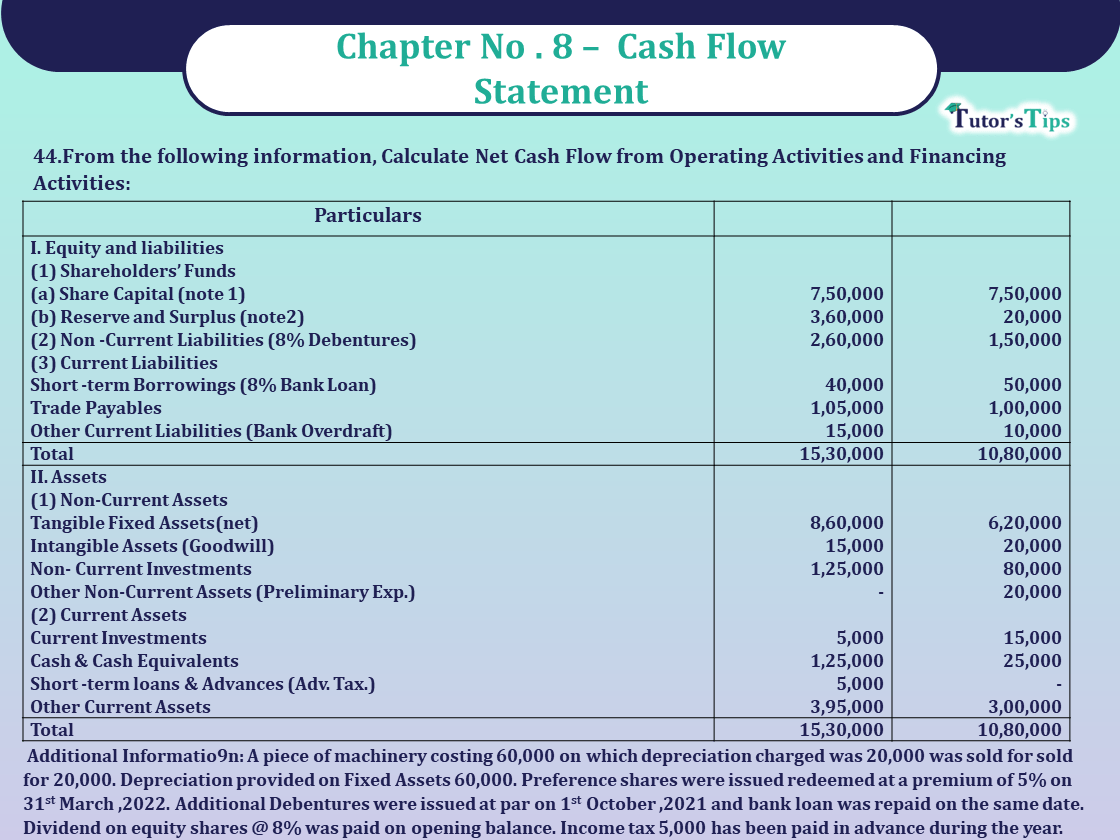

44.From the following information, Calculate Net Cash Flow from Operating Activities and Financing Activities:

BALANCE SHEETS AS AT…….

| Particulars | 31.3.2022 | 31.3.2021 |

| I. Equity and liabilities | ||

| (1) Shareholders’ funds | ||

| (a)Share Capital (Note1) | 7,50,000 | 7,50,000 |

| (b)Reserves and surplus (note2) | 3,60,000 | 20,000 |

| (2) Non- Current Liabilities (18% Debentures) | 2,60,000 | 1,50,000 |

| (3) Current Liabilities | ||

| Short -term Borrowings (8% Bank Loan) | 40,000 | 50,000 |

| Trade Payables | 1,05,000 | 1,00,000 |

| Other Current Liabilities (Bank Overdraft) | 15,000 | 10,000 |

| Total | 15,30,000 | 10,80,000 |

| B. Assets | ||

| (1) Non-Current Assets | ||

| Tangible Fixed Assets (Net) | 8,60,000 | 6,20,000 |

| Intangible Assets (Goodwill) | 15,000 | 20,000 |

| Non- Current Investments | 1,25,000 | 80,000 |

| Non- Current Investments | – | 20,000 |

| (2) Current Assets | ||

| Current Investments | 5,000 | 15,000 |

| Cash & Cash Equivalents | 1,25,000 | 25,000 |

| Short -term loans & Advances (Adv. Tax.) | 5,000 | – |

| Other Current Assets | 3,95,000 | 3,00,000 |

| Total | 15,30,000 | 10,80,000 |

NOTE 1: SHARE CAPITAL

| Particulars | 31.3.2022 ₹ | 31.3.2021 ₹ |

| Equity Share Capital | 5,50,000 | 4,50,000 |

| 5% Pref. Share Capital | 2,00,000 | 3,00,000 |

| 7,50,000 | 7,50,000 |

NOTE 2: RESERVES AND SURPLUS

| Particulars | 31.3.2022 ₹ | 31.3.2021 ₹ |

| General Reserve | 1,50,000 | 1,20,000 |

| Profit and Loss A/c | 2,00,000 | (1,00,000) |

| Securities premium | 10,000 | – |

| 1,70,000 | 20,000 |

Additional Information: A piece of machinery costing 60,000 on which depreciation charged was 20,000 was sold for sold for 20,000. Depreciation provided on Fixed Assets 60,000. Preference shares were issued redeemed at a premium of 5% on 31st March ,2022. Additional Debentures were issued at par on 1st October ,2021 and bank loan was repaid on the same date. Dividend on equity shares @ 8% was paid on opening balance. Income tax 5,000 has been paid in advance during the year.

The solution of Question 44 Chapter 8 – Unimax Publication Class 12 Part 2-2021 : –

CASH FLOW STATEMENT

FOR THE YEAR ENDED 31st MARCH . 2022

| Particulars | ₹ | ₹ |

| I. cash flow from operating activities | ||

| Net profit before tax | 3,81,000 | |

| Adjustment for Non-Cash and Non-Operating Activities | ||

| Dep. on Fixed Assets | 60,000 | |

| Loss on sale of machinery | 20,000 | |

| Interest on Debentures | ||

| (1,50,000 x 8/100) +(1,10,000 x 8/100 x 6/12) | 16,400 | |

| Interest on Bank Loan | ||

| (50,000 x 8/100 x 6/12) +(40,000 x 8/100 x 6/12) | 3,600 | |

| Goodwill Amort | 5,000 | |

| Preliminary Exp. written off | 20,000 | |

| Premium on Redemption of Preference Shares | 5,000 | 1,30,000 |

| Operating Profit before Working Capital Changes | 5,11,000 | |

| Change in CA &CL | ||

| Increase in other CA | (95,000) | |

| Increase in CL | 5,000 | (90,000) |

| Net Cashflow from Op. Activities before Tax | 4,21,000 | |

| Less Tx Paid | (5,000) | |

| Net Cashflow from Op. Activities after Tax | 4,16,000 | |

| II. Cash Flow from Investing Activities: | ||

| Sale | 20,000 | |

| Purchase | (3,40,000) | (3,65,000) |

| Investment Purchase | (45,000) | |

| III. Cash Flow from Financing Activities: | ||

| Issue of Share Capital (1,00,000+10,000) | 1,10,000 | |

| Issue of Debentures | 1,10,000 | |

| Interest on Debentures | (16,400) | |

| Interest on Bank Loan | (3,600) | |

| Dividend on Equity Shares | (36,000) | |

| Dividend on Preference Shares | (15,000) | |

| Redemption of Preference Shares (1,00,000+5,000) | (1,05,000) | |

| Bank Loan Repaid | (5,000) | |

| Net Cash used from Financing Activities | (39,000) |

Working Notes: (1)

| 1.Calculation of net profit before tax | ₹ |

| Closing Balance of profit &loss A/c | 2,00,000 |

| Add: Opening Balance of P&L A/c (Dr.) | 1,00,000 |

| Add: Transfer to Reserves | 30,000 |

| Add: Dividend on Equity Shares | 36,000 |

| Add: Dividend on Pref. Shares | 15,000 |

| Net profit before tax | 3,81,000 |

Working Notes: (2)

2. FIXED ASSETS ACCCOUNT

| Particulars | ₹ | Particulars | ₹ |

| TO Balance b/d | 6,20,000 | By Dep A/c | 60,000 |

| To Bank A/c (Purchase) (b. f) | By Bank A/c Sales | 20,000 | |

| (Purchased B. fig) | 3,40,000 | By P& L A/c Loss | 20,000 |

| By Balance c/d | 8,60,000 | ||

| 9,60,000 | 9,60,000 |

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

What is the cash flow statement? why do we need to prepare?

Unimax Publication – Accountancy PSEB Class 12 – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Change in Profit sharing ratio among Existing Partners )

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Unimax Publication – Accountancy PSEB (Class 12) – Part – II – Solution

- Chapter No. 1 – Company Accounts (Share Capital)

- Chapter No. 2 – Company Accounts (Issue of Debentures)

- Chapter No. 3 – Company Accounts (Redemption of Debentures)

- Chapter No. 4 – Financial Statements of a Company

- Chapter No. 5 – Financial Statement Analysis

- Chapter No. 6 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 7 – Ratio Analysis

- Chapter No. 8 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2023@ Official Website of Sultan Chand Publication