Question 43 Chapter 5 – Unimax Class 12 Part 1 – 2021

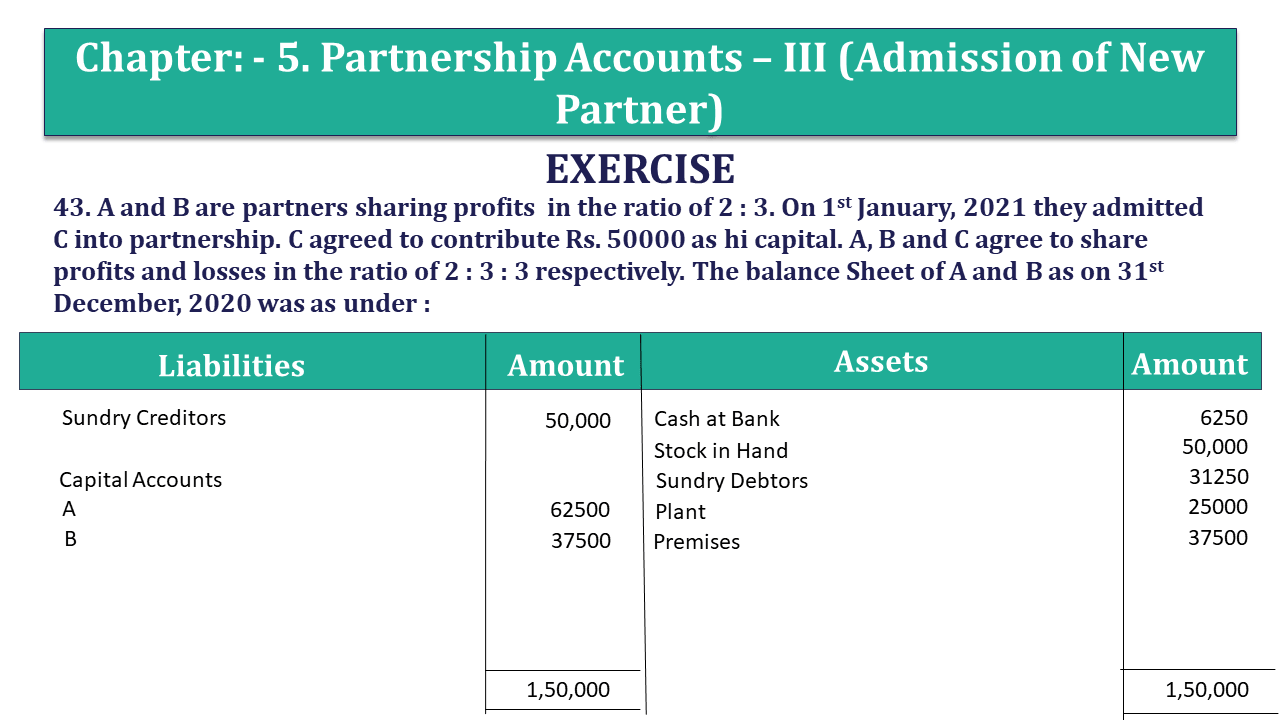

43. A and B are partners sharing profits in the ratio of 2 : 3. On 1st January, 2021 they admitted C into partnership. C agreed to contribute Rs. 50000 as hi capital. A, B and C agree to share profits and losses in the ratio of 2 : 3 : 3 respectively. The balance Sheet of A and B as on 31st December, 2020 was as under :

| Liabilities | Amount | Assets | Amount |

| Sundry Creditors | 50,000 | Cash at Bank | 6250 |

| Capital Accounts | Stock in Hand | 50,000 | |

| A | 62500 | Sundry Debtors | 31250 |

| B | 37500 | Plant | 25000 |

| Premises | 37500 | ||

| 1,50,000 | 1,50,000 |

They agreed to revalue the assets as under :

Stock on hand Rs. 45000 ; Plant Rs. 18000 ; Premises Rs. 50000 ; a provision of 5% for doubtful debts is to be made. C agrees to transfer to Rs. 15000 to A’s and B’s capital accounts for goodwill from his capital account in 2 : 3.

Pass necessary journal entries, prepare revaluation A/c, capital accounts of A, B and C and a revised Balance Sheet.

The solution of Question 43 Chapter 5 – Unimax Class 12 Part 1

| Particulars | Rs. | Particulars | Rs. | |

| To Stock A/c | 5000 | By Premises A/c | 12500 | |

| To Plant A/c | 7000 | By Loss on Revaluation A/c | ||

| To Provision on doubtful debts A/c | A ( 2/5 X 1063) | 425 | ||

| (5/100 X 31250) | 1563 | B ( 3/5 X 1063) ( 2 : 3 ) | 638 | 1063 |

| 13563 | 13563 |

Capital Accounts

| Particulars | M | N | R | Particulars | M | N | R |

| To Loss on revaluation A/c | 425 | 638 | _ | By Balance b/d | 62500 | 37500 | _ |

| To A’s Capital A/c | _ | _ | 6000 | By Bank A/c | _ | _ | 50000 |

| To B’s Capital A/c | _ | _ | 9000 | By C’s Capital A/c | 6000 | 9000 | _ |

| To Balance b/d | 68075 | 45862 | 35000 | ||||

| 68500 | 46500 | 50000 | 68500 | 46500 | 50000 |

Balance Sheet

| Particulars | Rs. | Particulars | Rs. | ||

| Sundry Creditors | 50000 | Plant | 18000 | ||

| Capital Accounts | Premises | 50000 | |||

| A : | 68075 | Cash at Bank | 56250 | ||

| B : | 45862 | Stock in hand | 45000 | ||

| C : | 35000 | 148937 | Debtors | 31250 | |

| Less Provision for sacrifice debts | 1563 | 29687 | |||

| 198937 | 198937 |

Journal

| Date | Particulars | L.F. | Debit | Credit | |

| Revaluation a/c | Dr. | 13563 | |||

| To Stock a/c | 5000 | ||||

| To Plant a/c | 7000 | ||||

| To Provision for bad debts a/c | 1563 | ||||

| (Being decrease in the value of assets) | |||||

| Premises a/c | Dr. | 12500 | |||

| To Revaluation A/c | 12500 | ||||

| (Being increase in the value of asset) | |||||

| A’s Capital a/c | Dr. | 425 | |||

| B’s Capital a/c | Dr. | 638 | |||

| To Revaluation A/c | 1063 | ||||

| (Being net loss on revaluation transferred to old partners capital a/c in old ratio) | |||||

| Bank a/c | 50000 | ||||

| To C’s capital a/c | 50000 | ||||

| (Being capital introduced by new partners in cash) |

| Date | Particulars | L.F. | Debit | Credit | |

| C’s capital a/c | Dr. | 15000 | |||

| To A’s Capital A/c | 6000 | ||||

| To B’s Capital A/c | 9000 | ||||

| (Being amount transferred from C’s capital a/c to A and B’s capital a/c on account of goodwill) |

Working Note

Old Share – New share

A’s sacrifice = Old share – new share

= 2/5 – 2/8

= 6/40

B’s sacrifice = 3/5 – 3/8

= 9/40

S.R. = 6 : 9 = 2 : 3

M and N will share goodwill = 2 : 3 = 6000 : 9000

What is Partnership – Meaning and Its 4 Types

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication