Question 35 Chapter 1 of Class 12 Part – 1

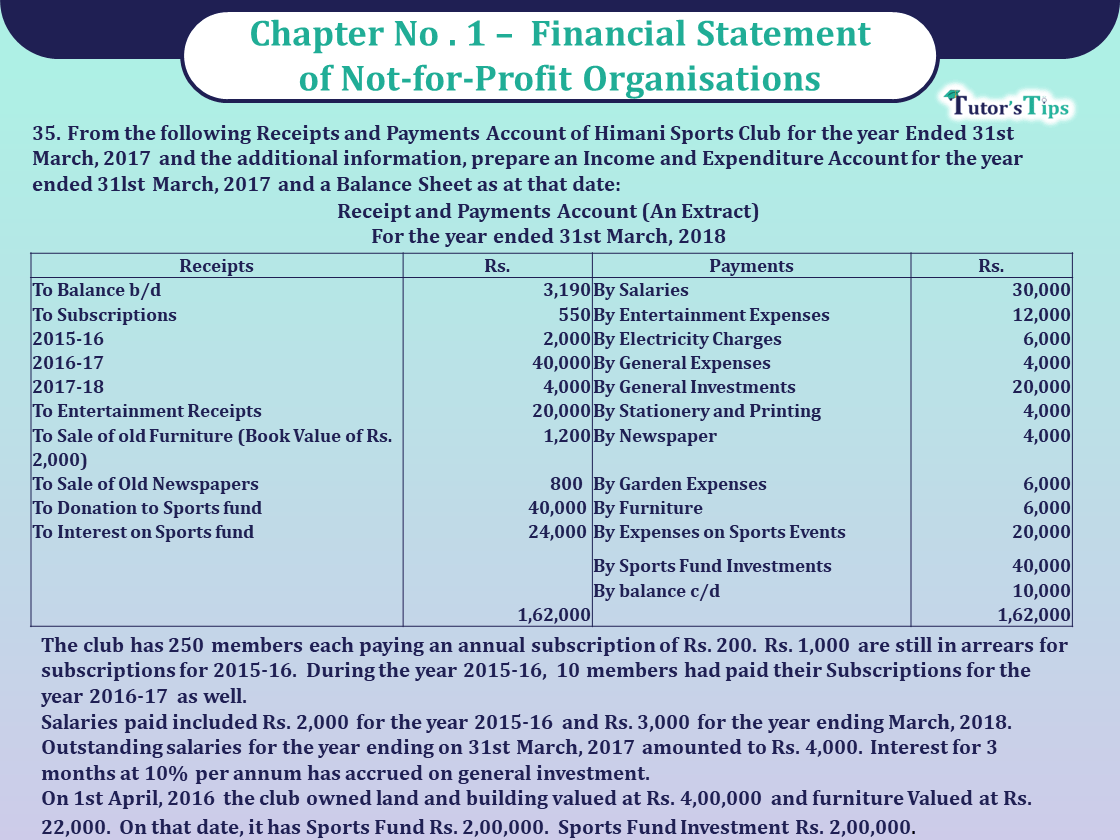

35. From the following Receipts and Payments Account of Himani Sports Club for the year Ended 31st March, 2017 and the additional information, prepare an Income and Expenditure Account for the year ended 31lst March, 2017 and a Balance Sheet as at that date:

Receipt and Payments Account (An Extract)

For the year ended 31st March, 2018

| Receipts | Rs. | Payments | Rs. |

| To Balance b/d | 3,190 | By Salaries | 30,000 |

| To Subscriptions | 550 | By Entertainment Expenses | 12,000 |

| 2015-16 | 2,000 | By Electricity Charges | 6,000 |

| 2016-17 | 40,000 | By General Expenses | 4,000 |

| 2017-18 | 4,000 | By General Investments | 20,000 |

| To Entertainment Receipts | 20,000 | By Stationery and Printing | 4,000 |

| To Sale of old Furniture (Book Value of Rs. 2,000) | 1,200 | By Newspaper | 4,000 |

| To Sale of Old Newspapers | 800 | By Garden Expenses | 6,000 |

| To Donation to Sports fund | 40,000 | By Furniture | 6,000 |

| To Interest on Sports fund | 24,000 | By Expenses on Sports Events | 20,000 |

| By Sports Fund Investments | 40,000 | ||

| By balance c/d | 10,000 | ||

| 1,62,000 | 1,62,000 |

The club has 250 members each paying an annual subscription of Rs. 200. Rs. 1,000 are still in arrears for subscriptions for 2015-16. During the year 2015-16, 10 members had paid their Subscriptions for the year 2016-17 as well.

Salaries paid included Rs. 2,000 for the year 2015-16 and Rs. 3,000 for the year ending March, 2018. Outstanding salaries for the year ending on 31st March, 2017 amounted to Rs. 4,000. Interest for 3 months at 10% per annum has accrued on general investment.

On 1st April, 2016 the club owned land and building valued at Rs. 4,00,000 and furniture Valued at Rs. 22,000. On that date, it has Sports Fund Rs. 2,00,000. Sports Fund Investment Rs. 2,00,000.

The solution of Question 35 Chapter 1 of Class 12 Part – 1: –

District Club

Income and Expenditure Account

For the year ended on 31st March, 2018

| Expenditure | Amount | Income | Amount | ||

| To Salaries | 30,000 | By Subscriptions | 40,000 | ||

| Less: Outstanding in the beginning | 2,000 | Add: Received in 2015-16 (10x 200) | 2,000 | ||

| 28,000 | Add: Outstanding (50,000-42,000) | 8,000 | |||

| Less: Advance for the next year | 3,000 | By Surplus from Entertainment | 50,000 | ||

| 25,000 | Receipts | 20,000 | |||

| Add: Outstanding at the end | 4,000 | 29,000 | Less: Payments | 12,000 | |

| To Electricity Charges | 6,000 | By Sale of old Newspapers | 8,000 | ||

| To General Expenses | 4,000 | By Interest on General Investments | 800 | ||

| To Stationery and Printing | 4,000 | 500 | |||

| To Newspapers | 4,000 | ||||

| To Garden Expenses | 6,000 | ||||

| To Loss on sale of Furniture | 800 | ||||

| To Surplus, i.e., Excess of Income over Expenditure | 5,500 | ||||

| 59,300 | 59,300 |

Balance Sheet (as at 31st March 2018)

| Liabilities | Amount | Assets | Amount | ||

| Subscriptions Received in advance | 1,000 | Cash | 10,000 | ||

| Salaries Outstanding | 8,000 | Sports Fund Investments | 2,00,000 | ||

| Sports Fund | 1,69,500 | Add: Additions during the year | 40,000 | 2,40,000 | |

| Add: Donations | General Investments | 20,000 | |||

| Add: Interest | Interest accrued on General Investments | 500 | |||

| Less: Expenses on Sports events | Salaries paid in Advance | 3,000 | |||

| Capital Fund (WN) | Subscriptions Outstanding | ||||

| Add: Surplus | For the year 2015-16 | 1,000 | |||

| for the year 2016-17 | 8,000 | 9,000 | |||

| Furniture | 22,000 | ||||

| Add: Additions during the year | 6,000 | ||||

| 28,000 | |||||

| Less: Sale | 2,000 | 26,000 | |||

| Land and Building | 4,00,000 | ||||

| 7,08,500 | 7,08,500 | ||||

Working Note:

To ascertain Capital Fund, Balance Sheet is prepared as at 1st April, 2016 as under:

Balance Sheet (as at 1st April 2016)

| Liabilities | Amount | Assets | Amount | |

| Salaries Outstanding | 2,000 | Subscriptions Outstanding (2,000+ 1,000) | 3,000 | |

| Subscriptions Received in advance | 2,000 | Cash | 30,000 | |

| Sports Fund | 2,00,000 | Sports Fund Investments | 2,00,000 | |

| Capital Fund (balancing figure) | 4,51,000 | Furniture | 22,000 | |

| Land and Building | 4,00,000 | |||

| 6,55,000 | 6,55,000 | |||

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of all Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

Chapter No. 1 – Accounting Not for Profit Organisations

Chapter No. 2 – Partnership Accounts – I (Introduction)

Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Chapter No. 8 – Company Accounts (Share Capital)

Chapter No. 9 – Company Accounts (Issue of Debentures)

Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

Chapter No. 1 – Financial Statements of a Company

Chapter No. 2 – Financial Statement Analysis

Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

Chapter No. 4 – Ratio Analysis

Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication