Question 43 Chapter 7 of +2-A

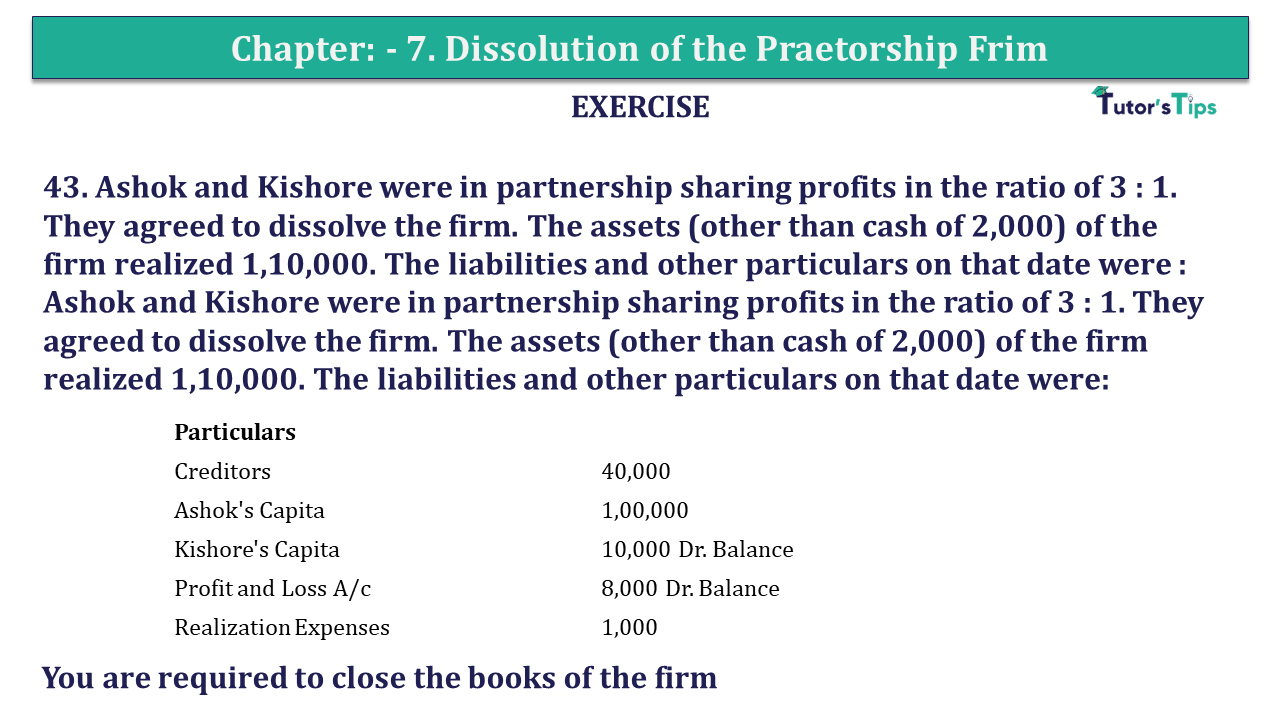

43. Ashok and Kishore were in partnership sharing profits in the ratio of 3: 1. They agreed to dissolve the firm. The assets (other than cash of 2,000) of the firm realized 1,10,000. The liabilities and other particulars on that date were: Ashok and Kishore were in partnership sharing profits in the ratio of 3: 1. They agreed to dissolve the firm. The assets (other than cash of 2,000) of the firm realized 1,10,000. The liabilities and other particulars on that date were:

| Particulars | |

| Creditors | 40,000 |

| Ashok’s Capita | 1,00,000 |

| Kishore’s Capita | 10,000 Dr Balance |

| Profit and Loss A/c | 8,000 Dr Balance |

| Realization Expenses | 1,000 |

You are required to close the books of the firm

The solution of Question 43 Chapter 7 of +2-A: –

| Realization Account |

|||||

| Particular 5 |

Amount | Particular | Amount | ||

| Sundry Assets (WN) | 1,20,000 | Creditors | 40,000 | ||

| Cash A/c Assets Realized | 1,10,000 | ||||

| Cash A/c: | |||||

| Creditors | 40,000 | ||||

| Expenses | 1,000 | 41,000 | |||

| Loss transferred to: | |||||

| Ashok’s Capital A/c | 8,250 | ||||

| Kishore’s Capital A/c | 2,750 | 11,000 | |||

| 1,61,000 | 1,61,000 | ||||

| Partners’ Capital Account |

|||||

| Part. | Ashok | Kishore |

Part. |

Ashok | Kishore |

| By Balance b/d | 10,000 | By Balance B/d | 1,00,000 | – | |

| By Realization A/c Loss | 8,250 | 2,750 | |||

| By Profit and Loss A/c | 6,000 | 2,000 | |||

| To Cash A/c | 85,750 | – | By Cash A/c | – | 14,750 |

| 1,00,000 | 14,750 | 1,00,000 | 14,750 | ||

| Cash Account |

|||||

| Particular |

Amount | Particular | Amount | ||

| Balance b/d | 2,000 | Realization A/c | 41,000 | ||

| Realization A/c | 1,10,000 | Ashok’s Capital A/c | 85,750 | ||

| Kishore’s Capital A/c | 14,750 | ||||

| 1,26,750 | 1,26,750 | ||||

Working Note:

| Memorandum Balance Sheet |

|||||

| Particular |

Amount | Particular | Amount | ||

| Creditors | 40,000 | Cash | 2,000 | ||

| Ashok’s Capita | 1,00,000 | Kishore’s Capital | 10,000 | ||

| Profit and Loss A/c | 8,000 | ||||

| Sundry Assets (Balancing figure) | 1,20,000 | ||||

| 1,40,000 | 1,40,000 | ||||

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication