Question 31 Chapter 8 – Unimax Publication Class 12 Part 2 – 2021

Table of Contents

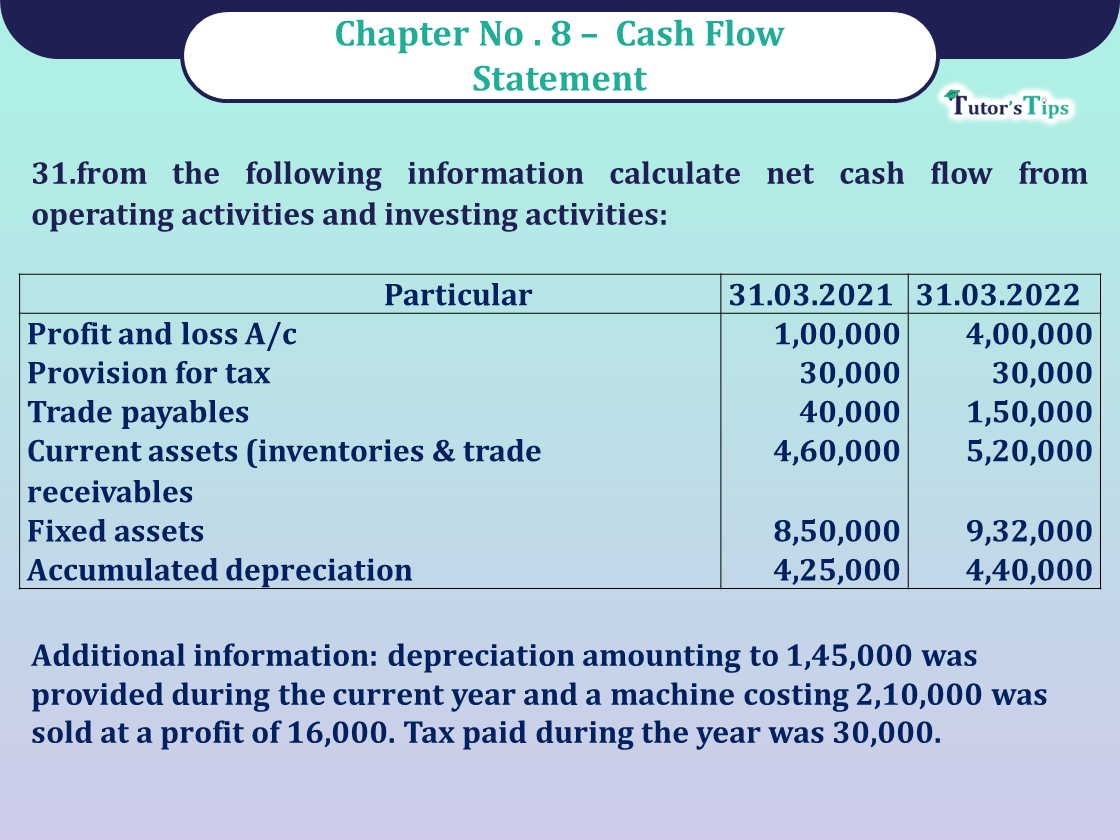

31.from the following information calculate net cash flow from operating activities and investing activities:

| Particulars | 31-3-2021 | 31-3-2022 |

| Profit and loss A/c | 1,00,000 | 4,00,000 |

| Provision for tax | 30,000 | 30,000 |

| Trade payables | 40,000 | 1,50,000 |

| Current assets (inventories & trade receivables | 4,60,000 | 5,20,000 |

| Fixed assets | 8,50,000 | 9,32,000 |

| Accumulated depreciation | 4,25,000 | 4,40,000 |

Additional information: depreciation amounting to 1,45,000 was provided during the current year and a machine costing 2,10,000 was sold at a profit of 16,000. Tax paid during the year was 30,000.

The solution of Question 31 Chapter 8 – Unimax Publication Class 12 Part 2-2021 : –

Calculation of net cash flow from operating &

Investing activities

| Particulars | ₹ | |

| I. Cash flow from operating activities | ||

| A.net profit before tax | 3,30,000 | |

| B. add: depreciation | 1,45,000 | |

| Less: profit on sale of machinery | (16,000) | |

| C. operating profit before working capital changes | 4,59,000 | |

| D. charges in current assets & current liabilities: | ||

| Increase in current assets | (60,000) | |

| Increase in current liability | 1,10,000 | 50,000 |

| E. net cashflow from operating activities before tax | 5,09,000 | |

| F. less tax paid | (30,000) | |

| Net cash inflow from operating activities before tax | 4,79,000 | |

| I . cashflow from investing activities | ||

| Sale of machinery | 96,000 | |

| Purchase of fixed assets | (2,92,000) | |

| Net cash used in investing activities | (1,96,000) |

Working notes:

| Calculation of net profit before taX | |

| Closing balance of P & L A/c | 4,00,000 |

| Less: operating balance of P & L A/c | (1,00,000) |

| Add: tax | 30,000 |

| Net profit before tax | 3,03,000 |

Working notes: (2)

Provision for depreciation account

| Particulars | ₹ | Particulars | ₹ |

| To assets disposal A/c (B. fig) | 1,30,000 | By balance b/d | 4,25,000 |

| To balance c/d | 4,40,000 | By P & L A/c (dep.) | 1,45,000 |

| 5,70,000 | 5,70,000 |

Working note: (3)

Fixed assets account

| Particulars | ₹ | Particulars | ₹ |

| To balance b/d | 8,50,000 | By assets disposal A/c | 2,10,000 |

| To bank A/c (purchase) | 2,92,000 | By balance c/d | 9,32,000 |

| 11,42,000 | 11,42,000 |

Working note: (4)

Asset’s Disposal Account

| Particulars | ₹ | Particulars | ₹ |

| To fixed assets A/c | 2,10,000 | By provision for depreciation A/c | 1,30,000 |

| To P & L A/c (profit) | 16,000 | By bank A/c (B. fig) (80,000 +16,000) | 96,000 |

| 2,26,000 | 2,26,000 |

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

What is the cash flow statement? why do we need to prepare?

Unimax Publication – Accountancy PSEB Class 12 – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Change in Profit sharing ratio among Existing Partners )

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Unimax Publication – Accountancy PSEB (Class 12) – Part – II – Solution

- Chapter No. 1 – Company Accounts (Share Capital)

- Chapter No. 2 – Company Accounts (Issue of Debentures)

- Chapter No. 3 – Company Accounts (Redemption of Debentures)

- Chapter No. 4 – Financial Statements of a Company

- Chapter No. 5 – Financial Statement Analysis

- Chapter No. 6 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 7 – Ratio Analysis

- Chapter No. 8 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2023@ Official Website of Sultan Chand Publication